Dahna M. Chandler, MPS, is an award-winning finance journalist with over 25 years of experience writing for major media outlets and top blogs. Committed to helping people thrive financially, she specializes in educating readers with guides, tips, and tools for managing their money effectively. Read more about Dahna's work at The Financial Content Architect.

Updated: November 2025 — The IRS has not yet published its 2025 filing updates. This page will be refreshed as soon as new guidance is released.

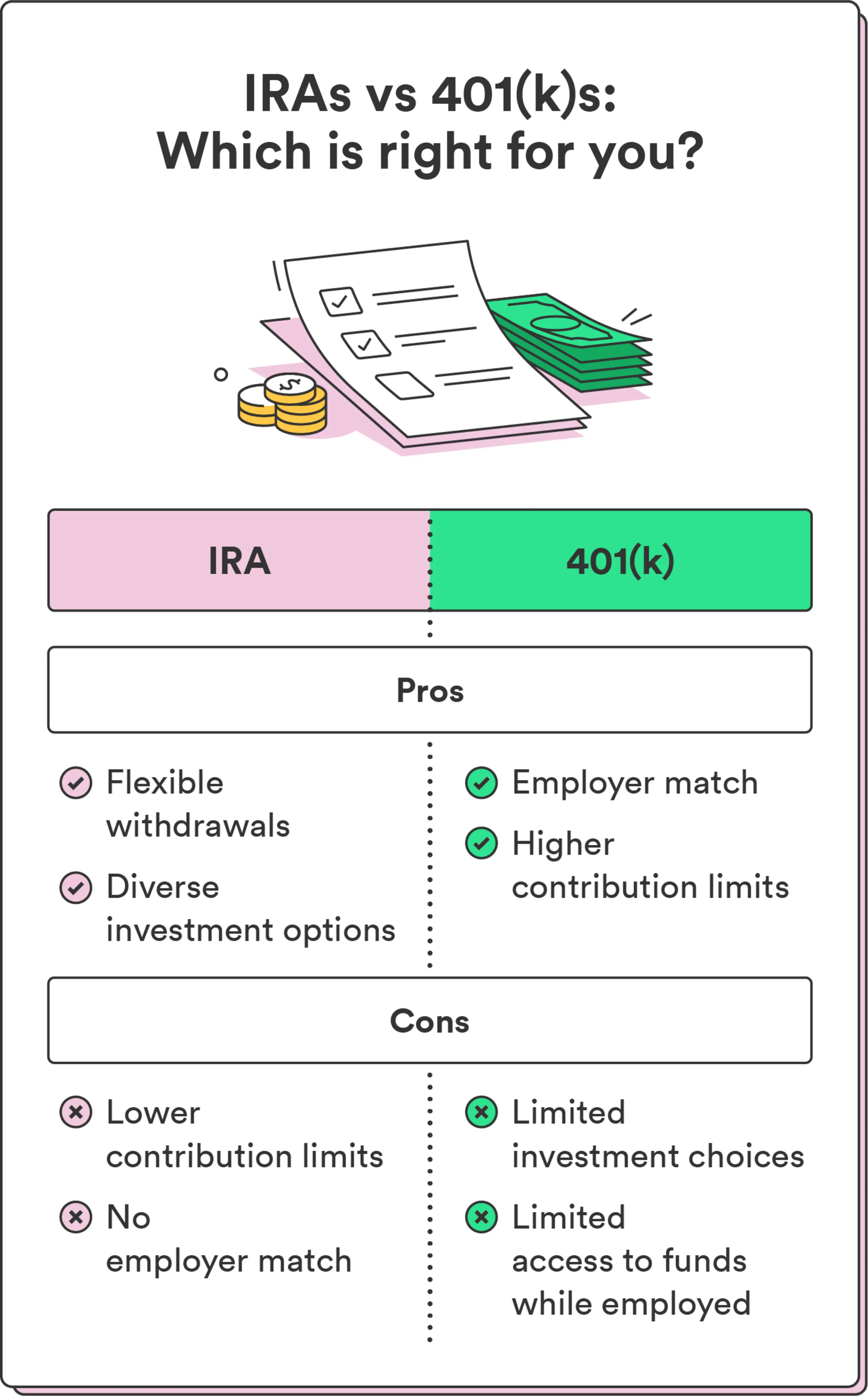

When planning for a financially secure retirement, you might consider two investment vehicles: individual retirement accounts (IRAs) and 401(k)s. Both help you save for retirement, but they come with their own sets of rules and benefits. Understanding the difference between an IRA and 401(k) can help increase your retirement savings.

An IRA is a tax-advantaged account that you set up independently to save for retirement. It offers a variety of investment options, including stocks, bonds, and mutual funds.

A 401(k) is a retirement savings plan sponsored by your employer. It allows you to save a portion of your paycheck before taxes. Often, employers match your contributions. Keep reading to learn the key differences between these two investment vehicles and how to use them most effectively in your retirement planning.

Comparing IRAs and 401(k)s

Navigating the labyrinth of retirement account options can be overwhelming at first. But understanding the distinctions between an IRA and a 401(k) can help you confidently grow your retirement nest egg.

Before you decide the best retirement account for you, let's compare the two. How is a 401k different from an individual retirement account (IRA)? 1,2

As you can see, both types of accounts offer savings benefits. But let's explore more about each, so you can determine if you should use one or both in your retirement plan.

IRA

401(k)

2025 Contribution Limits (Under 50)

$7,0003

$23,5003

2025 Catch-Up Limits (50 and older)

$8,0003

$31,0003

2025 Secure 2.0 Catch-Up Limits (61-63)

$1,0004

$11,2504

Contributions Source

You determine your own contributions

Automatic paycheck deductions with potential employer matches

Investment Options

Diverse asset choices (stocks, mutual funds, etc.)

Typically limited to a few funds selected by the administrator

Account Setup

You set up your own account

Established by employers

Account Types

Traditional, Roth, SEP, and SIMPLE

Roth and traditional 401(k)

Required Minimum Distributions (RMDs)

Start at age 73 or 75, depending on birth year

(Roth IRAs exempt)

Start at age 73 or 75, depending on birth year

(Roth 401(k)s subject to minimum distributions)

Benefits of choosing IRA vs 401(k)

Deciding between an individual retirement account (IRA) and a 401(k) is essential for developing the right retirement fund strategy. Both investment vehicles offer distinct tax advantages and contribution limits.

Here are six elements to consider when deciding between the two retirement accounts:

Flexibility in contribution limits. The IRA offers a degree of financial flexibility that is helpful for those with variable income streams. If you're under 50, the maximum annual contribution to your IRA is $7,000 in 2025.3 Because of the catch-up provisions allowed by federal law, an IRA has an annual contribution limit of $8,000 in 2025 for those over age 50. That's $7,000 plus an additional $1,000 in "catch-up" contributions for those 50 and over trying to make up for not contributing enough to their IRAs in earlier years to reach their retirement savings goals. IRAs also allow you to adjust contributions depending on your circumstances each year.3,4

Diverse investment options. One of the clearest benefits of an IRA is the range of investment options. Unlike 401(k)s, which often limit investors to a selection of funds, IRAs offer a range of assets like stocks, bonds, mutual funds, and index funds. This diversity can help you adopt a more strategic approach to retirement planning, like investing based on your values.3

Dependency on employer match. The matching contributions many employers offer with their401(k)s is appealing, as this is not available with IRAs. Employer matches are beneficial, but their absence in an IRA means you maintain control over your retirement contributions. You're also not dependent on the employer's health or your job to build your retirement savings. This independence can especially appeal to freelancers and those who prefer full control over their retirement strategy.3

Avoiding administrative fees. Consider the long-term impact of administrative fees often associated with 401(k) plans. IRAs typically come with lower fees, particularly when you use brokerage firms offering low-cost index funds. In the long term, these lower fees can affect your investment returns.3

Tax benefits of traditional IRAs. Roth or traditional IRAs offer their own set of tax advantages. Contributions to a traditional IRA may be tax deductible, reducing your taxable income for the contribution year.3

Pre-tax benefit consideration. Both 401(k)s and traditional IRAs offer the advantage of pre-tax contributions. This feature could allow you to reduce your taxable income, providing tax relief that can be valuable for those in higher tax brackets.3

By understanding these distinct advantages, you can make a more informed decision that aligns closely with your long-term financial objectives. Plus, they can help you answer the question, "Is an IRA better than a 401k?"

401(k) match vs. no match: How it affects you

The availability or lack of a 401(k) employer match often makes a difference in the way you shape your retirement investment strategy. It can influence how much you contribute and where you allocate your money for growth. It also can help you decide when it's time to max out your IRA contribution if you have both account types.

If your employer matches your 401(k), you should:

1. Maximize your employer match

Securing an employer match on your 401(k) contributions is like receiving additional income without extra work. If your employer matches your contributions, take advantage of the full employer match to increase the value of your retirement investment fund.

2. Max out IRA contributions

Once you get your full employer match in your 401(k), the next logical step is to maximize contributions to an IRA. That's because your IRA typically offers a broader range of investment options. They can provide opportunities to diversify your portfolio and potentially realize higher returns.

3. Consider 401(k) after IRA maxed

If you've reached the annual contribution limit for your IRA and still have extra funds, revisit your 401(k) options. Additional 401(k) contributions can further supplement your retirement savings and offer tax advantages.

Actions to take if your employer doesn't match your 401(k) include:

1. Prioritize IRA contributions

Without an employer match, the IRA may be an even more important opportunity for retirement savings. The IRA's lower fees and broader investment options also make it a preferable first choice for maximizing contributions.

2. Consider 401(k) after IRA maxed

Even if your employer does not offer a matching contribution, a 401(k) remains a viable path to additional retirement savings. The tax benefits associated with 401(k) contributions still can make it a worthwhile investment after you've maxed out your IRA annual contributions.3

How to choose between a 401(k) and IRA

Determining whether to invest in a 401(k) or IRA depends on a few factors, including your current financial standing, the benefits provided by your employer, if you're self-employed, and your long-term investment objectives.

The argument for a 401(k)

If your employer offers a 401(k)-matching program, take advantage of this opportunity. It's like getting extra income without doing additional work. Acquiring the extra contributions from your employer is one of the main benefits of a 401(k).

Another benefit is that employers typically offer this account type, so there is less manual setup or maintenance needed.

The argument for an IRA

IRAs often provide a broader array of investment options compared to 401(k)s, which are a limited range of mutual funds pre-selected by your employer. This may benefit you if you want more control over the fund's investment strategies or for self-employed individuals who don't have access to employer-sponsored plans.

401(k) plans often have higher administrative fees, which can diminish potential gains. IRAs usually have lower fees. With the latter, you won't get charged commissions or sales charges for selling the shares in the fund.

IRAs offer more flexibility for tax planning. For instance, Roth IRAs allow for tax-free withdrawals upon retirement, providing a hedge against potential tax rate increases in the future. Just remember that early withdrawals from a 401(k) or IRA are unlikely to be tax-free.

401(k)s are an excellent vehicle for retirement savings, especially if your employer offers matching contributions. However, IRAs offer greater flexibility in investment choices and tax planning.

Your choice between the two should be a strategic decision based on an evaluation of your financial situation, investment goals, and the specific features of each type of account.1,2

Chime® is a financial technology company, not a bank. Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC.

Chime is not FDIC-insured. The Bancorp Bank, N.A. and Stride Bank, N.A. are the FDIC-insured members. Deposit insurance covers the failure of an insured bank. Certain conditions must be satisfied for pass-through deposit insurance coverage to apply. FDIC deposit insurance limit is $250,000 per depositor, per insured bank, per ownership category.

Chime Checkbook: While Chime doesn’t issue personal checkbooks to write checks, Chime Checkbook gives you the freedom to send checks to anyone, anytime, from anywhere. See your issuing bank’s Deposit Account Agreement for full Chime Checkbook details.

By clicking on some of the links above, you will leave the Chime website and be directed to a third-party website. The privacy practices of those third parties may differ from those of Chime. We recommend you review the privacy statements of those third party websites, as Chime is not responsible for those third parties' privacy or security practices.

Opinions, advice, services, or other information or content expressed or contributed here by customers, users, or others, are those of the respective author(s) or contributor(s) and do not necessarily state or reflect those of The Bancorp Bank, N.A. and Stride Bank, N.A. (“Banks”). Banks are not responsible for the accuracy of any content provided by author(s) or contributor(s).

APPLE and the Apple Logo are registered trademarks of Apple Inc. GOOGLE PLAY and the Google Play Logo are registered trademarks of Google LLC. Third-party trademarks referenced for informational purposes only; no endorsements implied.

This guide is for informational purposes only. Chime does not provide financial, legal, or tax advice. You should check with your legal, financial, or tax advisor for advice specific to your situation.

Third-party trademarks referenced for informational purposes only; no endorsements implied.

Optional services and products may have fees or charges, such as outbound instant transfers, out-of-network transactions, and credit products. Learn more here.

Out-of-network ATM withdrawal and over the counter advance fees may apply except at FCTI® ATMs in a 7-Eleven® or Speedway, or any Allpoint® or Visa® Plus Alliance ATM participating in the Allpoint network.

Once the retailer accepts your cash, the funds will be transferred to your Chime account. You may use your barcode, debit card, or Chime Card to deposit cash. Cash deposit fees may apply if using a retailer other than Walgreens and Duane Reade. Cash deposits using a barcode or debit card are deposited to your Checking Account. If you have the Chime Card, those funds will be automatically swept to your Chime Card Secured Deposit Account. Cash deposits using your Chime Card first go to your Chime Card Account, then transferred to your Chime Card Secured Deposit Account. Cash deposits are not payment for any Chime Card balance due.

Licenses Chime Capital, LLC, Nationwide Multistate Licensing System ("NMLS") ID 2316451 Chime Payments, Inc., Nationwide Multistate Licensing System (“NMLS”) ID 2538752

Address: 101 California Street, Floor 5, San Francisco, CA 94111, United States.

No customer support available at HQ. Customer support details available on the website.