Log in

Log in

Knowing your discretionary income is useful for creating a budget and for determining your eligibility for lower student loan payments.

In this guide, we’ll break down how discretionary income works, what influences it, and how it can help you manage student loan debt more effectively.

What is discretionary income?

Think of discretionary income as the cash you have to spend or stash away once you’ve handled the basics, like rent, taxes, utilities, and other non-negotiable bills.

While discretionary income is useful for budgeting, it’s also crucial in determining student loan payments for income-driven repayment (IDR) plans.

Examples of discretionary expenses

Discretionary expenses are nonessential costs that fall outside the realm of basic necessities. These expenses can vary widely, but some common examples include:

- Travel: Travel and vacation expenses, including flights and hotels.

- Dining out: Eating at restaurants, ordering takeout, etc.

- Entertainment: Expenses related to movies, concerts, sporting events, streaming services, or other forms of entertainment.

- Hobbies: Spending on personal interests like photography, art, gaming, or other recreational activities.

- Shopping: Purchases of nonessential items, like clothing, electronics, or home decor.

- Gifts: Purchasing gifts for special occasions or charitable donations.

What is discretionary income for student loans?

If you’re under an IDR plan, the federal government uses your discretionary income to see how much you can afford in monthly student loan payments. This calculation considers the difference between your income and the federal poverty guidelines, often multiplied by a specific percentage.

How to calculate discretionary income

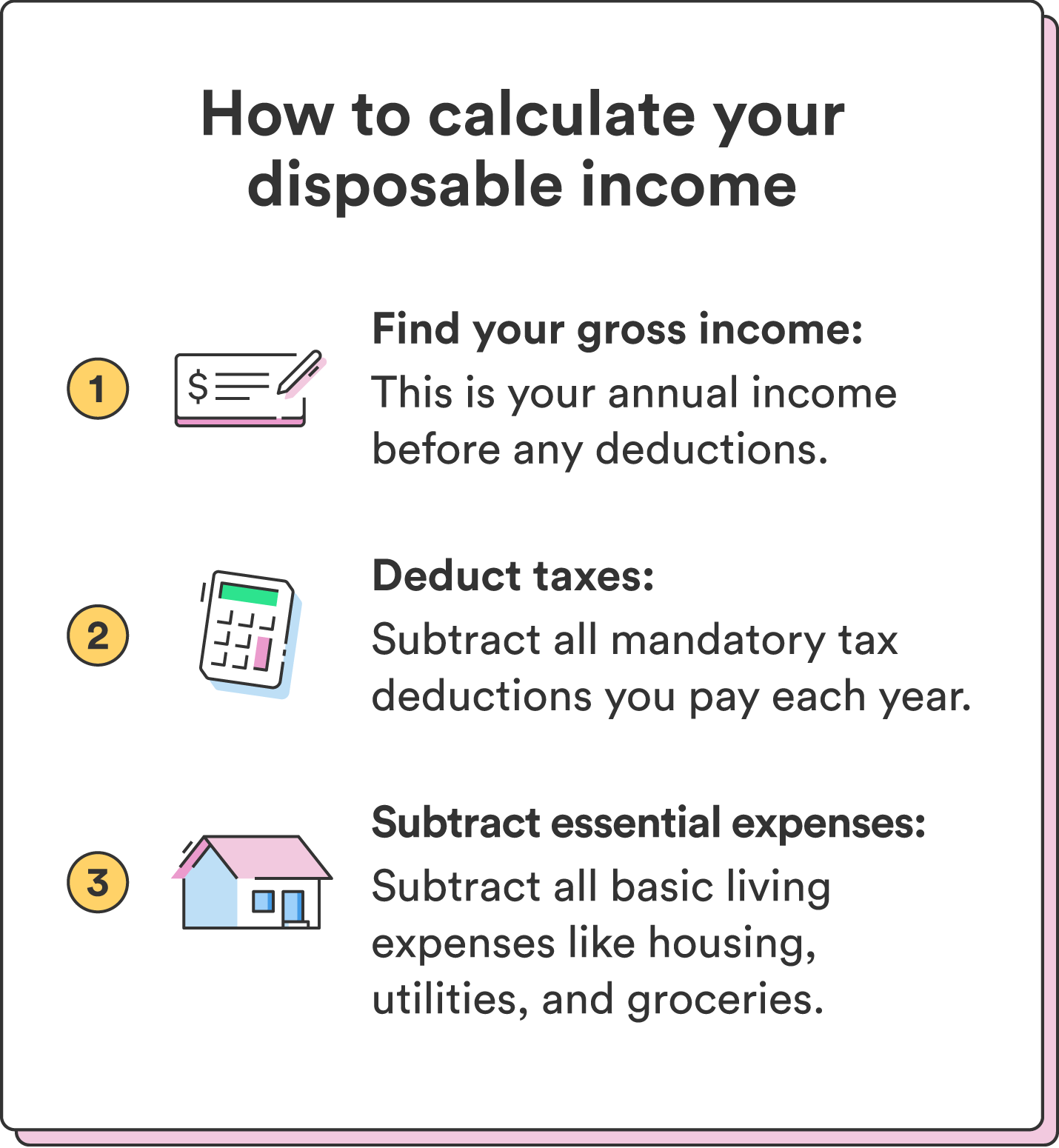

The information you’ll need to calculate discretionary will vary if you’re using discretionary income for student loan purposes. But for general budgeting purposes, here’s what you’ll need:

- Gross income: This is your annual income before any deductions, including your salary, bonuses, and any other sources of earnings.

- Taxes: List all mandatory tax deductions you pay each year, including federal and state income taxes, Social Security, and Medicare contributions. Your employer may automatically deduct these from your paycheck – read your pay stubs to see what deductions are taken from your paycheck.

- Essential expenses: List all of your basic living expenses, like housing costs (rent or mortgage), utilities (electricity, water, gas), groceries, transportation expenses (gas, public transportation, parking), and essential insurance (health, auto, etc).

If you’re calculating your discretionary income just for budgeting purposes, subtract your total tax deductions and essential expenses from your gross income. The remaining amount is your discretionary income.

To calculate discretionary income for student loans, the U.S. Department of Education uses your Adjusted Gross Income (AGI), which already accounts for your tax deductions and exemptions.

You can find your AGI on your most recent federal income tax return. For the 2023 tax year, your AGI is on Line 11 on IRS form 1040, 1040-SR, or 1040-NR from your 2022 IRS tax return.¹ Follow the steps below to calculate your discretionary income for student loans.

Chime tip: If you need help finding your previous tax returns, you can find them through your tax preparation software, tax preparer, or the IRS website if you filed online. If you filed a paper return, you can find your AGI on the physical return.

1. Determine the Federal Poverty Guideline for your household

Once you know your AGI, you must find the federal poverty guideline for your state and family size. The “poverty guideline” is a threshold amount based on your where you live and how many people are in your household.

You can find the Poverty Guidelines on the Department of Health and Human Services (HHS) website and below.²

| Number of people in household² | 2023 poverty guidelines (48 contiguous U.S. states and the District of Columbia)² |

|---|---|

| 1 | $14,580 |

| 2 | $19,720 |

| 3 | $24,860 |

| 4 | $30,000 |

| 5 | $35,140 |

| 6 | $40,280 |

| 7 | $45,420 |

| 8 | $50,560 |

If you have more than eight people in your household, add $5,140 per additional person.

| Number of people in household² | 2023 poverty guidelines for Alaska² |

|---|---|

| 1 | $18,210 |

| 2 | $24,640 |

| 3 | $31,070 |

| 4 | $37,500 |

| 5 | $43,930 |

| 6 | $50,360 |

| 7 | $56,790 |

| 8 | $63,220 |

If you have more than eight people in your household, add $6,430 per additional person.

| Number of people in household² | 2023 poverty guidelines for Hawaii² |

|---|---|

| 1 | $16,770 |

| 2 | $22,680 |

| 3 | $28,590 |

| 4 | $34,500 |

| 5 | $40,410 |

| 6 | $46,320 |

| 7 | $52,230 |

| 8 | $58,140 |

If you have more than eight people in your household, add $5,910 per additional person.

2. Multiply the amount by 1.5 (150%)

Once you have your poverty guideline, multiply that number by 1.5 (150%). Then, subtract this number from your AGI found in step two.

If you’re using an income-contingent repayment plan, you don’t need to multiply your poverty guideline amount by 1.5. (That’s because this type of repayment plan uses 100% of the federal poverty guideline amount instead of 150%, so the multiplier isn’t necessary).²

3. Subtract the result from your adjusted gross income

After finding your poverty guideline and multiplying that number by 1.5 (150%), subtract this number from your AGI.

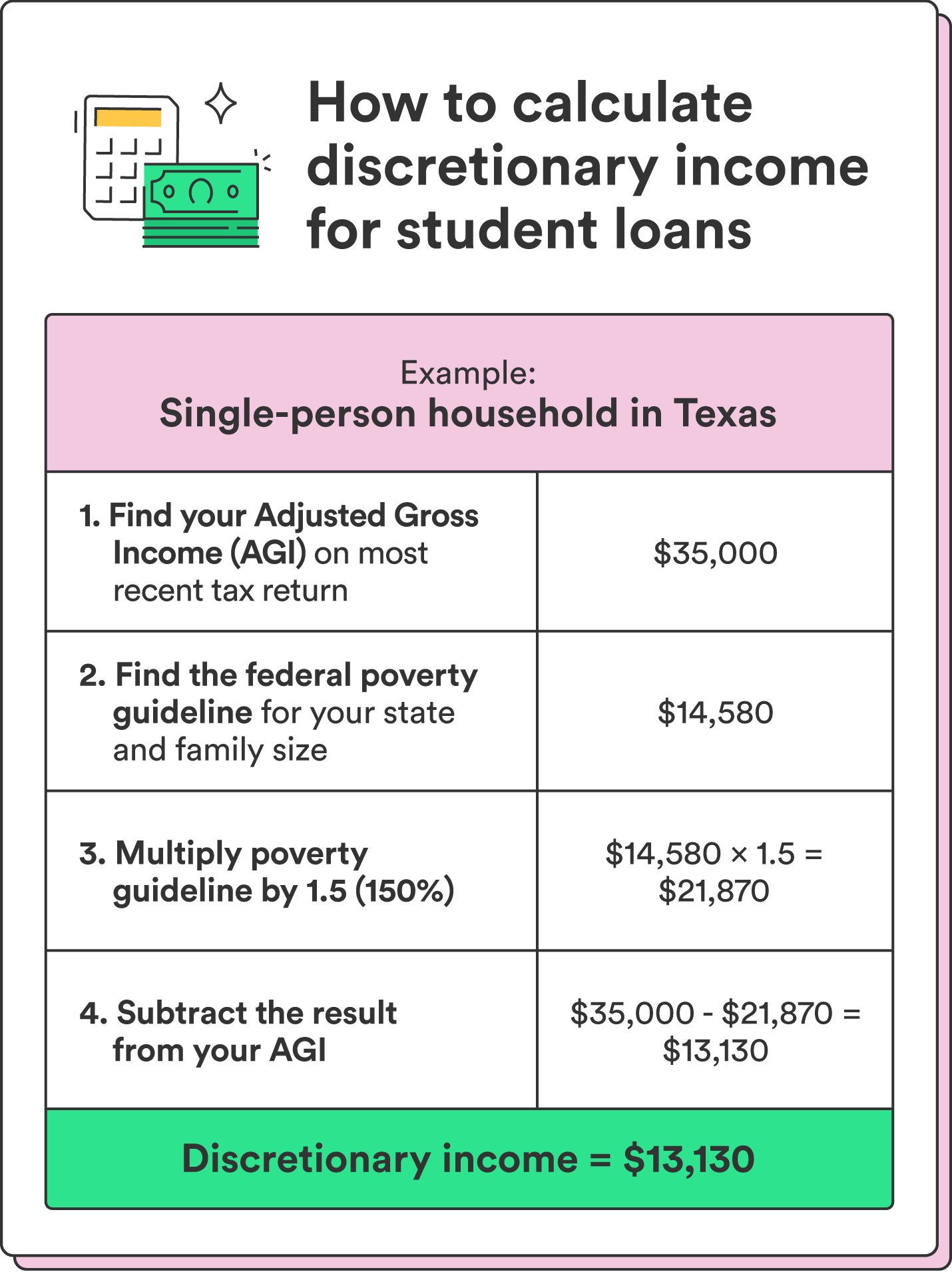

Example discretionary income calculation

Let’s break down a hypothetical calculation to figure out discretionary income for student loans. For this example, let’s say you’re single, live in Texas, and your AGI is $35,000 per year.

Here’s an overview of the calculation:

- 2023 federal poverty guideline (for a single-person household in Texas): $14,580

- Multiply your poverty guideline by 1.5 (150%): 1.5 x $14,580 = $21,870

- Subtract that number from your AGI: $35,000 – $21,870 = $13,130

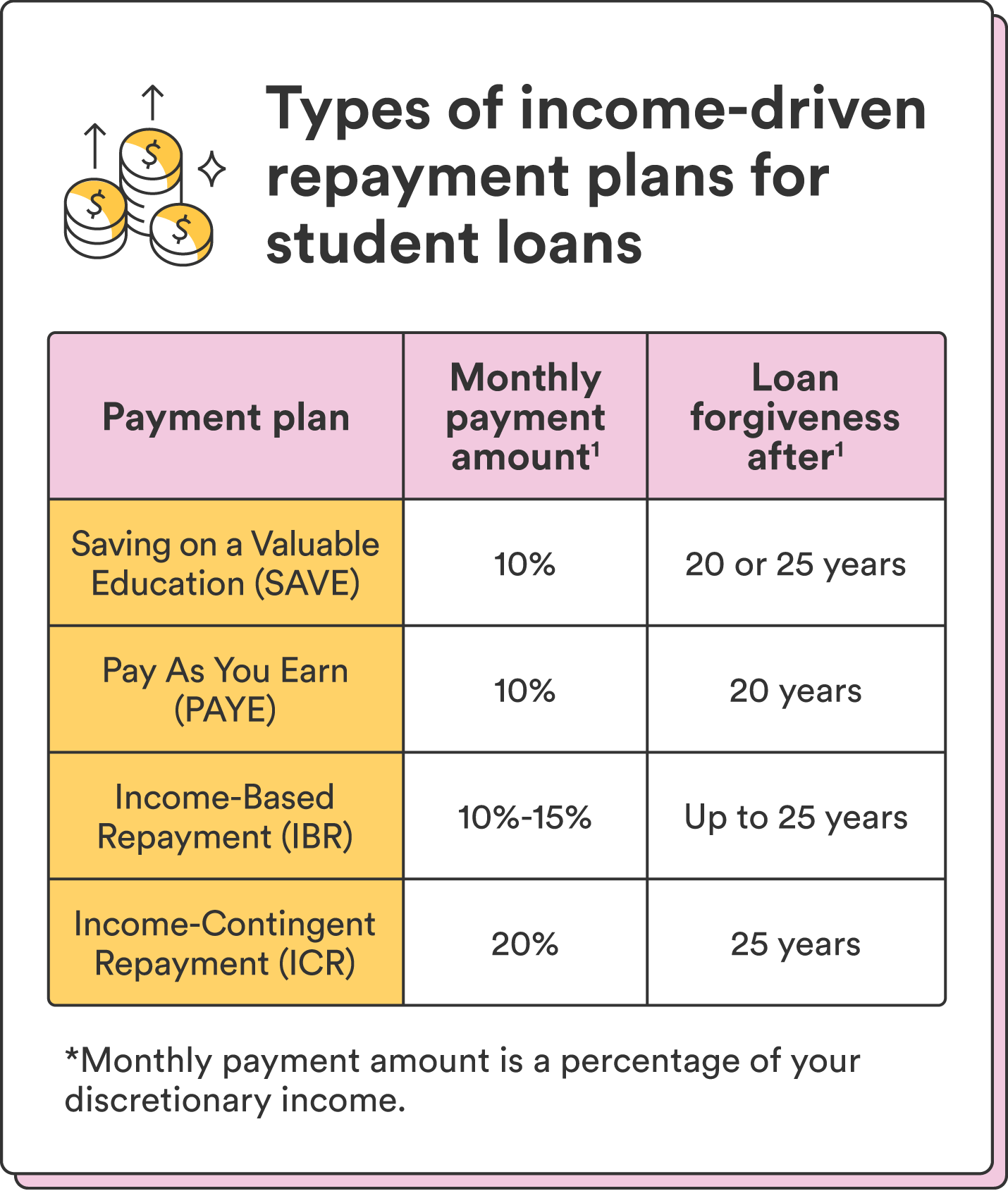

In this example, your discretionary income is $13,130. Use this amount to determine your monthly student loan payments under income-driven repayment plans. See a full breakdown below:

Discretionary income vs. disposable income

Disposable income is simply the money you have after taxes have been deducted from your gross income. On the other hand, discretionary income goes a step further by subtracting all your essential bills and expenses (think rent, utilities, or your car payment). Discretionary income is the money that remains after your basic needs are covered.

Can discretionary income change?

Your discretionary income isn’t set in stone; it can fluctuate over time for various reasons and can also impact your monthly payments on IDR plans.

Here are some common reasons your discretionary income may change:

- Relocation to a different state: If you move to a new state outside of the 48 contiguous U.S. states, the poverty guideline for your household size may change since Alaska and Hawaii have different poverty guidelines.

- Salary changes: Any changes in your income, whether an increase or decrease, can alter your AGI and your discretionary income. If your income increases, you’ll likely see your monthly IDR payments increase; if your salary decreases, your monthly payments may also decrease.

- Changes in family size or marital status: Getting married, having children, or experiencing other changes in family size can impact your discretionary income, as the federal poverty guidelines increase in proportion to the number of people in your household.

- Change in poverty guidelines: The federal poverty guidelines are updated annually. A change in these guidelines can impact your discretionary income calculation, even if your financial situation remains unchanged.4

Manage student loans and other finances with confidence

Once you have your discretionary income calculations nailed down, you can use them to clarify your budget by knowing exactly how much money you have available once the essentials are covered. You can also manage your student loans more effectively (and maybe even lower your monthly payments).

Take the first step today – calculate your discretionary income, set meaningful financial goals, and move closer to building a secure and balanced financial future.

Read more about student loan debt forgiveness.