A certificate of deposit (CD) is a steady and low-risk option for saving and investing. CDs are a type of investment savings account that earns a fixed interest over a set period of time. Typically, CDs earn higher interest because you can't touch the funds until the term ends.

Though certificates of deposit don't provide the same returns as higher-risk investments like stocks, they can help you earn significant interest with less risk. In this article, we'll explain why opening a CD is a smart money move, which types are available, alternatives to CDs, and tips for choosing the right CD.

How do CDs work?

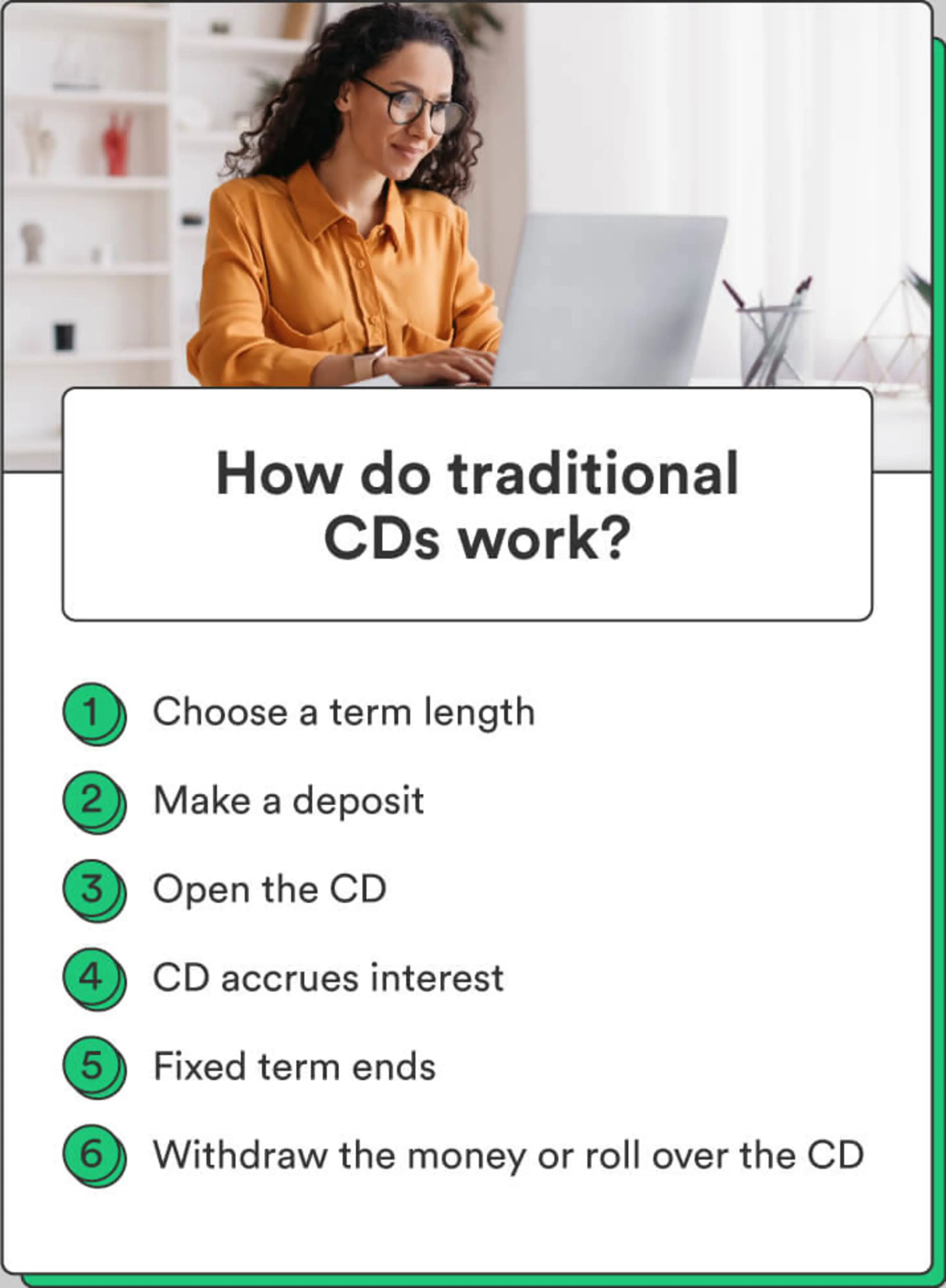

To open and earn interest on a CD, you need to deposit money equal to or greater than the minimum deposit and leave it untouched for a set period (usually three months to five years).

Once the CD reaches maturity, you can cash it in. You can also "roll it over," reinvesting your initial deposit and the interest it earned.

Financial institution sets the term length and rate

Before opening a new CD, you'll want to choose a term length. Most financial institutions offer several term lengths, ranging from a few months to years. However, CD rates can vary for several reasons, and interest rates often rise and fall.

The top factors influencing CD rates are:

Federal funds rate: Changes in the Federal Funds Rate set by the Federal Reserve can directly influence CD rates by making financial institutions adjust their offerings to remain competitive.1

Economy: During economic growth, interest rates tend to increase; economic downturns, on the other hand, bring lower rates.

Treasury yield changes: When U.S. Treasury yields go up, CD rates tend to go up too. This is because banks often set CD rates based on what they can earn from safe investments like Treasury bonds. So, when Treasury yields are higher, banks can offer you better CD rates. But when Treasury yields are low, CD rates are usually lower too.

Time to maturity: Generally, the longer a financial institution can use the money you deposit, the more interest you will earn. That's why you will likely earn more interest in five years than you would in three months.

The investor makes the deposit to open the CD

To officially buy the certificate of deposit, you'll need to deposit money into your account – this is the principal. In some cases, you can choose how much you want to put down.

Other times, the financial institution or broker will require a minimum deposit. Before deciding where you will invest, ask about the vendor's deposit policy.

The CD accrues interest until the fixed term ends

At this point, all you have to do is wait.

From the time you place the deposit, the CD will start to earn interest. During this time, the bank or credit union can use the money to grant loans to other account holders, make investments, keep the bank reserves full, or cover operating expenses.

Regardless, you can't touch the money during this time, or you'll have to pay steep penalties.

The investor withdraws the money or reinvests the CD

Finally, when the CD reaches maturity, or the fixed term ends, you can either withdraw the money or reinvest in a new CD.

CDs vs. savings accounts vs. money market accounts

As a reminder, a CD is a special type of savings account that can't be touched for a specific amount of time while it earns a predetermined amount of interest. If a CD isn't the right fit for your financial goals, you can also consider one of these savings solutions:

Traditional savings accounts: Even if you choose a high-yield savings account, chances are you may receive lower interest than you would with a CD or money market account. However, there are no penalties for withdrawing money and no minimum deposit, making it a strong choice for people with short-term goals or a limited emergency fund.

Money market accounts: This is another type of savings account that serves as a middle ground between traditional accounts and CDs. They have higher interest rates than traditional accounts, but the user can withdraw money before the term ends (with limitations).

CDs | Money market accounts | Savings accounts | |

|---|---|---|---|

Interest | Higher | Moderate | Lower |

Risk | Low | Medium | Low |

Liquidity | Low | Limited | High |

Deposit/minimum balance | Moderate to high | High | Low to none |

When should you open a CD?

Think about opening a CD if you need somewhere to store your savings for a specific amount of time. CDs can help grow your money until you need it and can be useful if you're:

Saving for a time-bound goal like purchasing a car or house

Looking for a low-risk investing opportunity

Someone who often dips into their savings

But, remember that CDs aren't ideal for building long-term wealth. If you want high returns, look into lucrative, high-risk investment opportunities like high-yield bonds, stocks, or mutual funds.

Pros of certificates of deposit

Fully understanding the pros and cons of certificates of deposit can help you make more informed decisions for the future, especially if you're a first-time investor.

So, let's look at some pros of certificates of deposit:

Low risk: Because CDs are FDIC-insured, you're guaranteed to receive your money when the term ends.

Higher interest rates: CDs generally earn higher interest than money market accounts and traditional savings accounts.

Prevents impulsive spending: CDs separate the money you need for a specific goal from your general savings, which helps you avoid spending it early.

Cons of certificates of deposit

While CDs are safe investments, they also have a few disadvantages. Some cons of CDs are:

Limited liquidity: If you withdraw money early, penalty fees will eat up a portion of your earnings.

Capped growth: While investments like stocks and bonds have the potential to earn limitless interest, CDs earn a set amount of interest over a specific period.

Minimum opening deposit: To open a CD, you have to pay the minimum deposit, generally between $500 and $2,000.2

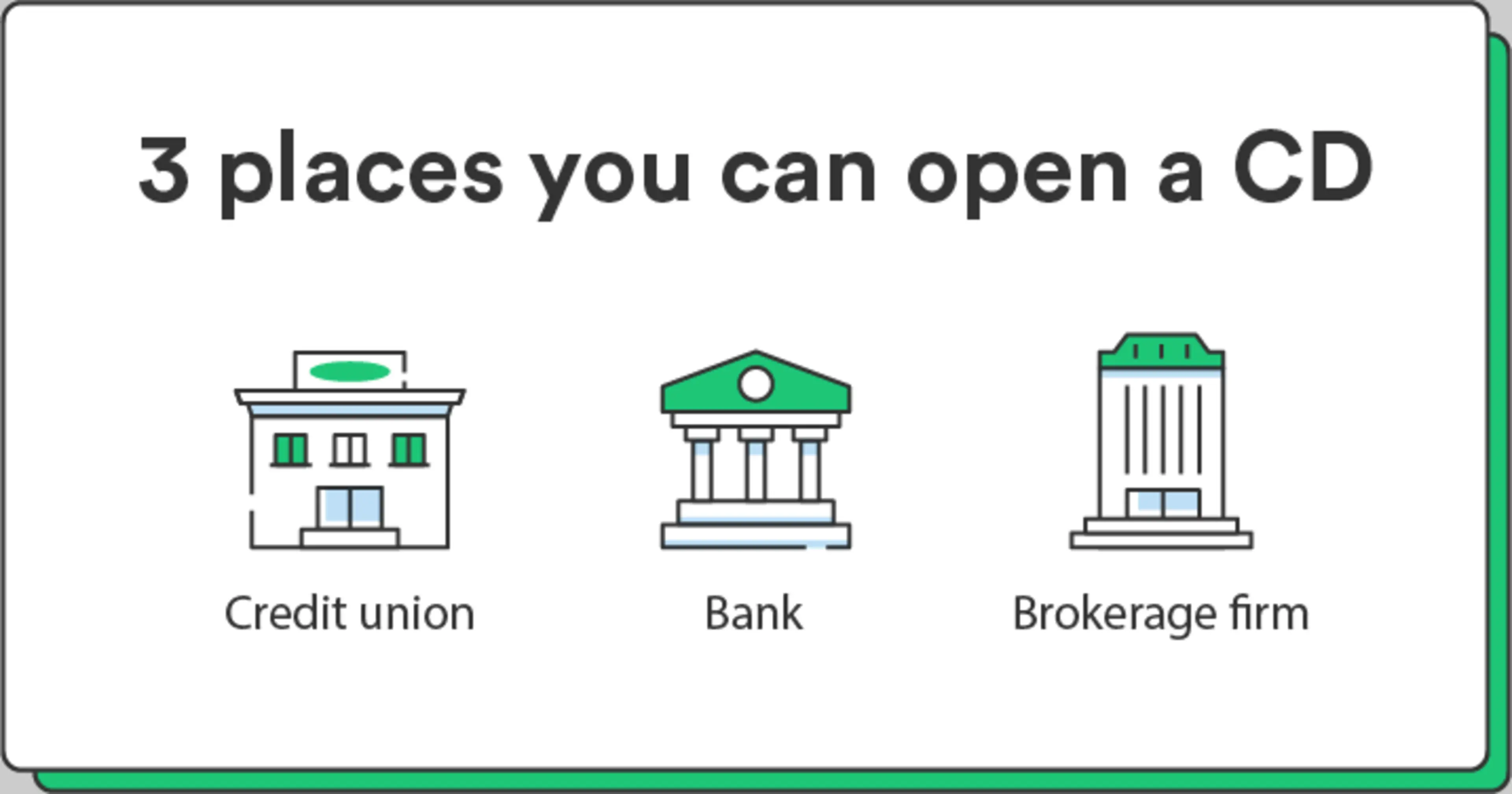

Where can you open a CD?

You can open a CD at most banks or credit unions. Financial institutions may all structure their CDs differently, so be sure to shop around to compare interest rates, terms, minimum deposits, and fees to find the right fit for you. We'll cover the different types of CDs you'll likely come across while you search below.

You can also buy certificates of deposit through brokerages and financial advisory firms. Brokers can help you secure CDs from different banks, acting as a middleman between you and the CD provider.

What types of CDs can you choose from?

Depending on your risk tolerance and desired liquidity, a traditional CD might not be right for you. Fortunately, there are several other types of CDs for you to choose from. Here's a quick rundown of the top options:

Type | Interest | Liquidity | Inflation resistance |

|---|---|---|---|

Traditional CD | Moderate because they often have lower deposit minimums | Low liquidity because an early withdrawal results in penalties | Low because you can't make early withdrawals |

No-penalty CD | Moderate due to the ability to withdraw early | Easiest to liquidate without penalties | High because you can withdraw the money and reinvest it with zero penalties |

Jumbo CD | High due to large deposit requirements | Least liquid due to large deposit requirements and withdrawal fees | Low because they're on a fixed term |

IRA CD | Lower, but they offer tax and retirement advantages | Low liquidity since early withdrawals can trigger tax penalties | Low because they don't gain interest within Individual Retirement Accounts |

Bump-up CD | High because the interest rate can increase once if market rates rise | Moderate liquidity since you can increase the interest rate or deposit | Low because you can increase the interest rate if the market changes |

Brokered CD | High because of access to more competitive options | Moderate liquidity since you can sell before they reach maturity | Moderate because you can sell CDs with a fixed term to turn a profit |

Below you'll find some additional info about the different types that are available to you in 2024.

Traditional CD: This is the most common type of CD – it comes with a fixed term and interest. It also has strict penalties for people who withdraw money early.

No-penalty CD: Also called liquid CDs, these are best for people who don't know when they'll need to access their money since there is no penalty for early withdrawal.

Jumbo CD: These often come with higher interest rates than regular CDs. However, you may need to pay a larger deposit or withdrawal penalties to secure the more favorable terms.

IRA CD: These CDs are meant to save for retirement spending and aren't taxed as long as you meet Individual Retirement Account (IRA) withdrawal guidelines.

Bump-up or step-up CD: This is a strong option if you expect CD interest rates to rise because it allows you to raise the interest rate once before the CD reaches maturity.

Brokered CD: You can buy brokered CDs from specialized brokers who have access to a wide variety of options from banks and credit unions.

How to choose a CD: What to consider

There is no "best" or one-size-fits-all CD. You just have to choose the option that complements your goals. Here are some factors you should consider:

What's the CD rate?

CD rates represent the interest your investment will earn before it reaches maturity.

You can't set your own CD interest rate, but you can choose the most favorable option for your financial goals. You'll need to choose which trade-offs you're willing to make, whether that's extending the term length for higher interest or accepting lower interest for a shorter term.

Here are some nuances to be aware of:

The longer the term you choose, the higher the interest rate.

Market interest rates can change once you place a deposit, increasing or decreasing the value of your CD.

Market rates for CDs are influenced by factors like economic conditions and the U.S. treasury.

CD interest rates may vary based on the issuer's internal policies and strategies.

How much do you need to open a CD?

The minimum amount of money you need to open a certificate of deposit will vary based on the financial institution you're working with and the type of CD they're selling.

Typically, banks offer CDs with minimum deposit requirements ranging from as low as $500 to more than $1,000. Others don't set a minimum deposit at all. Check with the specific bank or credit union you are interested in to find out their minimum deposit requirements for their CD offerings.

What happens when a CD matures?

Several things can happen when a CD matures. You can withdraw or "redeem" the funds, depending on your bank's policy. Remember to check the policy before attempting a withdrawal.

Some other things that can happen include:

Automatic renewal: If you don't take any action, some banks will automatically renew your CD for a similar term. For example, if you had a one-year CD, it may be renewed as another one-year CD.

Rolling over to a different term: You may have the option to choose a different CD term when your current CD matures. This allows you to take advantage of the latest interest rates and increase the value of your investment.

Interest payment: If you don't take action, some banks will automatically transfer the interest earned on the matured CD into a linked savings or checking account.

To make the most of your CD investment, it's wise to plan ahead and decide what to do with the funds when the CD matures.

Which CD term will work best for you?

The CD term you should choose depends on your financial goals, risk tolerance, and the current interest rates. Here are some of the most common CD terms financial institutions offer and the benefits of each:

Three months to one year is ideal if you're worried about inflation devaluing the CD or you need access to funds soon.

One to three years is ideal for higher interest rates without sacrificing short-term liquidity.

Three or more years is ideal if you want the highest interest rate and won't need to access the money in the CD soon.

Or, you can buy multiple CDs and stagger the maturity dates to access the earned interest at regular intervals.

Is there a chance you'll need to make an early withdrawal from your CD?

Early withdrawals from a certificate of deposit have consequences, so consider them carefully. Here's what you need to know about early withdrawals from your CD:

Penalties: Most CDs have penalties for early withdrawals. Issuers typically base these penalties on a percentage of the interest earned or a specified number of months' interest. The penalty amount varies depending on the terms of the CD.

Loss of interest: In addition to penalties, you may forfeit some of the interest you've earned if you withdraw funds before the CD's maturity date.

Tax implications: The IRS will tax the interest you earn on CDs as income. Early withdrawals could mean you're responsible for paying extra taxes the year you take out the money.

In some cases, you may be able to avoid or reduce penalties for early withdrawals. For instance, some banks offer "no-penalty CDs" or allow penalty-free withdrawals in circumstances like death or disability.

How will (or will) you grow your CD ladder?

A CD ladder is a savings strategy that involves continuously reinvesting the money from matured CDs into new CDs with staggered maturities.

Here's how you can create and grow a CD ladder:

Open multiple CDs with the financial institution of your choice.

Set different term lengths for each – again, common terms include three months, six months, one year, two years, and five years. From there, you can select whatever cadence you prefer.

Invest extra money back into your investments to keep your funds growing over time.