Key takeaways

The time it takes to receive your tax refund depends on when you file and whether there are any errors on your forms.

Most e-filed refunds are paid within 21 days, while mailed refunds might take four or more weeks to process.1

Once you've filed your tax return, you can check its status online, by phone, or via the IRS app.

Once you file your taxes, you'll eagerly anticipate your IRS tax refund hitting your account. It's hard to wait, and the IRS's timeline can lag if there are any errors with your tax return.

If your return is error-free, there are ways to speed up the refund process and access your tax return status as soon as possible.

Let's take a look at how the tax refund process works, the estimated tax refund schedule for 2026, and how to check your tax refund status.

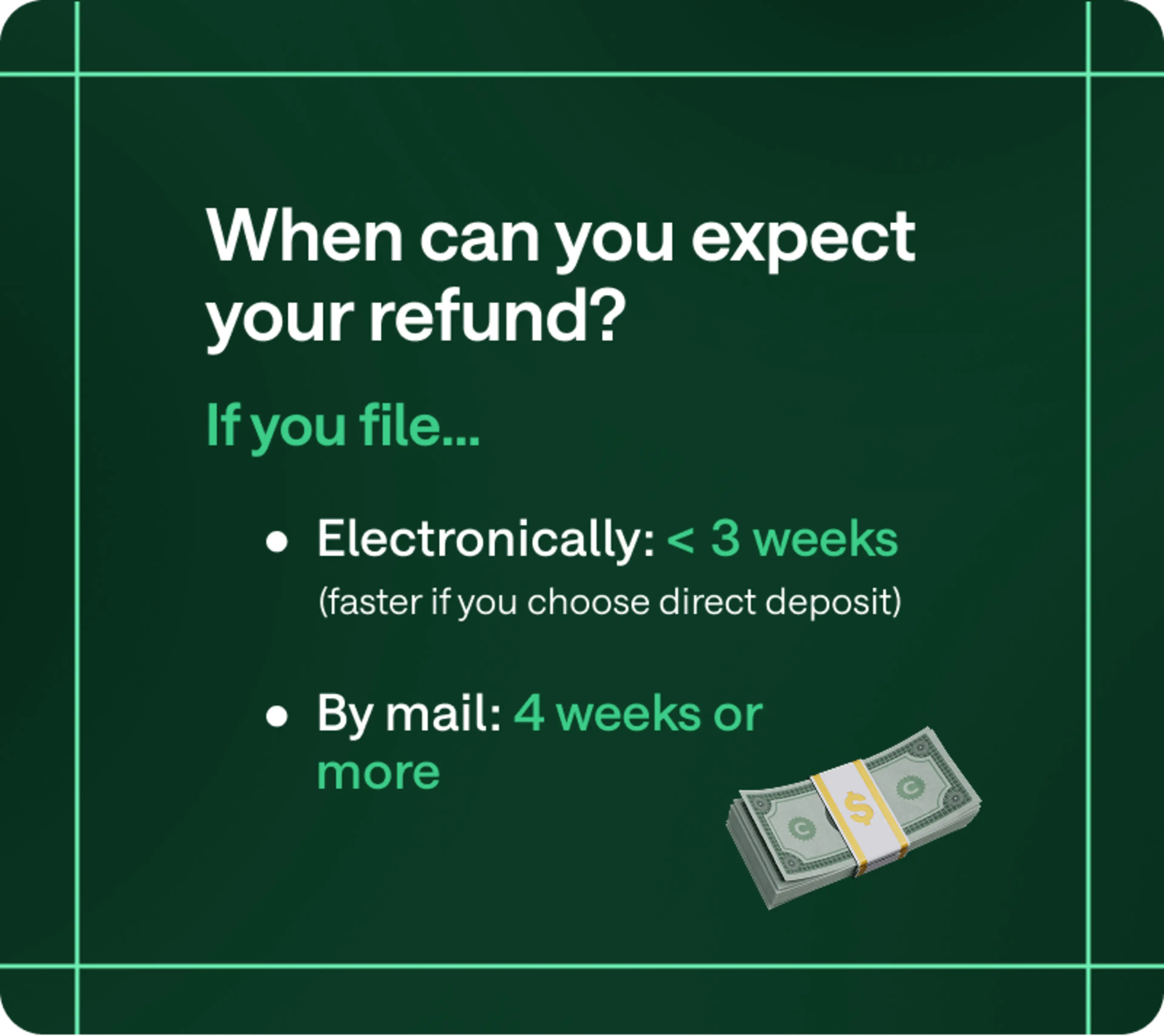

When will I get my 2025 tax refund?

If you e-filed your return, you could receive your refund through direct deposit faster than if you mailed in your tax documents. You can expect a paper tax refund in the mail in four weeks or more. You can usually get an electronically filed refund in less than three weeks – even faster if you choose direct deposit.1

Although direct deposit is faster, you should still expect to wait a few extra days for the funds to show up in your account. Depending on your financial institution, your waiting time may vary.

To e-file, you can file online through the IRS Free File tool.

When e-filing, you'll indicate how you want to receive your payment. While direct deposit is the most popular, there are several ways to receive your federal tax refund:1

Direct deposit (you can split this among up to three separate financial accounts)

Paper check

Prepaid debit card

Mobile payments app

Contribution to a traditional IRA, Roth IRA, or SEP-IRA

Purchase of up to $5,000 in U.S. Savings Bonds2

Free Online Tax Filing: File 100% for free, max out your tax refund guaranteed3, and get your federal tax refund up to 5 days early* when you direct deposit it with Chime.

If you're a Chime member, you can choose to direct deposit your refund into your Chime account. Just input your Chime Checking Account number and corresponding routing number, and that's it!

From there, you just have to wait for your refund to show up in your account. Enable notifications and, once your refund is available, Chime will send you a notification. This way, you'll know that the money is there right when you receive it.

Not too fast: Filing your taxes as early as possible certainly gets you your refund faster, but make sure you take advantage of all the tax write-offs you're eligible for.

2025 tax year refund schedule

How soon you're likely to receive your refund in 2026 for the 2025 tax year depends in part on the IRS schedule. This schedule varies depending on:

When you file: Filing earlier in the year may help you get a refund sooner. If you file closer to the deadline, the IRS might have a considerable amount of backlogged returns to sort through.

How you file: If you file electronically, you can get your return in about three weeks.1Note that it may take a couple of days for the IRS to receive your return, even when you e-file.

What credits you claim: When you claim certain tax credits, like the Child Tax Credit or the Estimated Income Tax Credit, this can change the timing of your tax refund.1

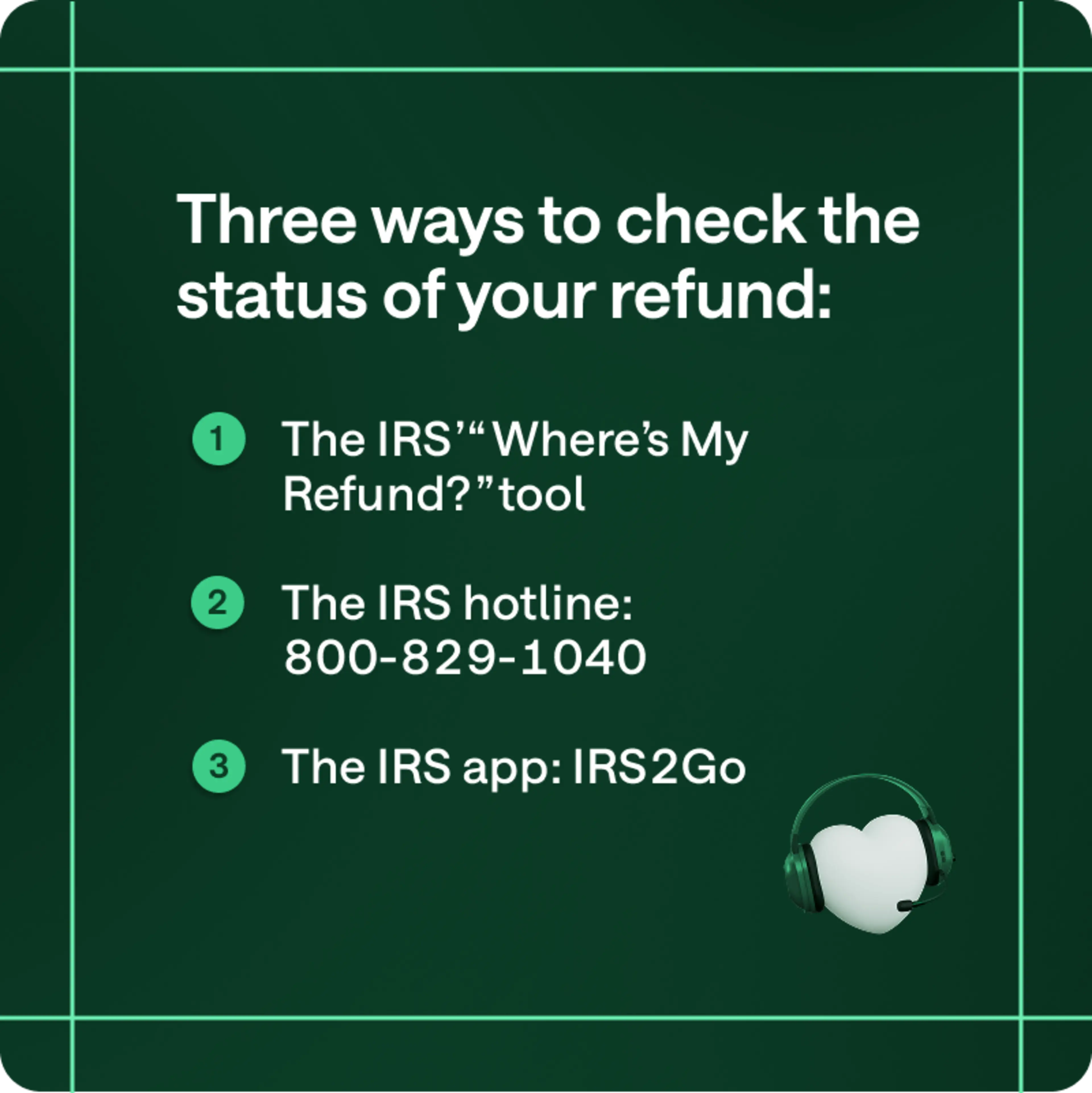

How do I check my tax refund status?

If at any point after filing, you're curious about your tax refund status you can use one of the following government tools:

Use the IRS refund status tracker tool: The IRS's "Where's My Refund?" tool is a quick and easy way to check the status of your tax refund. This will help you monitor your refund status and give you a better idea of when to expect your deposit.

Call the IRS to check the status of your refund: The IRS hotline number is 800-829-1040. Again, you will need to provide your Social Security number, tax filing status, and the amount of the refund you expect.

Use the free IRS app called IRS2Go: After downloading the app, enter the required information to receive an update. It's never been easier to check your tax status while on the go!

To check the status of your tax refund, you'll need the following items:4

Social Security number or individual taxpayer identification number (ITIN)

Filing status

The exact refund amount on your return

What to do if you don't receive your tax refund

There are a few reasons you might not receive your IRS tax refund:

If your tax return has any personal information errors, like misspelled names, incorrect Social Security numbers, unsigned forms, or incorrect account information, this can delay your refund.

It's also possible your return contains calculation errors. To avoid mistakes, carefully review your tax return before you click submit. If a tax preparer is completing your return for you, make sure they have all of your correct information.

Another reason for a potential hold-up is if you were a victim of identity theft or fraud. In this case, the IRS may hold your return until it can work with you to resolve the issue.

If you didn't receive your refund, you can use the "Where's My Refund?" tool, call the IRS at 800-829-1040, or check the IRS app IRS2Go for more information.

Track your tax refund status in 2026

Waiting for your tax refund can feel stressful, especially if Uncle Sam owes you a big chunk of change. Choose direct deposit for the fastest refund, and file as soon as possible to get your refund earlier in the year. Don't forget that you can use free IRS resources to track your tax refund status after filing.

Most importantly, make sure that you set up direct deposit correctly. Getting your tax refund can make a huge difference – here's what to do if your tax refund was deposited into the wrong account.

Looking for more tax tips? Here are some tax deductions you might not have thought of.