Gen Z isn't content to maintain the system they were born into: they want to redefine it. This applies to every aspect of their lives, including how they bank.

Most Gen Z's already have a bank account: 72% of Gen Z adults have a checking account, and 57% have a savings account.1 However, their parents or guardians likely set up these accounts for them.

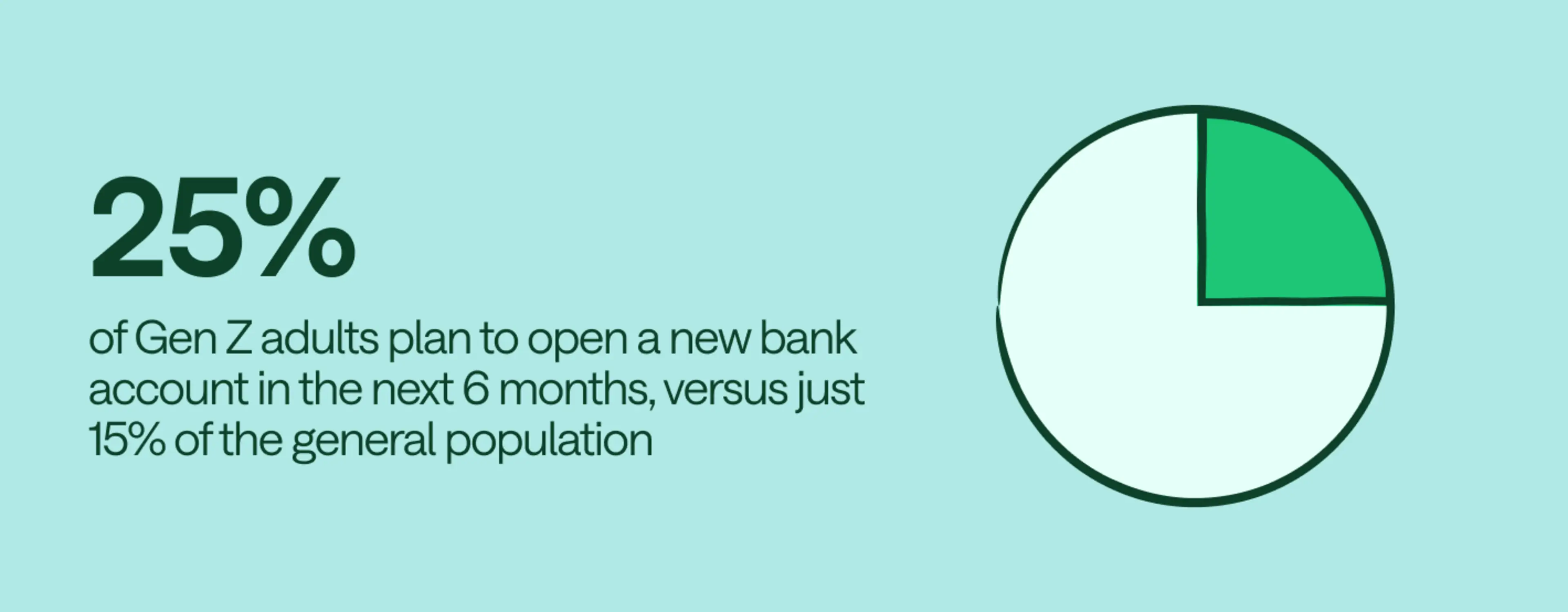

Now that Gen Z is ready to handle things on their own, many are making moves. 44% of Gen Z changed their banking relationship over the past 12 months.2 Here's how Gen Z is charting their own path for money management long-term.

Why Gen Z is ready to switch banks

Banks beware: Gen Z isn't content to sit back with what they've had for years. So just why are so many ready to switch things up?

Financial independence: Gen Z includes anyone born between 1997 and 2012. This puts them between 12 and 27 years old in 2024.3 Gen Z is ready for that long-awaited financial independence by creating their own accounts. They no longer want to rely on what their parents set up for them, especially if they were on a joint bank account.

Ready for something new: Young people are more likely to experiment, innovate, and take risks on something different. This includes using new products and brands. 77% of Gen Z says they make an effort to try new brands, the most of any adult group.4 Gen Z is more interested in trying a new banking relationship compared to other generations, who are more likely to report loyalty to one single financial institution.5

More comfortable with tech-first banks: Gen Z is more likely to try newer, less traditional accounts outside national brick-and-mortar banks, like fintechs and neobanks.1 When you grow up on phones, you might be more comfortable choosing a tech-first option where you can access everything you need on an app. These online financial institutions can have lower fees, better interest rates, and digital planning tools thanks to the money they save by not having physical branches.

Ultimately, Gen Z is less brand-loyal and more likely to switch to the bank that offers the features, benefits, and values they want most.

What Gen Z wants in a bank

So what does it take to impress the next generation of savers? While Gen Z might be new to banking, they know what they want.

Digital (and instant) payments: Gen Z grew up with digital payment services. Many of them may have never written a check. Gen Z often expects digital payment systems to be included and work smoothly with their bank.

Financial planning support: Gen Z knows they need help from their financial institution. Around 39% are worried about making the wrong choices with their money.6 They appreciate options that provide financial planning support, like budgeting software or free access to view their credit scores.

Personalized recommendations: One-size-fits-all service is a thing of the past in the world of AI and big data. Gen Z hopes their bank's online system will proactively give them customized offers and advice based on their situation. No pre-approved loan offers in the mail if what you really want is faster access to your paycheck.

Social justice values: Gen Z is willing to walk away from a company that doesn't share their values. Banks that meet Gen Z's values for climate change, DEI, and other ethical business practices are a priority.7

24/7 customer service: Even though Gen Z is tech-savvy, they still appreciate the value of having someone to talk to. Access to 24/7 support is commonly listed as one of their top suggested improvements for digital banking.5

What problems are Gen Z experiencing with finances?

Everyone thinks they have it rough, but Gen Z definitely has reason to complain about money and the overall economy.

Bank fees: Gen Z bank account holders pay over $19 per month for ATM fees, overdraft fees, and routine account fees. Millennials are also struggling with fees, spending nearly $17 a month. In comparison, Gen X only pays around $4.50 a month, while Baby Boomers pay just $2.21 a month.8 Gen Z account holders could save by switching to banks that don't charge out-of-network ATM fees, monthly fees, or overdraft fees.

High cost of living: Gen Z is entering the workforce during an expensive period. There's a lot to deal with between high interest rates, rising prices from inflation, student loan payments, and the rising cost of renting and home ownership. No wonder over 50% of Gen Z worry about not having enough money.6

Less certain income: Gen Z is following a different career path than past generations. Gen Z workers are more likely to be gig workers and freelancers, even if they have another job. Many are interested in starting their own business. They have less income certainty than those receiving everything from a steady paycheck. This could make it harder to qualify for mortgages and credit cards, unless they have accounts at places tailored for freelancers.

Why Gen Z should focus on building credit and savings

Given everything Gen Z has on their plates, building credit and savings is understandably not a top priority. Still, while it's easier said than done, here's why getting started now is so important.

Living for today, not tomorrow

Roughly three-quarters of Gen Z adults say the economy makes them hesitant to set long-term financial goals. Meanwhile, two in three Gen Z adults wonder if they'll ever have enough money to retire.9

At the same time, most Gen Z said they would prefer spending more on experiences to have a better quality of life today rather than having extra money in their bank account.9

While Gen Z might be less focused on the long-term future, many say they wish they had put more aside for an emergency fund.10 This would give them a cushion against short-term issues like a car breakdown, a medical bill, or a lost job.

Building for the future

Gen Z is concerned about reaching their long-term goals. But they have some good news: time is on their side. The sooner someone starts saving money, the more it will grow thanks to the power of compound interest. No one can predict the future, but members of Gen Z who focus on building savings and credit will likely be pleased with the results later in life.

The types of accounts Gen Z is opening

There are bank accounts and there are bank accounts. What types do Gen Z want?

Spending accounts

When it comes to opening bank accounts, Gen Z is still sticking to the basics. They prioritize entry-level checking and savings accounts and credit cards.1

More sophisticated deposit accounts like a certificate of deposit (CD) and money market accounts are not as popular with Gen Z. A money market account could require an opening deposit of thousands of dollars. CDs pay higher interest rates but can lock up the money for months to years at a time.

Digital investments

Gen Z is also less interested in developing relationships with investment advisors and insurance agents.1 But as their financial needs evolve and become more sophisticated, they could become more interested in these relationships.

On the other hand, Gen Z adults show more interest in investing in digital assets and cryptocurrencies than other generations. Around 20% of Gen Z owns digital assets, while only 18% own stocks.11

New money for a new generation

Gen Z customers are digital-savvy and facing unique challenges. They expect their financial institutions to understand where they're coming from and find ways to help. And if their current account isn't up to the job, Gen Z is ready to move on.

Are you exploring the market and ready to try something new? Consider opening an account with Chime. As the fintech that was one of the pioneers of the elimination of overdraft fees, we provide digital-first users plenty of helpful features and products, including digital payments with Pay Anyone, a network of over 50,000 fee-free ATMs,12 getting paid up to two days early with direct deposit,13 and 24/7 customer service. There's a reason why we're the #1 Most Loved Banking App.™

For a deeper dive into how Gen Z is making money moves, check out how Gen Z is thinking about building wealth.