Key takeaways

Here are the main things to know about savings goals and how Chime can help you reach them.

Savings goals organize your money by purpose: Instead of saving into one lump sum, you can create separate goals for things like an emergency fund, a vacation, or a down payment.

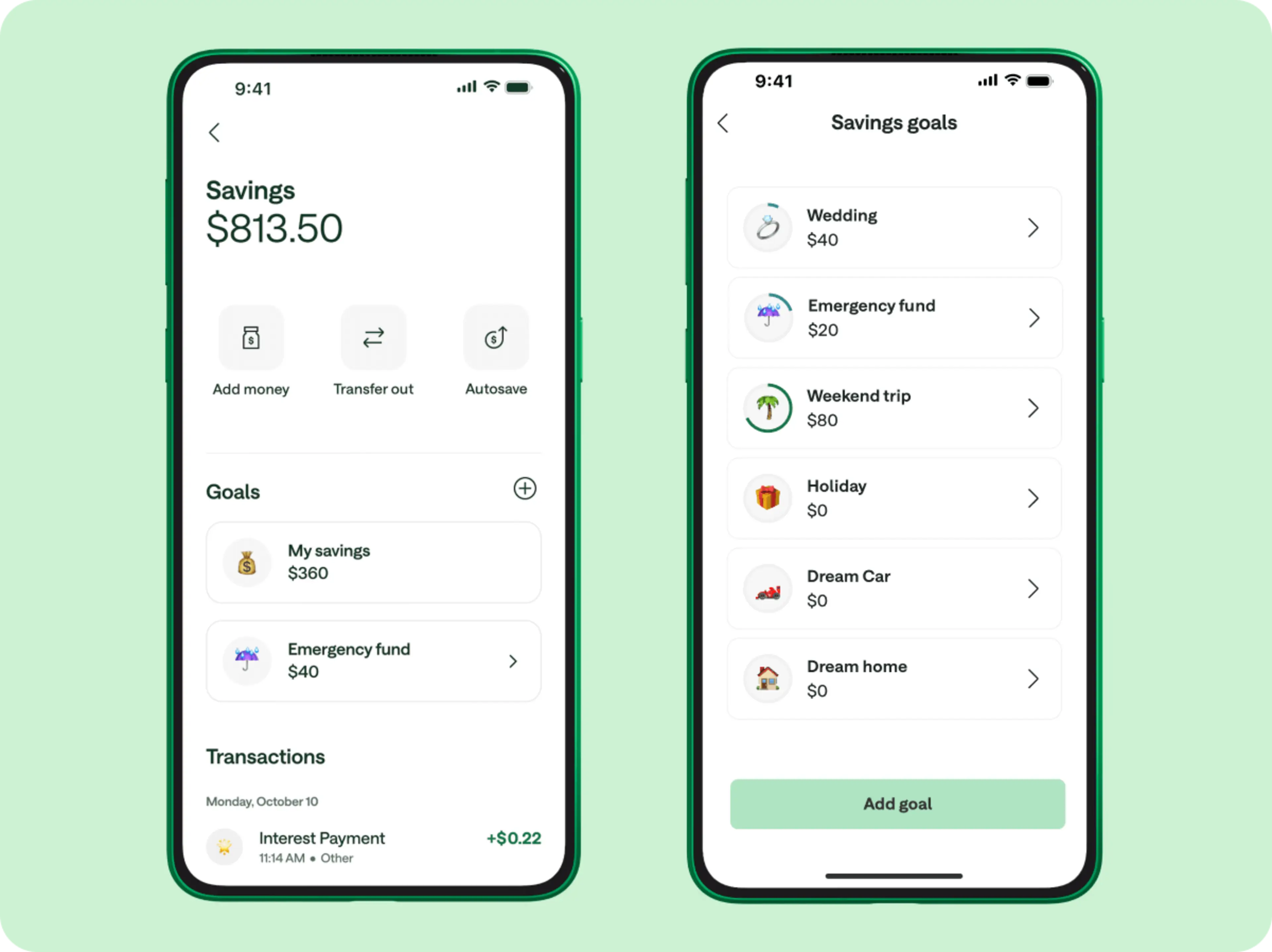

Chime lets you set and track multiple goals: Create savings goals with custom names and targets, and watch your progress bar fill up as you get closer to each one.

Your savings can grow with interest: Chime Prime™ members can earn 3.75% APY, Chime Plus™ members can earn 2.75% APY, and all members earn a base rate of 0.75% APY on funds allocated to Savings Goals.1

You might know how to save money, but it's just as important to have a why. Your why is what motivates you and gets you excited about saving so that it feels like fun, not a chore. Chime® Savings Goals can help you turn small habits into big results – whether you want to build an emergency fund, save for a vacation, or put money toward a down payment on a home.

What are savings goals and why do they matter?

Many financial institutions and financial technology companies now offer savings goals or savings buckets features that let you divide your savings into separate categories within a single account. Chime calls this feature Savings Goals. Ally Bank® offers a similar tool called Buckets2, and SoFi® uses Vaults3.

Third-party brands and companies are mentioned for informational purposes only. Chime does not sponsor, endorse, or partner with any of these brands or companies, and they do not sponsor or endorse Chime.

Savings goals give your money a job. Instead of looking at one lump sum and guessing how much is "available," you can see exactly how much you've set aside for rent, travel, or your emergency fund. This kind of clarity can make it easier to avoid dipping into money you've already committed to something else.

People who set specific financial targets tend to save more than those who save without a plan. A defined goal creates a sense of purpose and accountability. You're not just "saving" – you're saving for something.

How to set up savings goals in the Chime app

Within the Savings Account screen, you can create your own savings goals in just a few taps. Here's how it works.

Create a savings goal. To get started, tap Savings Account on the app's home screen. Tap Set your goal to create your first goal – all you have to do is name it and add a cute emoji to make it stand out.

Set your savings target. Next, you have the option to decide how much you want to save. Maybe that means $1,000 for rainy days or $20,000 for a new car. Setting a savings target is optional – Chime allows you to set money aside for your goal whenever you have some extra to spare.

Add money to your goal. Once you've got a savings target in mind, the next step is funding it. Move funds from Savings Account to a specific goal, or through the Move tab in the app. Completed goals stay visible, so you always have a reminder of what you're capable of achieving.

Types of savings goals to consider

Not sure where to start? Savings goals generally fall into three categories based on your timeline.

Short-term goals

These are goals you can reach within the next 3 to 12 months. They're great for building momentum and creating a savings habit.

Emergency fund starter: Aim for $500 to $1,000 to cover unexpected car repairs, medical bills, or other surprises.

Vacation fund: A weekend getaway might cost $500 to $2,000 depending on the destination.

Holiday and gift fund: Setting aside $50 to $100 a month can help you avoid holiday spending stress.

Mid-term goals

These goals typically take 1 to 5 years to reach. They require more planning but can have a big impact on your financial progress.

Car down payment: A down payment of $2,000 to $5,000 can lower your monthly car payments and help you secure better loan terms.

Home down payment: Even $10,000 to $20,000 toward a home purchase can open doors. Many first-time buyer programs accept down payments as low as 3% of the home price.4

Fully funded emergency fund: Financial experts often recommend saving 3 to 6 months of essential expenses5 – roughly $5,000 to $15,000 for many households.

Long-term goals

These goals stretch beyond 5 years. They take patience, but even small contributions add up over time.

Retirement savings: While dedicated retirement accounts are ideal for long-term growth, a savings goal can help you build the habit of setting money aside regularly.

Education fund: Whether it's for your own continued education or a child's future, saving $50 to $200 a month can grow into a meaningful contribution over several years.

Major life milestone: A wedding, a cross-country move, or starting a business – big life changes often come with big price tags.

Tips for reaching your savings goals

Setting a goal is the first step. Reaching it takes consistency and a solid plan. These strategies can help you stay on track.

Set specific targets: Give your goal a name, a dollar amount, and a deadline. "Save $2,000 for a vacation by December" is much easier to work toward than "save for a trip."

Break big goals into milestones: A $10,000 goal can feel overwhelming. Break it into smaller chunks – like saving $833 per month for 12 months.

Automate your savings: Take the guesswork out of saving by setting up

automatic transfers. Chime offers tools like Allocation and Savings Round-Ups that can move money into your savings automatically.6

Track your progress regularly: Check in on your goals at least once a month. Seeing your progress bar move forward can be a powerful motivator.

Celebrate your wins: Every milestone matters. Reaching a savings target is a real achievement, and recognizing your progress can help you stay motivated for the next one.

How Chime works as a savings goal tracker

Chime designed Savings Goals to make saving easy, empowering, and intuitive. Here are the features that help you stay on top of your progress.

Visual progress bar: As you add funds to your goal, you'll see the progress bar move closer to the finish line. This tracker helps you see your momentum building over time.

Celebratory milestones: When you reach your goal, you'll see a celebratory message in the app. Your completed goals stay visible so you can always be reminded of what you've accomplished.

Multiple goals at once: You can set up multiple goals and contribute to each one at your own pace.

Easy fund transfers: Moving money between your checking account, savings account, and individual goals takes just a few taps in the app.

Earn interest on your savings goals

Your savings goals don't just sit still – they can grow. Chime members earn interest on the money in their goals, which means your balance can increase even when you're not actively adding to it.

Chime Prime members can earn 3.75% APY, Chime Plus members can earn 2.75% APY, and all Chime members earn a base rate of 0.75% APY on funds in their goals.1

That rate difference adds up. On a $5,000 balance, the difference between 0.75% and 3.75% APY is roughly $150 in interest over a year.

Take the first step toward your savings goals

The Savings Goals feature can help you prioritize which goals to work on and create a realistic plan for saving each payday. You don't need to have it all figured out – just pick one goal, give it a name, and start putting a little money toward it.

All you need is a Chime Checking Account, a Chime high-yield savings account, and the Chime app to get started.7