Updated: November 2025 — The IRS has not yet published its 2025 filing updates. This page will be refreshed as soon as new guidance is released.

When planning for a financially secure retirement, you might consider two investment vehicles: individual retirement accounts (IRAs) and 401(k)s. Both help you save for retirement, but they come with their own sets of rules and benefits. Understanding the difference between an IRA and 401(k) can help increase your retirement savings.

An IRA is a tax-advantaged account that you set up independently to save for retirement. It offers a variety of investment options, including stocks, bonds, and mutual funds.

A 401(k) is a retirement savings plan sponsored by your employer. It allows you to save a portion of your paycheck before taxes. Often, employers match your contributions. Keep reading to learn the key differences between these two investment vehicles and how to use them most effectively in your retirement planning.

Comparing IRAs and 401(k)s

Navigating the labyrinth of retirement account options can be overwhelming at first. But understanding the distinctions between an IRA and a 401(k) can help you confidently grow your retirement nest egg.

Before you decide the best retirement account for you, let's compare the two. How is a 401k different from an individual retirement account (IRA)? 1,2

As you can see, both types of accounts offer savings benefits. But let's explore more about each, so you can determine if you should use one or both in your retirement plan.

IRA | 401(k) | |

|---|---|---|

2025 Contribution Limits (Under 50) | $7,0003 | $23,5003 |

2025 Catch-Up Limits (50 and older) | $8,0003 | $31,0003 |

2025 Secure 2.0 Catch-Up Limits (61-63) | $1,0004 | $11,2504 |

Contributions Source | You determine your own contributions | Automatic paycheck deductions with potential employer matches |

Investment Options | Diverse asset choices (stocks, mutual funds, etc.) | Typically limited to a few funds selected by the administrator |

Account Setup | You set up your own account | Established by employers |

Account Types | Traditional, Roth, SEP, and SIMPLE | Roth and traditional 401(k) |

Required Minimum Distributions (RMDs) | Start at age 73 or 75, depending on birth year (Roth IRAs exempt) | Start at age 73 or 75, depending on birth year (Roth 401(k)s subject to minimum distributions) |

Benefits of choosing IRA vs 401(k)

Deciding between an individual retirement account (IRA) and a 401(k) is essential for developing the right retirement fund strategy. Both investment vehicles offer distinct tax advantages and contribution limits.

Here are six elements to consider when deciding between the two retirement accounts:

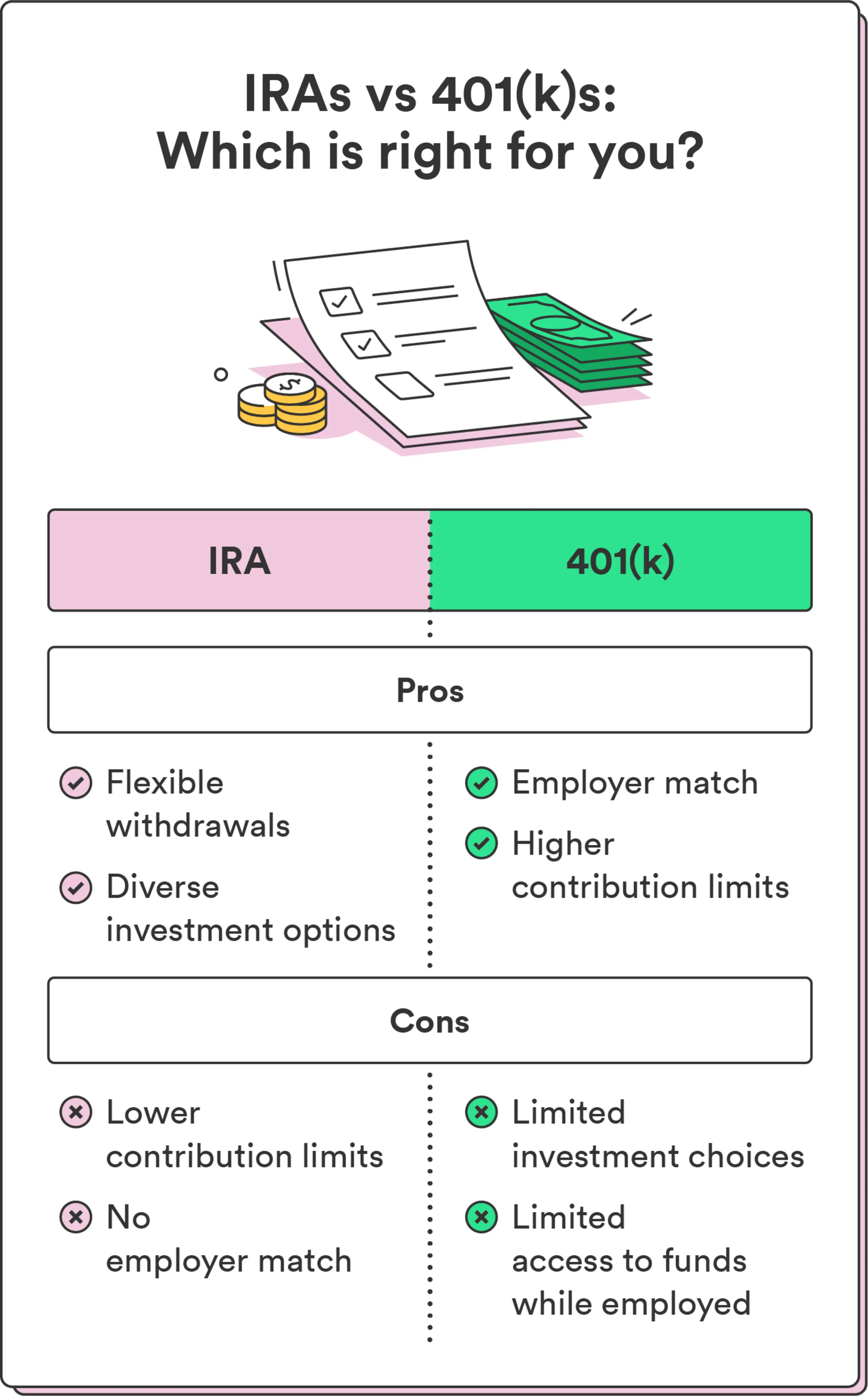

Flexibility in contribution limits. The IRA offers a degree of financial flexibility that is helpful for those with variable income streams. If you're under 50, the maximum annual contribution to your IRA is $7,000 in 2025.3 Because of the catch-up provisions allowed by federal law, an IRA has an annual contribution limit of $8,000 in 2025 for those over age 50. That's $7,000 plus an additional $1,000 in "catch-up" contributions for those 50 and over trying to make up for not contributing enough to their IRAs in earlier years to reach their retirement savings goals. IRAs also allow you to adjust contributions depending on your circumstances each year.3,4

Diverse investment options. One of the clearest benefits of an IRA is the range of investment options. Unlike 401(k)s, which often limit investors to a selection of funds, IRAs offer a range of assets like stocks, bonds, mutual funds, and index funds. This diversity can help you adopt a more strategic approach to retirement planning, like investing based on your values.3

Dependency on employer match. The matching contributions many employers offer with their 401(k)s is appealing, as this is not available with IRAs. Employer matches are beneficial, but their absence in an IRA means you maintain control over your retirement contributions. You're also not dependent on the employer's health or your job to build your retirement savings. This independence can especially appeal to freelancers and those who prefer full control over their retirement strategy.3

Avoiding administrative fees. Consider the long-term impact of administrative fees often associated with 401(k) plans. IRAs typically come with lower fees, particularly when you use brokerage firms offering low-cost index funds. In the long term, these lower fees can affect your investment returns.3

Tax benefits of traditional IRAs. Roth or traditional IRAs offer their own set of tax advantages. Contributions to a traditional IRA may be tax deductible, reducing your taxable income for the contribution year.3

Pre-tax benefit consideration. Both 401(k)s and traditional IRAs offer the advantage of pre-tax contributions. This feature could allow you to reduce your taxable income, providing tax relief that can be valuable for those in higher tax brackets.3

By understanding these distinct advantages, you can make a more informed decision that aligns closely with your long-term financial objectives. Plus, they can help you answer the question, "Is an IRA better than a 401k?"

401(k) match vs. no match: How it affects you

The availability or lack of a 401(k) employer match often makes a difference in the way you shape your retirement investment strategy. It can influence how much you contribute and where you allocate your money for growth. It also can help you decide when it's time to max out your IRA contribution if you have both account types.

If your employer matches your 401(k), you should:

1. Maximize your employer match

Securing an employer match on your 401(k) contributions is like receiving additional income without extra work. If your employer matches your contributions, take advantage of the full employer match to increase the value of your retirement investment fund.

2. Max out IRA contributions

Once you get your full employer match in your 401(k), the next logical step is to maximize contributions to an IRA. That's because your IRA typically offers a broader range of investment options. They can provide opportunities to diversify your portfolio and potentially realize higher returns.

3. Consider 401(k) after IRA maxed

If you've reached the annual contribution limit for your IRA and still have extra funds, revisit your 401(k) options. Additional 401(k) contributions can further supplement your retirement savings and offer tax advantages.

Actions to take if your employer doesn't match your 401(k) include:

1. Prioritize IRA contributions

Without an employer match, the IRA may be an even more important opportunity for retirement savings. The IRA's lower fees and broader investment options also make it a preferable first choice for maximizing contributions.

2. Consider 401(k) after IRA maxed

Even if your employer does not offer a matching contribution, a 401(k) remains a viable path to additional retirement savings. The tax benefits associated with 401(k) contributions still can make it a worthwhile investment after you've maxed out your IRA annual contributions.3

How to choose between a 401(k) and IRA

Determining whether to invest in a 401(k) or IRA depends on a few factors, including your current financial standing, the benefits provided by your employer, if you're self-employed, and your long-term investment objectives.

The argument for a 401(k)

If your employer offers a 401(k)-matching program, take advantage of this opportunity. It's like getting extra income without doing additional work. Acquiring the extra contributions from your employer is one of the main benefits of a 401(k).

Another benefit is that employers typically offer this account type, so there is less manual setup or maintenance needed.

The argument for an IRA

IRAs often provide a broader array of investment options compared to 401(k)s, which are a limited range of mutual funds pre-selected by your employer. This may benefit you if you want more control over the fund's investment strategies or for self-employed individuals who don't have access to employer-sponsored plans.

401(k) plans often have higher administrative fees, which can diminish potential gains. IRAs usually have lower fees. With the latter, you won't get charged commissions or sales charges for selling the shares in the fund.

IRAs offer more flexibility for tax planning. For instance, Roth IRAs allow for tax-free withdrawals upon retirement, providing a hedge against potential tax rate increases in the future. Just remember that early withdrawals from a 401(k) or IRA are unlikely to be tax-free.

Both IRAs and 401(k)s are smart choices

Investing in IRAs and 401(k)s offers valuable strategies for securing your financial future.

401(k)s are an excellent vehicle for retirement savings, especially if your employer offers matching contributions. However, IRAs offer greater flexibility in investment choices and tax planning.

Your choice between the two should be a strategic decision based on an evaluation of your financial situation, investment goals, and the specific features of each type of account.1,2

Discover more retirement options and learn how to plan for retirement in your 20s and 30s.