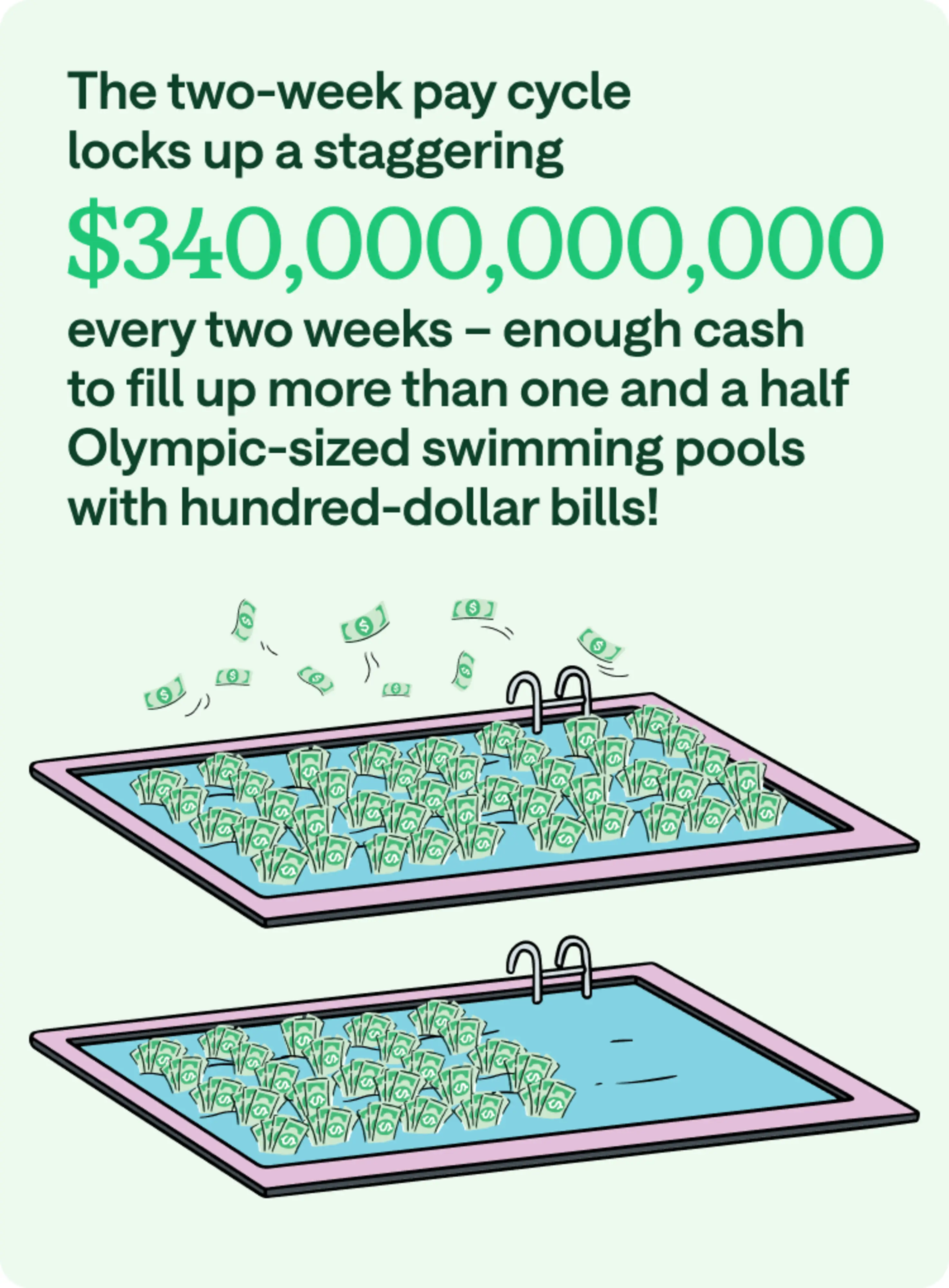

The two-week pay cycle, a common practice in the U.S. where employees are paid bi-weekly throughout the year, locks up a staggering $340,000,000,000 every two weeks while workers wait to get paid.1 That's enough cash to fill up more than one and a half Olympic-sized swimming pools with hundred-dollar bills!

With modern technology changing the way Americans unlock financial progress™, it may be time to think outside this status-quo pay structure and explore how we can move beyond the wait for payday.

For over 80 years, the way Americans are paid has remained largely the same, while other technologies have improved exponentially. Think about the strides we've made since the first digital computer that took up an entire room, or the first microwave that was the size of a stove and weighed over 750 pounds.2 Why have we not made similar progress when it comes to the pay cycle?

Let's find out why the two-week pay cycle is still being used and explore alternate options that may allow you to access your hard-earned pay in a new way.

What is the two-week pay cycle?

A two-week pay cycle, also known as a bi-weekly pay schedule, is a payroll system that gives employees their wages every two weeks. In this system, workers usually receive 26 paychecks per year.

This schedule is helpful for employers and predictable for employees, but what if you want to manage your money week to week? The wait for payday could mean relying on credit cards or payday loans for expenses that can't wait or make time-sensitive purchases like flights.

Despite advancements in payroll technology, the two-week pay cycle remains a standard due to its historical roots. Let's travel back in time…

Why is the two-week pay cycle the norm?

The two-week pay cycle became more common after the New Deal's 1938 Fair Labor Standards Act, which introduced the minimum wage and child labor standards.3 During that time, payroll processing was done manually, and paychecks had to be calculated, printed, and distributed to workers by hand.

During World War II, the Revenue Act was passed to help fund the war with income taxes.4 This made manually calculating pay slips even more complicated for businesses, as workers wanted to understand their take-home pay after deductions like social security and income tax.

The two-week pay cycle lightened the workload for companies so they could spend less time writing pay slips. Over many decades, employers and employees became used to the stability and predictability of receiving paychecks every two weeks.

Despite the evolution of technology that allows for real-time payroll processing, the two-week pay cycle persists largely due to its history in American business culture and labor practices. It's a system we haven't called into question in nearly 100 years.

Pros and cons of the two-week pay cycle

The bi-weekly pay schedule has its pros and cons. While it may be easier for employers to plan their bookkeeping around a two-week cycle, the system can place a burden on workers.

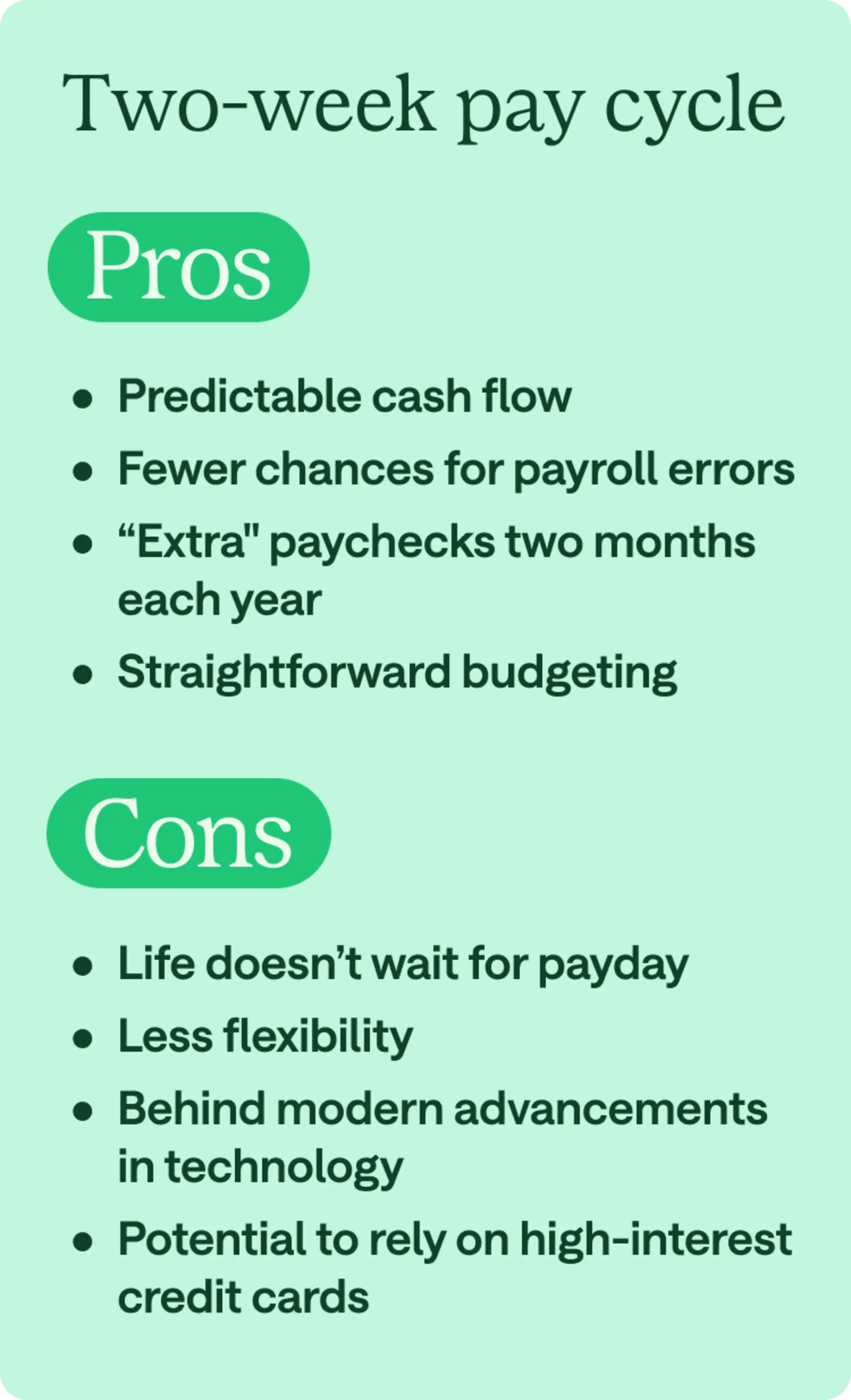

Pros of the two-week pay cycle

Predictable cash flow

Fewer chances for payroll errors

"Extra" paychecks two months each year

Straightforward budgeting

Cons of the two-week pay cycle

Life doesn't wait for payday

Less flexibility

Behind modern advancements in technology

Potential to rely on high-interest credit cards

Chime's own research shows that, for 60% of Americans, the two-week pay cycle leads to an increase in "pay paralysis," the wave of anxiety or fear due to low funds between pay cycles.5

In addition, almost half of Americans have had to skip a once-in-a-lifetime event like a wedding to avoid financial hardship.5

Thinking beyond the two-week pay cycle with MyPay

Research from the Federal Reserve notes that 40% of adults in the U.S. don't have enough savings to cover a $400 emergency bill, and almost 10% of workers making at least $100,000 are struggling financially.6 This dominant pay structure is keeping paychecks locked up for too long, when you should be able to tap into your pay without having to wait.

Since our founding, Chime has provided innovative, easy-to-understand financial service products that address the liquidity and credit needs of everyday people. Chime first pioneered Get Pay Early, allowing members to access their direct deposit up to two days early.7

Now, to help Americans unlock their pay beyond the restrictions of the two-week pay cycle, Chime has unveiled MyPay™: a revolutionary new way to get paid when you say™ that allows eligible members to access up to $5008 of their pay, including government benefits, before payday, with no interest9, no credit check, and no mandatory fees.

If you're an eligible Chime member and enroll in MyPay, you can get part of your pay within 24 hours for free or get it instantly for $2 to $5 per advance.

Whether it's an unexpected trip to the vet or taking advantage of a last-minute offer for concert tickets, members can access their pay on their own terms and navigate whatever life throws their way, beyond the traditional two-week wait for payday.

Dive deeper into MyPay: find out why Gen Z wants on-demand pay.