Send & Receive Money Instantly fee-free with Chime.1

Instantly pay friends through Chime, no matter which bank account they use

No instant cash-out fees

Payments are safe and secure

Chime® Pay Anyone

Learn how we collect and use your information by visiting our Privacy Notice ›

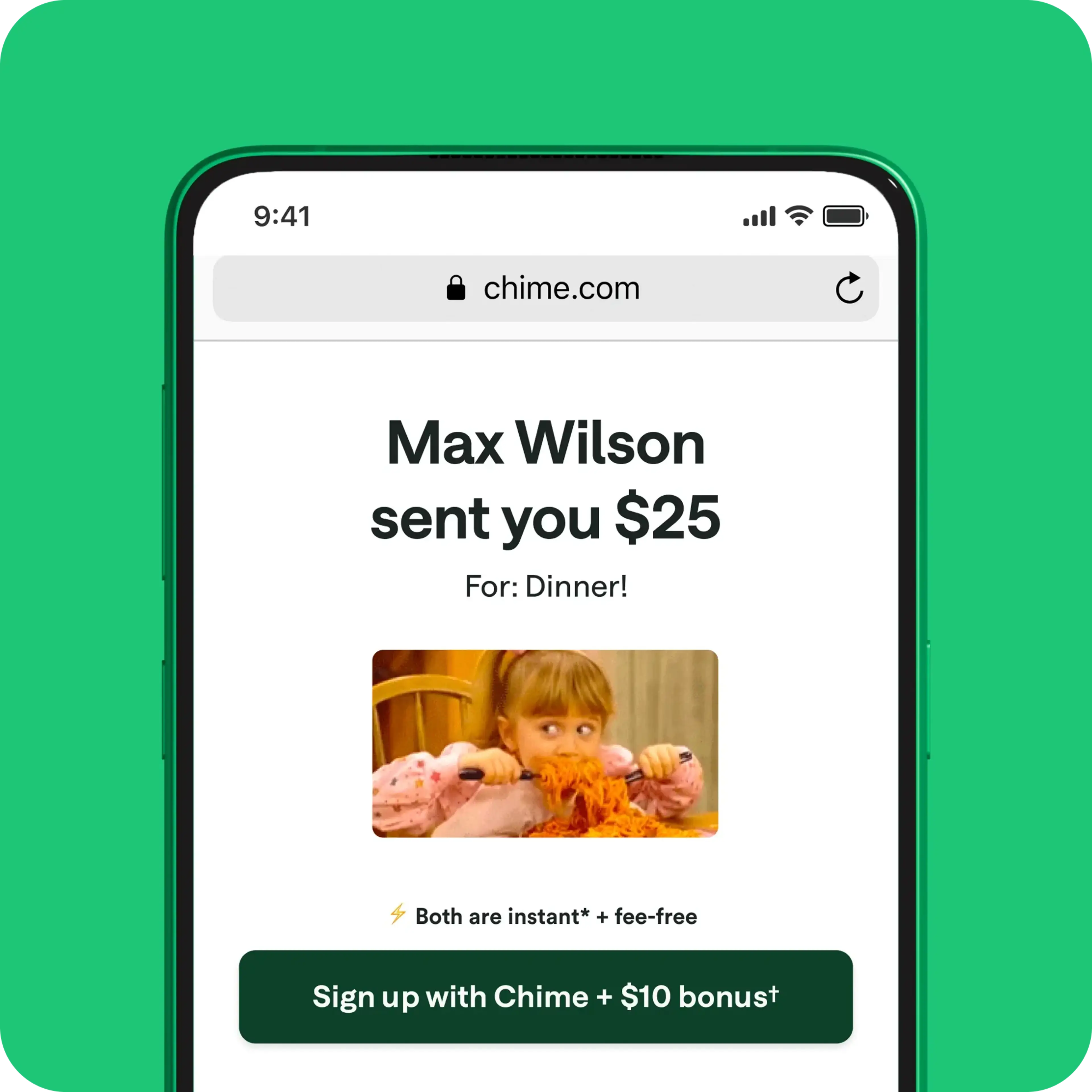

Send and receive money instantly.2

Securely Pay Anyone through Chime in seconds – all they need is a valid debit card to claim their cash. No sign-up needed!

Fee-free instant transfers.

Pay with Chime to avoid instant transfer fees. Your number ones get all their cash when they cash out.

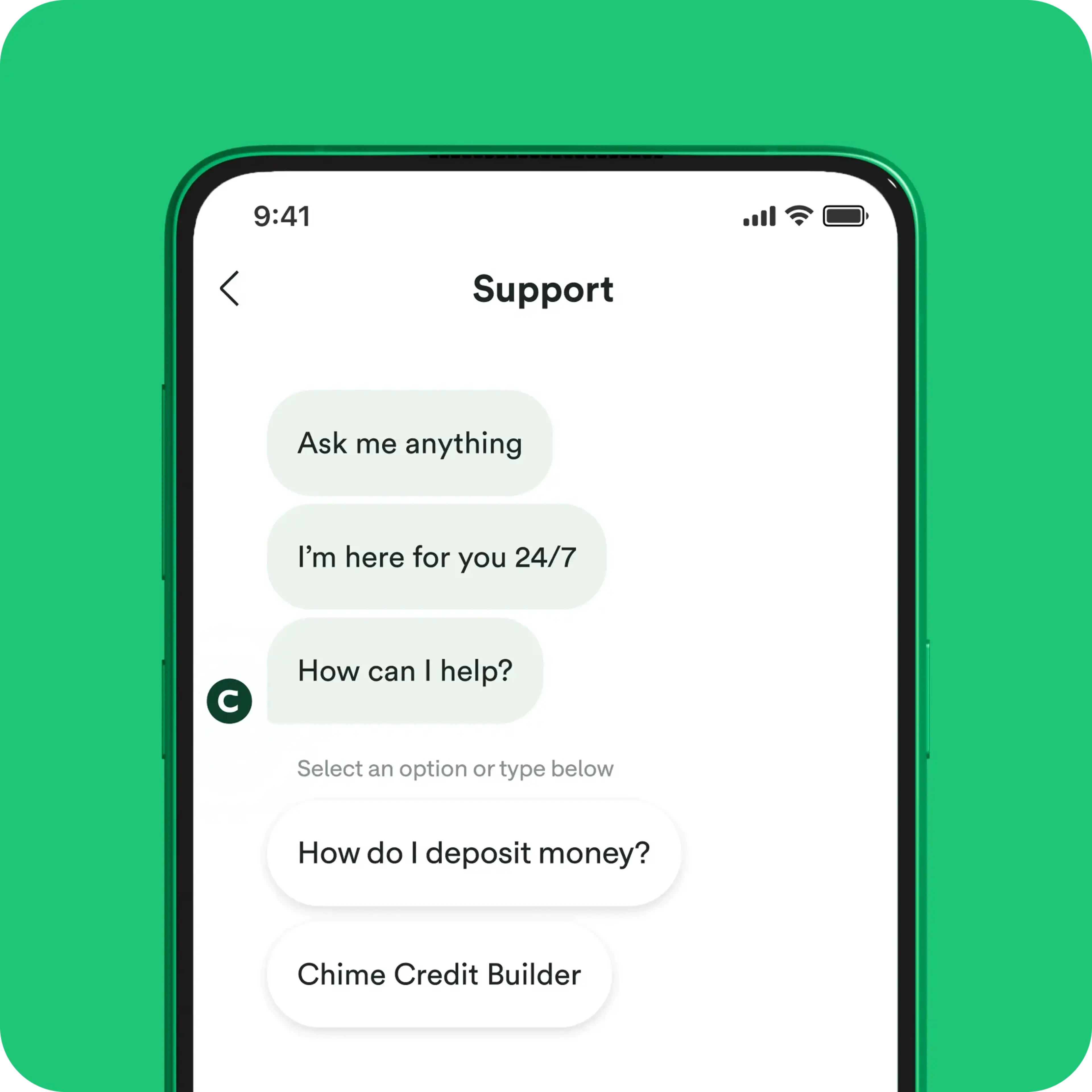

24/7 live support.

You can talk to a human at any time for Chime support. Pay Anyone with peace of mind!

Secure payments.

Chime deposit accounts are FDIC insured through The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC.3

I love Chime for so many reasons - I get paid a day earlier, I can track my money and payments, [and] send money and pay people with ease and confidence.

Bryan P.

I can pay anyone now without having [to use] Zelle or Cash App.

Chelsea M.

The new Pay Anyone feature... has been a livesaver between my husband and I adjusting to our new life together!.. I stayed with Chime because they just keep improving, growing, and make managing my money a breeze!

Jessica B.

Real members. Sponsored content.

Pay anyone instantly — all from one app.

Stop juggling payment apps! With Chime, you can send payments to anyone and manage your money in one place.

Chime | Cash App4,5 | Venmo6,7,8 | PayPal9,10,11 | |

|---|---|---|---|---|

Instant cash-out fee | None | Up to 1.75% | 1.75% | Up to 1.75% |

Both people need an account? | No | Yes | Yes | Yes |

24/7 customer support? | Yes | No | No | No |

Pay Anyone

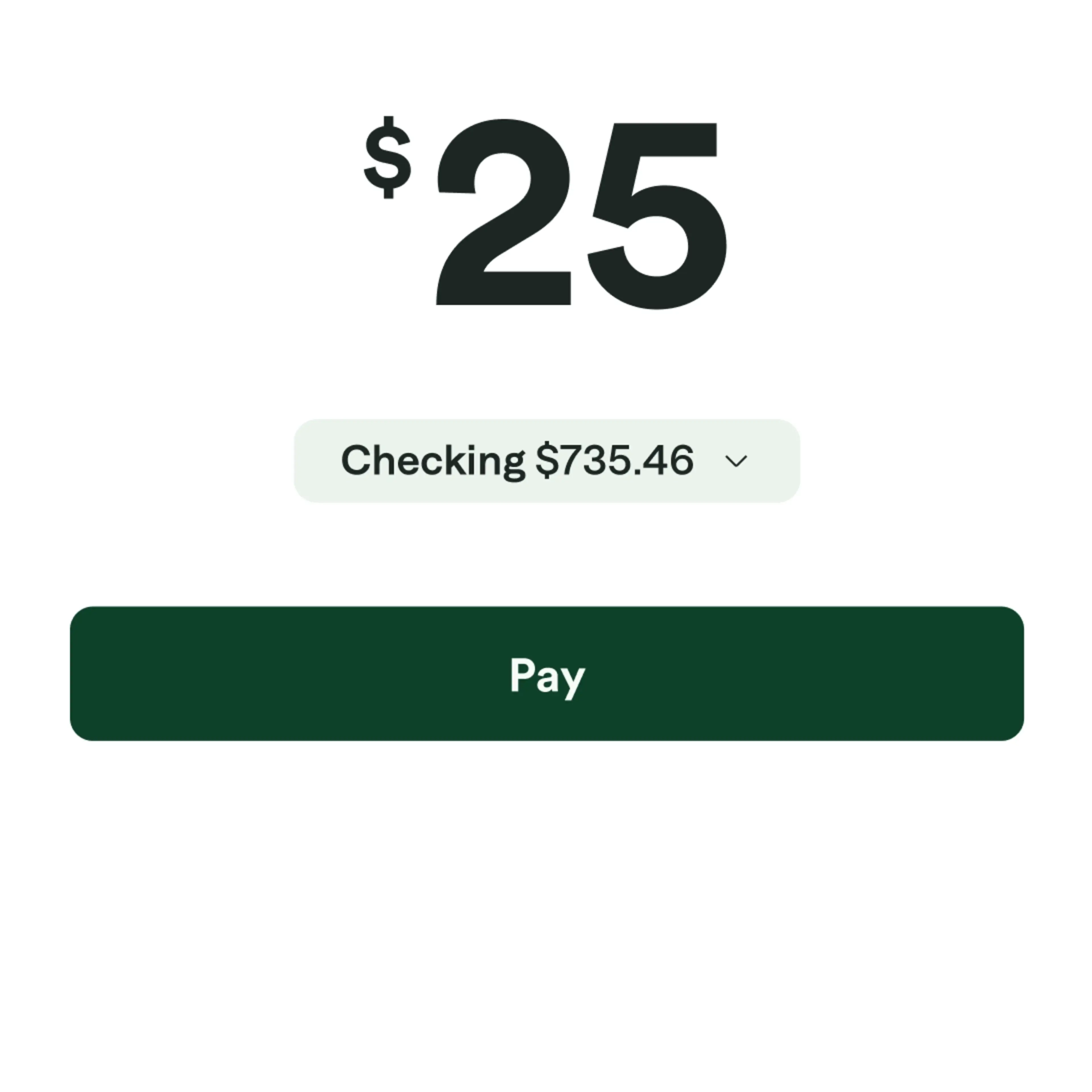

How to Pay Anyone with Chime.

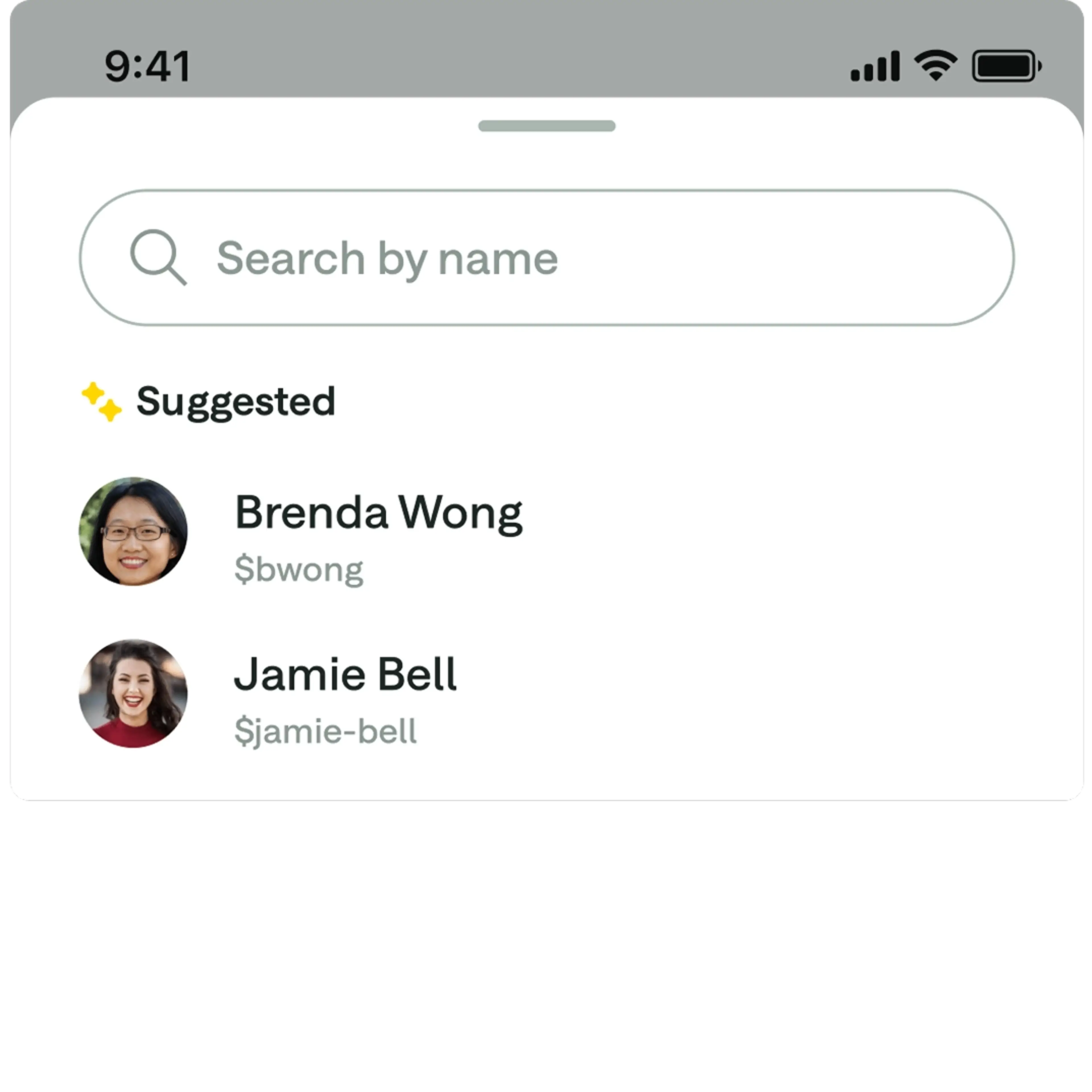

Tell us who you're paying.

Tap “Pay Anyone” to find a friend or enter their $ChimeSign® . You can also pay by email or phone # for someone who isn't on Chime.

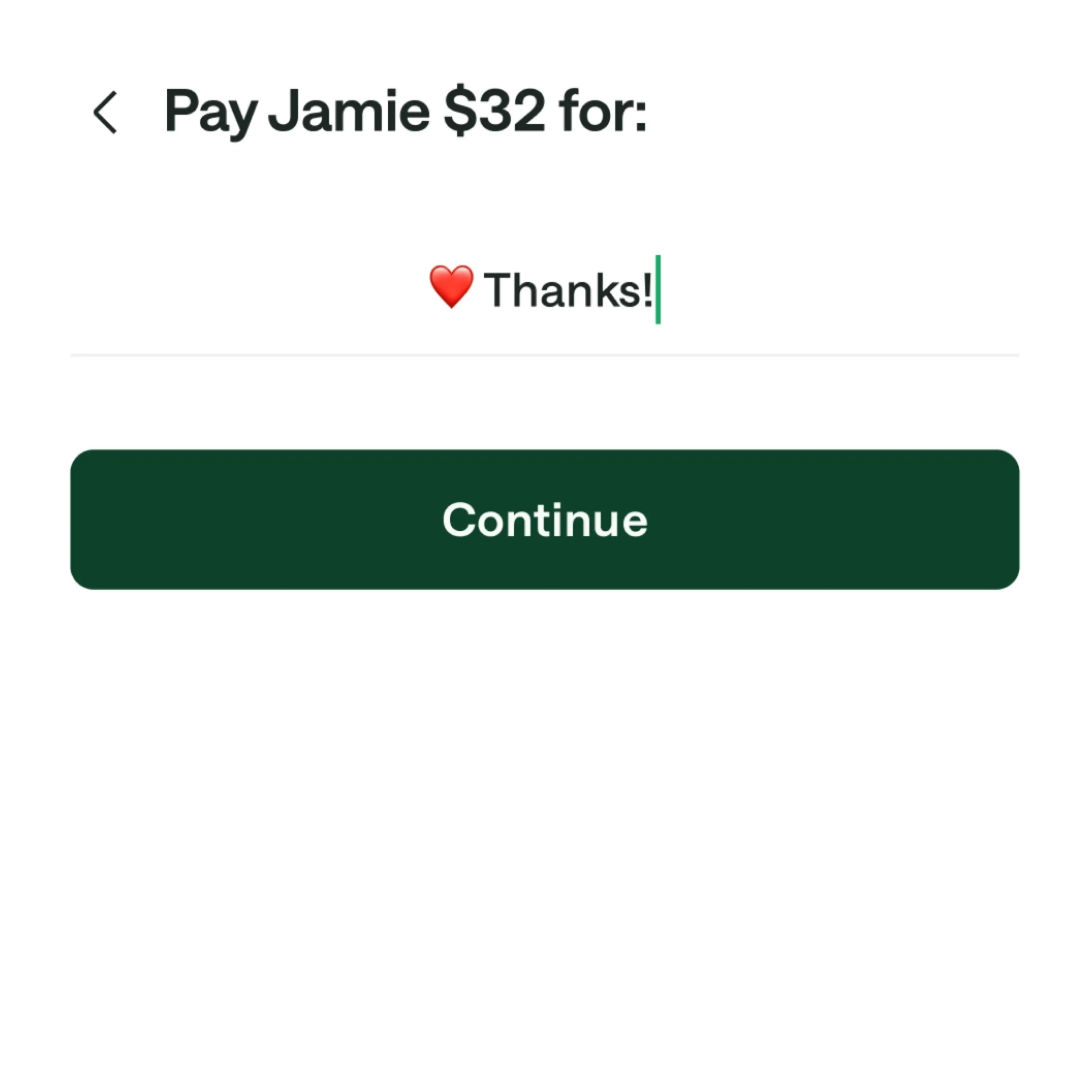

Fill out the info.

Enter the dollar amount and a quick note. Add an emoji or a drop a GIF - it's not just money, it's money from you!

Pay Anyone Instantly2

Choose "Pay." Both Chime members and non-members can get their money instantly! Non-members have up to 14 days to claim funds by entering a valid debit card.

Receive money

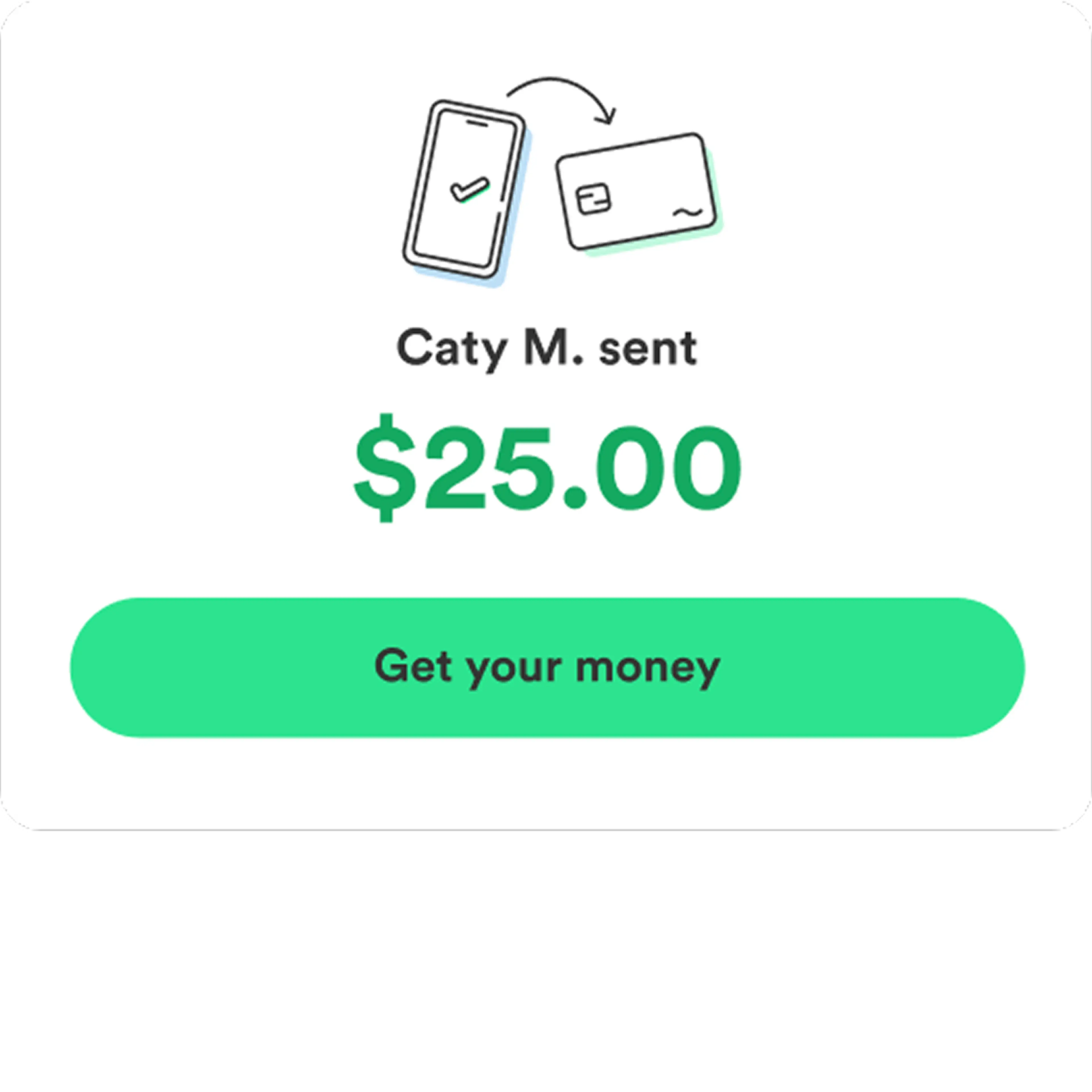

How to receive money with Chime.

Click the link.

You will receive a friendly email or text to claim your funds online. Just click and go!

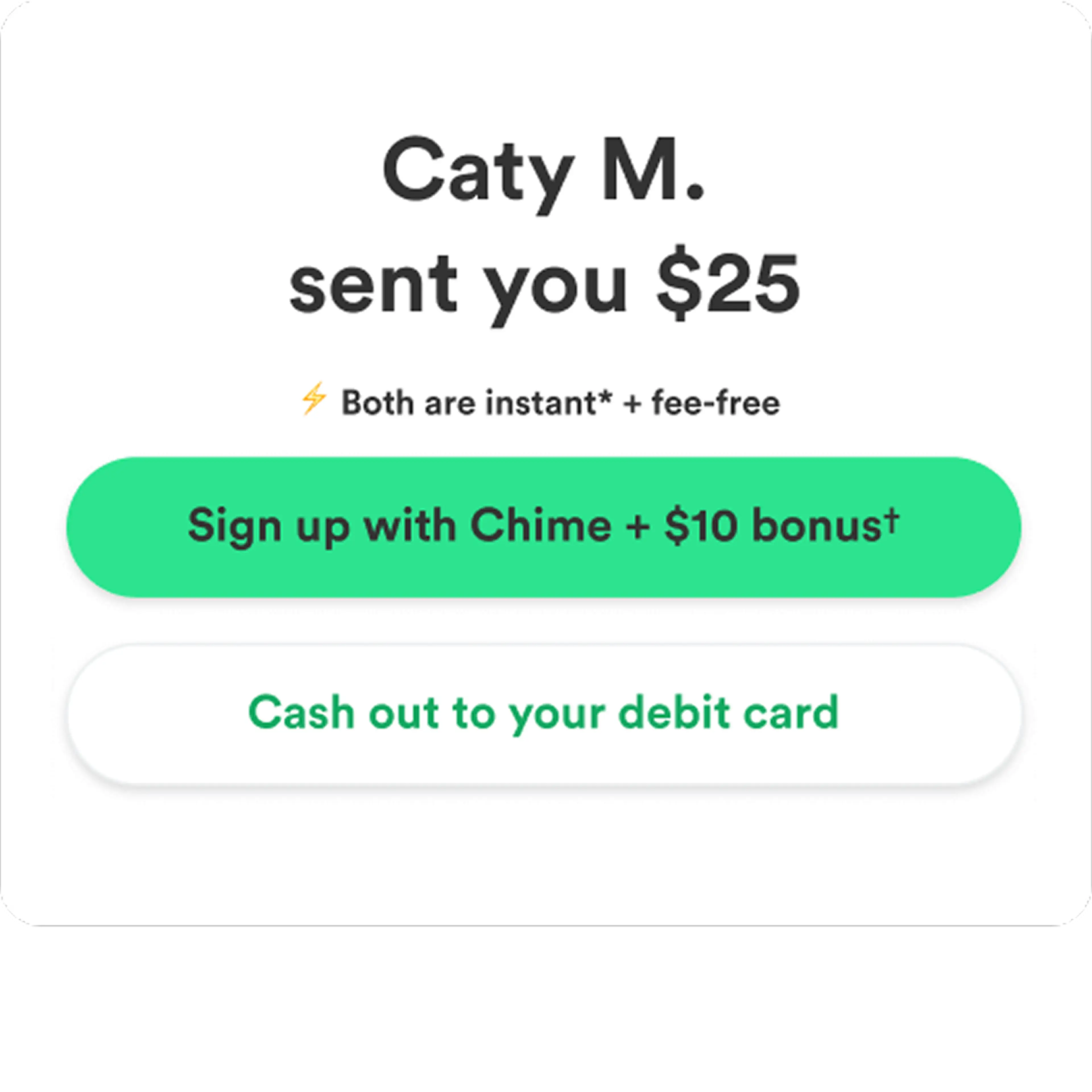

Fill out the info.

You can enter valid debit card information to get the funds transferred to your bank account or create a Chime Checking Account.

Claim your cash!

Once you've entered your info, claim your money and we will transfer the funds to your account without a fee, even for instant cashout. Score!

Unlock Chime Prime for free with direct deposit

Unlock even more Chime benefits when you set up a qualifying direct deposit.12

Ways to use Chime’s Pay Anyone

Splitting expenses

Paying friends and family

Taking care of rent payments and bills

Paying for services

Helping someone out in an emergency

Giving the best gift of all – cash!

Simplify how you send money – all from one app.

FAQs

How do you pay friends and family with Chime?

To use Pay Anyone1 in the Chime app to send money:

Log in to your Chime mobile app.

Select "Pay" at the bottom of the home screen or tap "Pay" at the bottom of the home screen.

Search for your friend’s name or $ChimeSign, or enter the email or phone number of someone who isn’t on Chime.

Enter the amount to send to the recipient and the reason that you’re sending the money.

Confirm the amount and the recipient.

Choose Pay now to send the money.

When I use Chime’s Pay Anyone, is it an instant transfer?

Yes! If you are transferring money to or from someone who is a Chime member, the money transfers are processed immediately.2 If you are paying a friend or family member who does not have Chime, they have 14 calendar days to claim their transfer.

Can I use Pay Anyone to pay friends for free, or will someone be charged a fee?

No one will be charged a fee to send or receive money with Pay Anyone. Fee-free means no fees to you for sending and no fees for them to claim funds instantly.2

How do I know these payments are secure?

Breathe easy: your payments are protected. We keep your money safe and secure with periodic security tests of our systems.

How do I know the money I get from a Pay Anyone transfer is protected?

Any money you receive from a Pay Anyone transfer and deposit into your account is safeguarded. All funds in Chime deposit accounts are FDIC insured up to $250,000 through The Bancorp Bank, N.A. or Stride Bank; Members FDIC.

Can I pay anyone instantly if they’re not in my contacts?

Yes! To pay a friend with Chime who is not on your contact list:

On the Pay Anyone tab, enter your friend’s phone number or email address into the search bar.

Tap the green Pay button that appears with your friend’s information to initiate the transfer.

Can I use Chime to pay friends who aren’t Chime members?

Yes! Using the Pay Anyone feature, you can send money instantly to people who are not members!

You will need the phone number or email address of the person you’d like to send money to.

To send money to a friend who is not a Chime member:

Log in to your Chime mobile app.

Select the Pay Anyone tab.

Enter the email or phone number of someone who isn’t on Chime.

Enter the amount to send to the recipient and the reason that you’re sending the money.

Confirm the amount and the recipient.

Choose Pay now to send the money.

When you pay friends who don’t have Chime, they will receive a text or an email message from Chime to let them know that you’ve sent them money with Pay Anyone. The text or email contains a link to the Chime website where they can open a Chime Checking Account or use their debit card information to claim their money. Your friend could receive up to three (3) reminders to claim their money.

If the friend that you want to pay isn’t a Chime member, they have 14 calendar days to accept the transfer. The funds are returned to your Checking Account if they haven’t claimed the money after 14 days.

What is a $ChimeSign?

A $ChimeSign is a unique handle that acts as a Chime member’s “username.” It makes it easier to send and receive money between Chime members. If someone wants to send you money, you can share your $ChimeSign with them and they can enter it into the recipient field.

How much money can you send on Chime with Pay Anyone?

There is no limit to the number of transactions for Pay Anyone. Transfer limits vary. You can find your Pay Anyone limits under Settings in the Chime app:

Tap the gear icon in the top left-hand corner of the home screen to open Settings

In Account info, select View limits

Scroll down to view your limits for Pay Anyone Transfers

What if I accidentally send money to the wrong person?

Prior to sending money to a friend, you are prompted to confirm the transaction. Once the payment is sent, it cannot be canceled or reversed because the funds are instantly transferred.

It is the sender’s responsibility to ensure that the information is accurate prior to confirming the payment.

If you believe that your Checking Account has been compromised or that a Pay Anyone transfer from your Chime Checking Account was completed without your permission, please contact us at 1-844-244-6363 as soon as you can.

Can I cancel a Pay Anyone P2P transfer that I’ve sent to someone who isn’t a Chime member?

Yes! You can cancel a Pay Anyone transfer if it is still pending:

Tap the transaction in your Chime Checking Account.

Confirm the cancellation.

Once you cancel a pending Pay Anyone transfer, the funds are returned to your Chime Checking Account instantly.

Note that you can only cancel a Pay Anyone transfer if the transfer is still pending. Completed Pay Anyone transfers cannot be reversed.

What are P2P apps?

Peer-to-peer payment apps, often abbreviated to P2P pay apps or simply P2P apps, are mobile apps designed to allow users to send and receive money by connecting their banking information to the app.

Chime is not just a P2P app. You can use Pay Anyone to send money instantly to Chime members and anyone else, but you can also count on Chime to be your one money app for checking, savings, and great features like SpotMe.

Do I need other payment apps if I use Chime?

No! You can send money to anyone, whether they’re on Chime or not, all within the Chime app without paying a fee. With Chime, you don’t have to keep juggling 5 different P2P apps like Cash App, Venmo, or Zelle.