Are you fed up with bank fees? You aren't alone. American consumers still pay billions per year for ATM fees, overdrafts, and monthly maintenance fees.1

What's most frustrating is that these fees may come as a surprise. Many seem hidden and happen without people realizing it, often when they need the money for something else.

We surveyed 2,000 Americans2 to discover what bank and credit card fees consumers deal with most, and how these fees impact them. Nearly 1 in 3 people recall being charged at least one bank fee over the past three months, with the average person recalling being charged $78 during this time.

Bank and credit card fees still impact millions

Overall, some bank fees are declining. According to Bankrate, overdraft and non-sufficient funds (NSF) fees have declined significantly since 2022.3 In addition, their study found that 45% of non-interest earning checking accounts are free, meaning they don't charge a monthly fee or require a minimum balance.

However, based on Chime's new data, for the Americans who are still paying these fees, it certainly doesn't feel like bank accounts are becoming more affordable. 32% of consumers who were charged a fee in the past three months believe fees have increased over the past two years.

What could be driving this perception is that while some fees have decreased recently, out-of-network ATM fees are at a record high of $4.73 per transaction.3 18% of consumers have paid an out-of-network ATM fee in the past three months, making it by far the most common fee. Chime's out-of-network fee, for reference, is $2.50, which is $2+ less than the average out-of-network withdrawal fee.

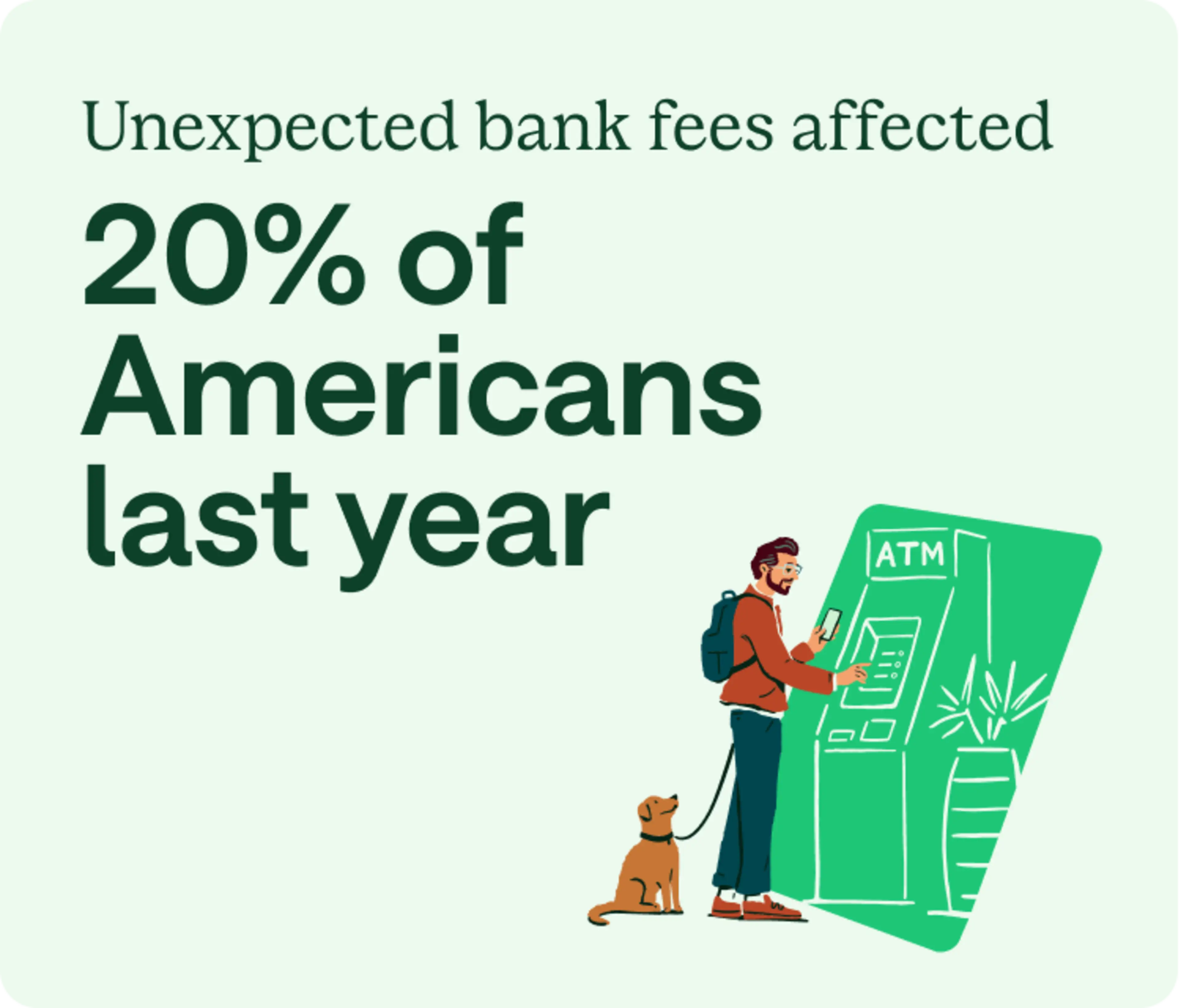

Bank fees are already frustrating, but they feel even worse when they come as a surprise. 20% of survey respondents reported being surprised by an unexpected bank fee in the past year.

For context, let's assume everyone banks somewhere that charges the described fees and also banks in a way where they would be charged those fees. If you were to take the US adult population and multiply it by 20%, that would mean approximately 52 million Americans have been affected by an unexpected bank fee in the past year.

As inflation strains the typical household's budget, getting caught off-guard by extra fees is a curveball many consumers cannot afford.

How people perceive fee fairness

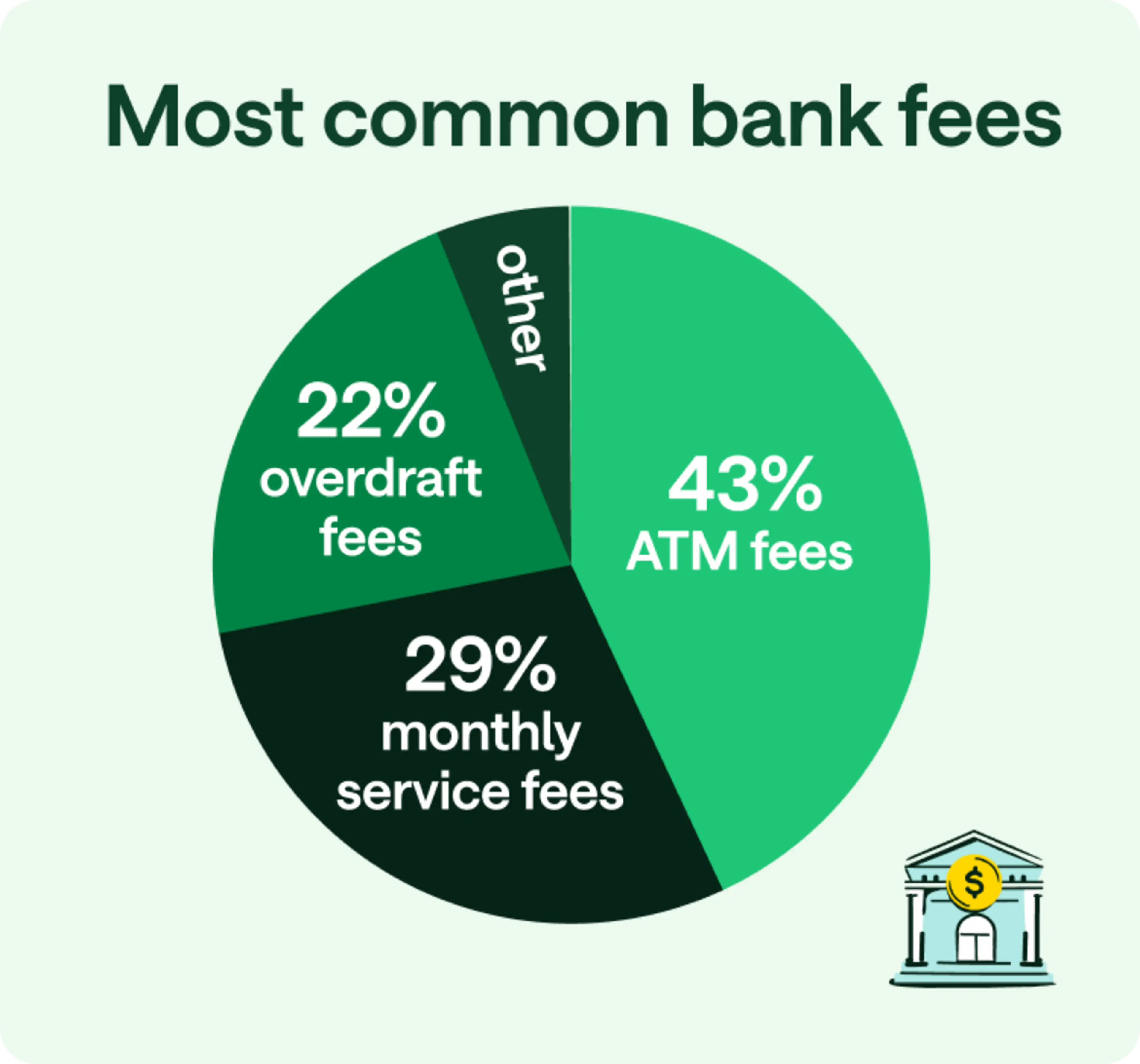

While bank fees overall have come down over the past couple of years, a few still pop up regularly. The top three most common bank fees reported by people surveyed were:

43% of consumers surveyed reported paying ATM fees over the past three months, with an average total cost of $13.40

29% of consumers surveyed reported paying monthly service and maintenance fees with an average total cost of $18.60

22% of consumers surveyed reported paying overdraft fees with an average total cost of $31.80

How banks make money

Banks can make money in a number of ways, including account fees, credit card fees, and by earning interest by lending your cash for mortgages, car loans, and small business loans.

Consumers feel like the most common account fees, like monthly fees and ATM fees, are an unfair way for banks to earn money. Only 18% of respondents thought ATM fees were a fair way for banks to make money. Even fewer people – 14% – thought monthly maintenance fees were fair.

When asked about banks' general income sources, not all revenue streams were seen as bad – 54% of people feel that banks earning interest off their deposits is fair. Consumers also reported being more accepting of fees for services like printing checks and wire transfers.

Consumers also feel common bank fees aren't very transparent – only 35% of respondents thought that the fees charged by their financial institutions were "very" or "extremely" transparent. This means 65% of respondents thought that their financial institutions need to do better about being up front about the fees they charge.

Consumers did not have the same level of frustration when banks earned money from purchases on their debit and credit cards, as 44% thought this was fair. Unsurprisingly, people can be upset by the sometimes confusing nature of bank fees.

The emotional damage from unexpected bank fees

Getting caught off-guard with a bank fee is an unpleasant emotional experience. People who got hit with an unexpected bank fee in the past year said they felt stressed, frustrated, anxious, helpless, and depressed when charged an unexpected bank fee.

35% of people who were charged an unexpected bank fee in the past year reported feeling stressed when recalling it, and 10% reported feeling depressed.

Bank fees can become an ongoing source of stress. 28% of people who have faced an unexpected bank fee worry about future fees, compared to only 9% who haven't.

Nearly half of consumers (47%) check their accounts at least weekly to ensure they haven't been hit with a surprise bank fee.

While monitoring your account can be a smart money habit, it shouldn't be done out of fear.

In the end, unexpected bank fees can greatly affect your emotional health, your perceptions of your financial situation, and your ability to reach long-term goals. When people are worried about their daily budget getting thrown off by a surprise fee, how can they plan for the future?

Money that should be spent elsewhere

Bank fees can add up quickly. That's money that could and should be spent elsewhere. Consumers say that without bank fees, they would have extra money to:

Buy more groceries (38%)

Pay off debt (36%)

Build an emergency fund (31%)

Take care of family and friends (22%)

Go out more (18%)

Add to retirement savings (17%)

Use credit cards less (14%)

All those activities and goals sound more fulfilling, helpful, and enjoyable than paying money for bank services that could be free.

Confusing fees that customers perceive as hidden may cost banks business in the long run. 41% of consumers said they would keep more money in a checking account or savings account if it weren't for fees. Banks are leaving opportunities for earning interest on the table when people close accounts due to frustration from fees.

41% of customers who were charged an unexpected bank fee last year closed their account. Considering that it costs banks roughly $561 to acquire each new retail customer, they are likely losing money by driving away existing account holders with unexpected fees.4

Unexpected bank fees disproportionality fall on minority groups

Unexpected bank fees were not experienced equally in terms of demographics in our survey. Fees were more prominent among younger, Black, and Hispanic respondents.

Impact by generation

Younger Gen Z and Millennial consumers are roughly twice as likely to report getting hit with bank fees. Here's what share of each age group reported being charged different bank fees in the three months before our survey:

18-24 | 25-44 | 45-64 | 65+ | |

|---|---|---|---|---|

ATM fees | 20% | 27% | 16% | 7% |

Monthly service/maintenance fees | 7% | 19% | 12% | 5% |

Overdraft fees | 15% | 14% | 6% | 3% |

People typically build wealth over time. It makes sense that older Americans have more cash to meet monthly balance requirements and avoid overdrafts. Large-balance premium checking accounts often waive or reimburse out-of-network ATM fees, too. But you shouldn't have to be loaded to dodge these fees.

While a smaller share of senior consumers face bank fees, many still do, especially monthly service and ATM fees. It's a lifelong problem.

Chime tip: 18 to 44-year-olds are less likely to contact banks and ask to have fees removed, a strategy that could save them money. Don't hesitate to contact customer service if you get hit with an unexpected fee.

Impact by ethnicity

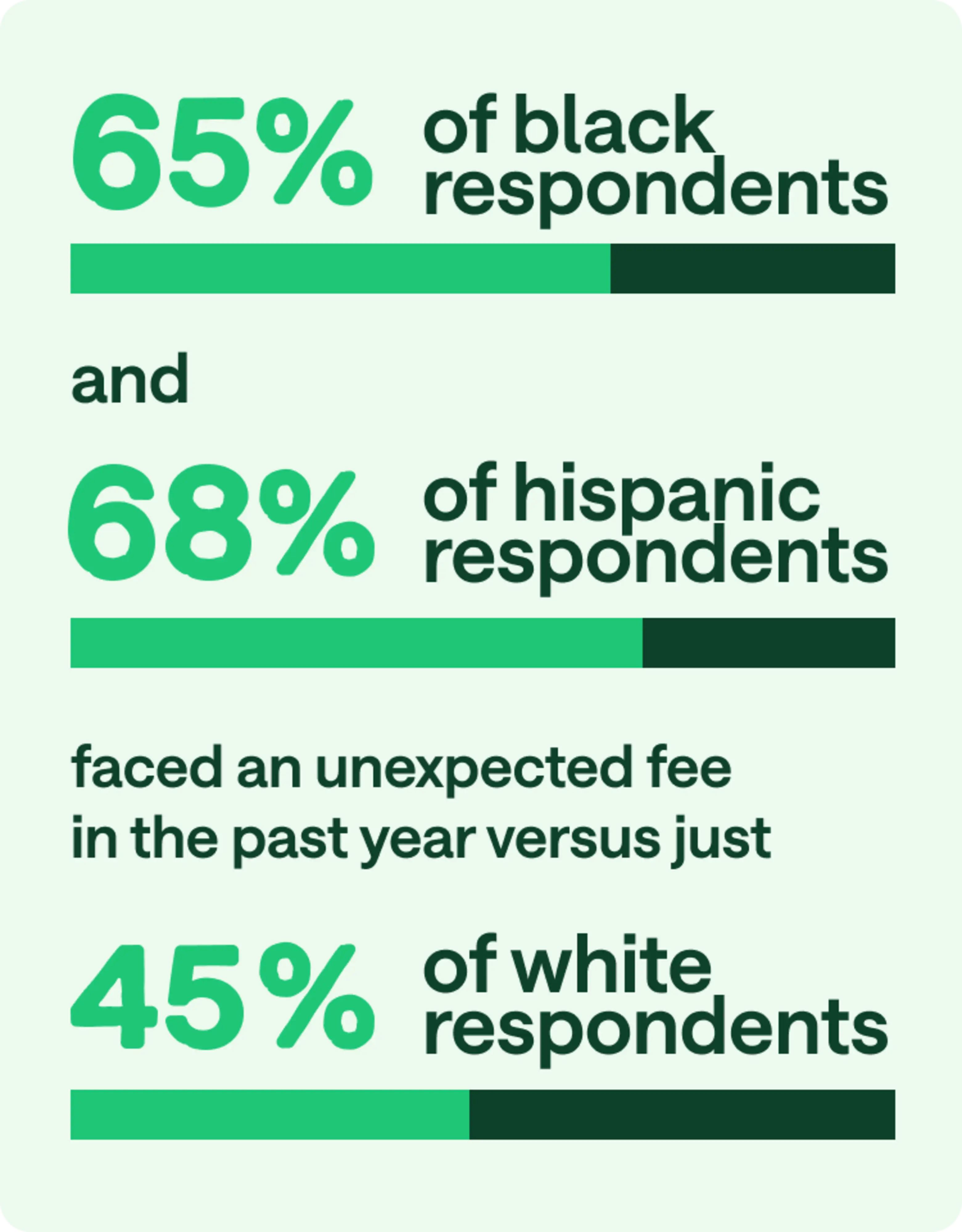

Bank fees are also not spread out evenly by race and ethnicity. Black and Hispanic consumers were more likely to report being hit by practically every bank and credit card fee compared to white and Asian consumers.

68% of Black and 65% of Hispanic respondents faced an unexpected fee in the past year, versus just 43% of white respondents. People identifying as Hispanic are also most likely to be "somewhat worried" to "extremely worried" about unexpected fees.

Given these gaps, it's no wonder that consumers in these categories were less likely to see bank fees as fair. For instance, 47% of white respondents believe overdraft fees are fair compared to 32% of Black respondents. 29% of white respondents think fees for printing checks are fair compared to 19% of Hispanic and 12% of Black respondents.

Chime: Banking That Has Your Back®

Unexpected bank fees might seem like a part of life, but they don't have to be. Online-only financial technology companies like Chime have made it our mission to help our members unlock financial progress™.

Our fee schedules (Stride Bank, N.A. and The Bancorp Bank, N.A.) with our partner banks are completely transparent. We have access to 50,000+ fee-free ATMs, but you can be assessed a $2.50 cash withdrawal fee if you use an out-of-network ATM. There's no fee for transactions at any Allpoint® or Visa® Plus Alliance ATMs, or at MoneyPass® ATMs located in a 7-Eleven location.

Chime doesn't charge overdraft fees, monthly maintenance fees, or foreign transaction fees. The only surprise you should expect is that empowering feeling when your direct deposit hits up to two days early.5

As frustration over bank fees continues to build, more people may try an option like Chime that bets big on their members instead of charging them with fees like overdraft fees or monthly account fees.