Key takeaways

Opening a joint bank account can simplify managing shared bills and saving for common goals if you are aligned with your partner

Both account holders share equal access and responsibility: that means you're both liable for withdrawals, overdrafts, or debts tied to the account

A joint account makes sense when you trust each other's money habits, have similar financial philosophies and goals, and communicate openly about money

Keeping separate individual accounts and a shared joint account can often offer the best of both worlds

Are you thinking about merging finances with your significant other, sharing a bank account with a child to help them learn finances, or even opening a joint bank account with a roommate to handle shared expenses? Opening a joint bank account offers a lot of convenience and flexibility but comes with some risks.

It's always wise to discuss how you'll manage finances with someone else before committing to a shared account. If you're on the same page and have the same goals for the account, a joint bank account can make a lot of sense. But if you can't seem to agree on spending habits and savings goals, opening a joint bank account online – no matter the ease and conveniences offered – may not be for you.

Pros and cons of opening a joint bank account online

Should married couples have joint accounts? The simple answer: It depends. In fact, there are several reasons to open a joint account with a spouse, significant other, child, or even a roommate, but there are plenty of pros and cons of joint bank accounts to consider before you do so.

Benefits of a joint bank account

Easier bill management and budgeting: If you and a partner or roommate co-manage finances and have shared bills (rent or mortgage, utilities, etc.), it's much easier to pay those bills together from a shared account. No more writing each other checks, sending money back and forth through a peer-to-peer payment app, or keeping a tracker of who owes whom what.

Meet minimum balance requirements: Pooling your money in a single account can help you meet minimum balance requirements to avoid fees and get better interest rates on savings accounts.

Simplified shared financial goals: If you and a spouse are saving for a down payment on a house, a joint bank account allows you to track your progress together. Similarly, opening a joint bank account with a child allows you to coach them as they save for their first car or another big purchase.

Clear separation of finances: Joint bank accounts help you keep your personal finances and shared finances separate. Many couples happily share a joint bank account but also have separate savings and checking accounts for their own personal expenses.

Ready to get a joint bank account with your significant other? Here's how to open a checking account in five simple steps.

Drawbacks of a joint online bank account

End of relationship: If you and your partner split up, it can be challenging to separate funds in a joint bank account in a way that feels fair.

Debt liability: One partner could be liable for debts the other partner acquired through the joint account.

Fighting: If you and a partner don't have clear rules around how you're spending and saving, you might find yourselves fighting about money more regularly.

Reckless spending: Your joint account member may recklessly spend money as they see fit – or even withdraw large chunks of cash – without your permission since you are both equally responsible for and entitled to the money in the account. Joint bank accounts require a lot of trust.

When is it right to keep separate accounts?

It's up to you and your partner to decide whether to keep your bank accounts separate or merge them. Some folks swear by having their own accounts, especially if they've had problems with joint finances in the past.

Here are some scenarios when it makes sense to keep separate accounts:

You have different philosophies on spending and saving.

You each have your own job and retirement plans.

You have significantly different levels of credit card debt or student loan debt.

You have been burned by a past partner and have trust issues surrounding money.

However, even if you have joint bank accounts, partners should be open and honest about finances. If you're building a life with someone, you've got to be able to talk about money. It impacts every part of our lives, from health and housing to education and leisure activities.

When does it make sense to open a joint account?

In many cases, however, it doesn't make sense for couples to keep their accounts separate. Here are some scenarios when opening a joint bank account could be the right call:

You are aligned on several goals, such as saving for a house, wedding, car, or vacation together.

You have children together – or are planning to have children.

One partner primarily works while the other takes care of the home and/or children.

You don't generally fight with your spouse and trust they will treat money as responsibly as you will.

Opening both a joint bank account online and a separate account

The good news? You don't have to choose between opening a joint bank account online or keeping finances entirely separate. Many couples, parents with children, roommates, or even friends saving for a trip together have the option to open a bank account together – and still retain their personal accounts.

If you and your partner trust each other's financial habits, keeping both types of accounts may be the best choice. You can still have separate accounts, perhaps for one partner to manage their student loan debt or because each partner wants their own "fun fund" with no questions asked.

However, if you frequently disagree on how to spend or manage your money, it may be best to keep that money separate entirely.

Not sure how to have joint and separate accounts? It's easy! Simply retain your existing bank accounts, and apply for a joint account together at your preferred financial institution. While it may be more convenient to have all three accounts – your account, your partner's account, and your joint account – at the same bank or credit union, you should be able to transfer money easily between different institutions with little hassle.

Making the final decision on opening a joint bank account online

When opening a joint bank account, whether a joint online checking account or a savings account, make sure it's a joint decision. A joint account means you will share money with your significant other (or any other joint account holder), so you both need to be ready to have open and constructive financial discussions.

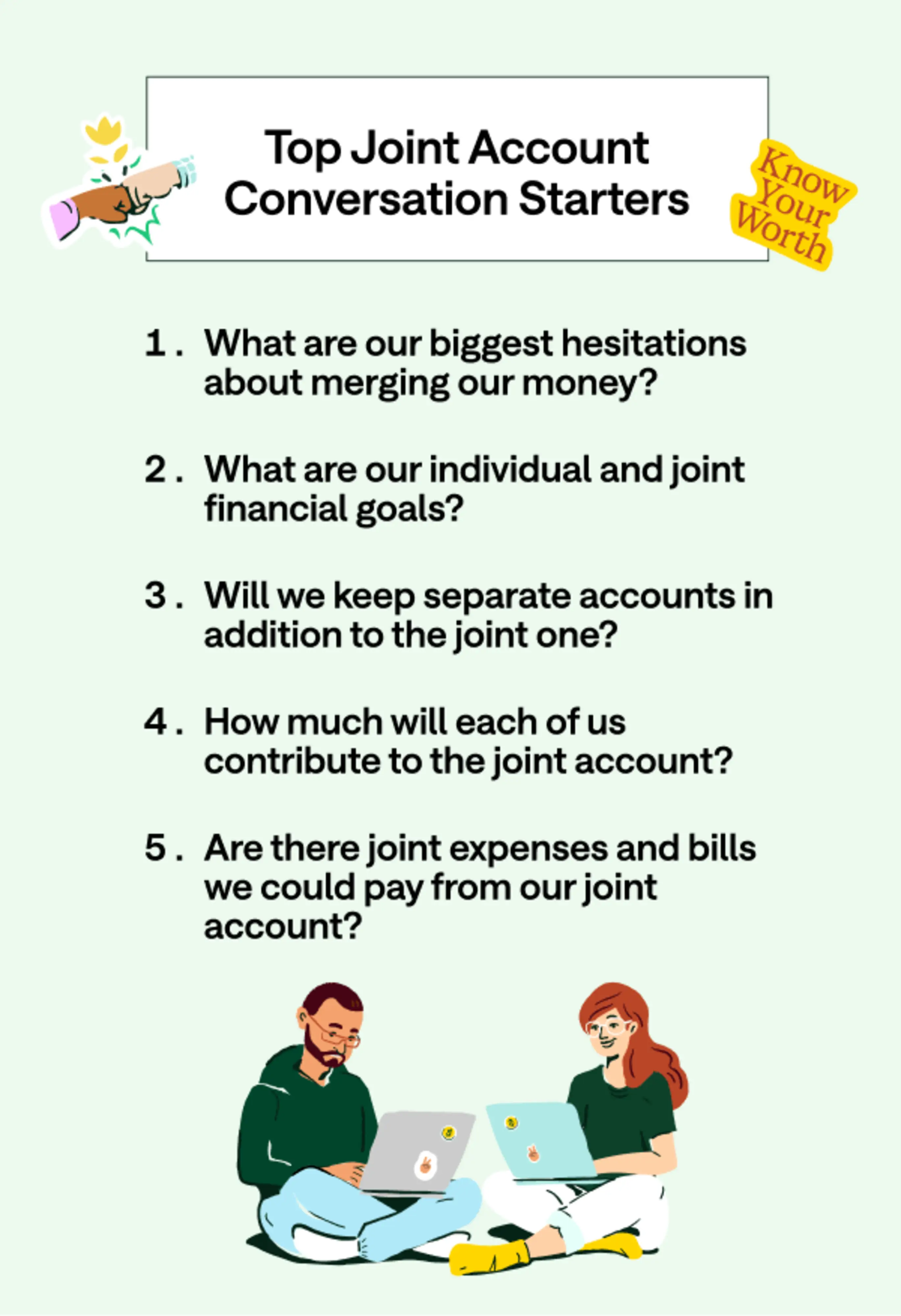

Start with a conversation with your significant other. Try to understand each other's viewpoints, and don't attempt to impose your views over theirs. If you don't know how to start the conversation, here are some financial questions you can use as a guide:

What are our financial goals?

Will we keep separate accounts, too?

How will we contribute to the joint account?

Can we pay joint expenses from the joint account?

Do we need money guidelines?

How will we communicate about finances?

How much will we save each month?

How much will we budget for leisure?

How will we handle unexpected expenses?

How will we manage changes in income or job loss?

How will we deal with debts and loans?

How will we resolve financial disagreements?

What are our concerns about merging finances?

There's no wrong answer when discussing whether a joint bank account makes sense for you and your partner. Remember to be honest during your discussion, as this is a big decision – and you need to be realistic about how you feel.

What worked for others might not work for you and your partner. The decision is yours to make as a couple, no one else's.

Decide on joint bank accounts together

Joint bank accounts are popular among couples, parents and children, and even roommates because of the convenience, but that doesn't mean they make sense for everyone. If you're not ready to go all in with a partner, keeping a separate bank account alongside a joint one – or skipping a joint account altogether – is a totally viable option.

When you're ready, find out what you need to open an online bank account, with or without a significant other.