Pay yourself first is an often-repeated personal finance rule that encourages saving before you pay bills or spend anything. You can build a positive money habit by moving cash to savings as soon as your paycheck hits your bank account.

The question is, how much of your paycheck should you save?

You might aim for a set dollar amount or a percentage of your take-home pay. Regardless, figuring out how to divide your paycheck to save money can be challenging when you have bills and other expenses that need your attention.

Let's look at a couple saving strategies to get you closer to your goals.

How much of a paycheck should go to savings?

A good rule of thumb is to save at least 20% of your take-home pay, but the "right" amount depends on your financial situation and goals.

If you're just getting started, even saving even 5% can build momentum. On the other hand, if you already have an emergency fund and minimal debt, you might aim higher, like 25–30% or more, to accelerate long-term goals like retirement or home ownership.

Think of your savings as divided into three buckets:

Short-term savings: emergency fund and upcoming expenses

Mid-term savings: major purchases or life events in the next few years

Long-term savings: retirement and investments

The ideal split between those buckets changes over time, but the goal is progress, not perfection. What matters most is developing a habit of saving something from every paycheck, no matter the amount.

Now, let's look at three practical strategies you can use to decide how much to save and how to make it happen.

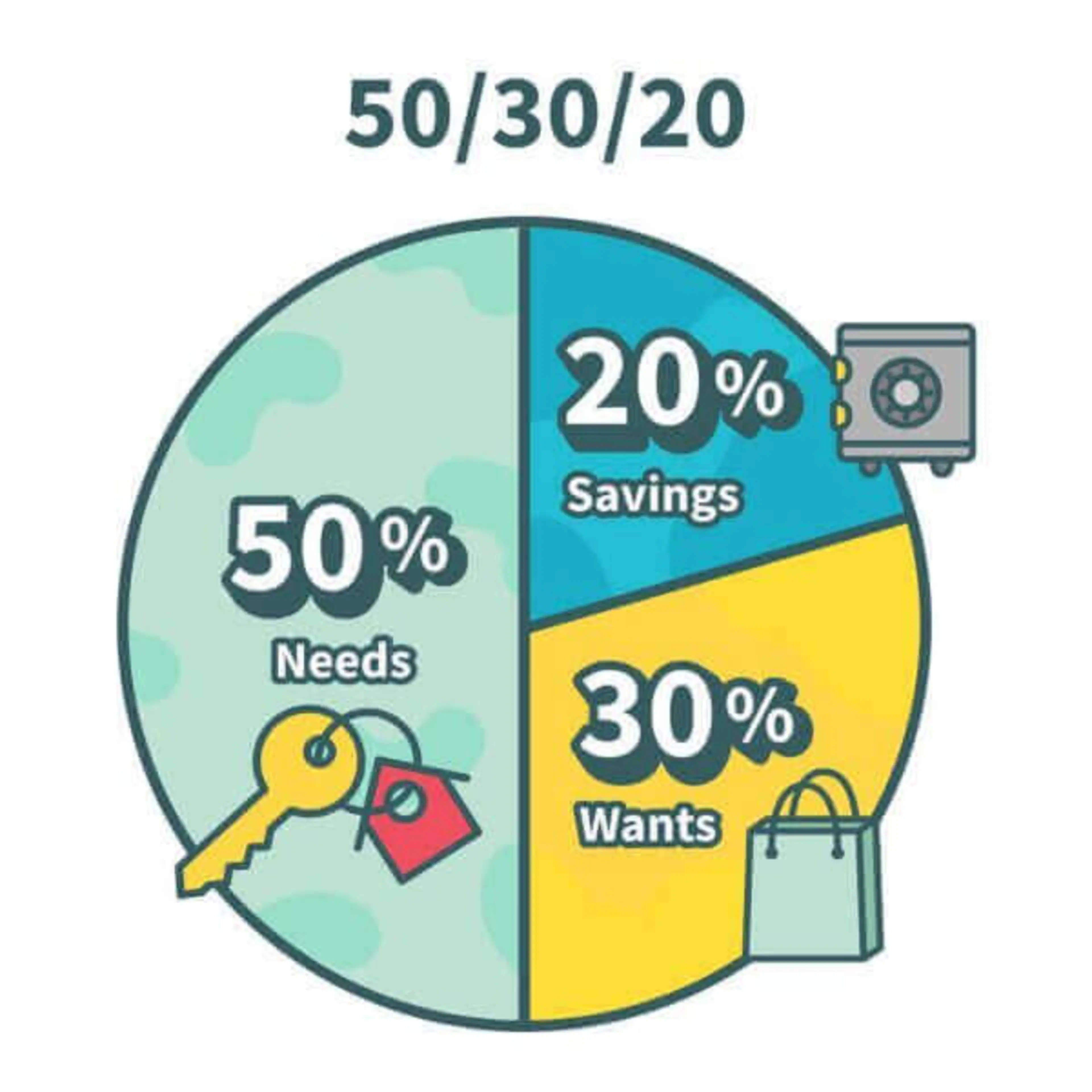

Strategy #1: The 50/30/20 Rule

How much of my paycheck should I save? Rather than aim for a dollar amount, use the 50/30/20 rule as a guideline. Here's how it works.

While everyone's paycheck and bills are different, the 50 30 20 rule is a simple way to divide your paychecks to include room for saving.

Here's how it works:

50% of your income goes to essential expenses

30% of your income is earmarked for spending

20% of your income is dedicated to saving (and debt repayment, if that applies to you)1

You can use the 50 30 20 rule to budget any amount of money.

For example, how much should you save a month if your take-home pay is $5,000? According to the 50/30/20 budget plan, you'd save $1,000 ($5,000 x 0.20).

It's that easy to set a savings target. You can also apply the same principle using other percentage-based budget systems, including:

80/20 method: 80% to expenses; 20% to savings and investments

70/20/10 method: 70% to needs; 20% to savings; 10% to wants

60/30/10 method: 60% to needs; 30% to wants; 10% to savings

Each of these budget systems can be used alongside the zero-based method, which requires you to assign every dollar of income a job with nothing left over. You can use a budget calculator to determine how much money should go into each bucket.

Strategy #2: Fixed-dollar, or "Pay Yourself First"

If you prefer simple math over percentages, pick a flat amount to save every payday and move it to savings the moment your check lands.

This works especially well if your income is steady.

How to do it

Choose a number you can commit to (e.g., $100 per paycheck).

Automate a transfer from checking to savings on payday.

Revisit the amount every 60–90 days and adjust up or down as life changes.

Why it works

It builds the savings habit without math every month.

You'll see steady progress toward near-term goals (e.g., a $1,000 starter emergency fund).

Quick example

If you're paid biweekly and saving $100 each check, you'll save $2,600 a year (26 pay periods × $100). Bump your savings amount to $125 per paycheck and you're at $3,250.

Pro tip: If your income varies, set a minimum flat amount (e.g., $50) plus a % of any paycheck over a baseline (say, 10% of anything above $1,500 take-home).

Strategy #3: Step-up savings

Grow your savings rate gradually by increasing it on a schedule, or every time your income rises, so you feel the change less.

How to do it

Start with a small % (even 5%) or a flat number.

Auto-increase by 1–2 percentage points each quarter, or direct half of each raise and windfalls (tax refunds, bonuses) to savings.

Why it works

You capture gains before lifestyle creep.

Small, scheduled bumps compound into big annual totals.

Quick example

Begin at 5% of a $4,000 take-home paycheck ($200/month). Add 1% every quarter. In a year you're at 9% ($360/month), saving $4,320/year without a single "budget overhaul."

Alternatively, when you finish paying off a loan or card, roll that payment to savings (turn your debt-snowball into a savings-snowball). You've already proven you can live without that money!

How to divide your savings

When you're talking about how much of your paycheck you should save, it's also important to think about where that money goes. If you have multiple financial goals you're saving for, then it makes sense to separate those funds into distinct pots.

Your savings account

A savings account is designed to hold money that you don't plan to spend right away. Savings accounts are a good place to store your sinking funds if you include them in your budget.

Sinking funds are savings funds for designated uses. So, for example, you might have sinking funds for:

Home maintenance or vehicle maintenance

Holidays and birthdays

Insurance premiums you pay biannually or annually

Pet care

New furniture

You can use sinking funds to plan for one-time expenses or recurring expenses that you only pay a few times a year. You can open a savings account for each of your sinking funds or choose one savings account that allows you to set up subaccounts for different goals.

Your retirement account

Retirement accounts help you save money for the future while enjoying some tax benefits. Those benefits may include tax-deductible contributions or tax-free withdrawals when you retire.

Here are some ways to maximize retirement plan savings, even on a small budget.

If you have a 401(k) or similar retirement plan at work, contribute enough to get the full company match if one is offered.

Get an annual raise? Increase your 401(k) contribution annually by the same amount each year.

Consider opening a traditional or Roth Individual Retirement Account (IRA) and setting up automatic contributions monthly. You can save up to $7,000 in an IRA for 2024 and 2025, or $8,000 if you're 50 or older.2

Your emergency fund

An emergency fund is money you save for emergencies only. Examples of emergency expenses include:

Unexpected vet bills

A car repair you didn't plan for

Temporary loss of income due to a layoff

Unplanned home repairs

Where to keep your emergency fund? Ideally, you keep this money in a savings account that's separate from your sinking funds but still linked to your checking account for easy transfers.

How much to save for emergencies? Three to six months' worth of expenses is a common rule of thumb but if you're just getting started, you might aim smaller.

For instance, you could set a goal to save a $500 emergency fund. Once you hit that, you can bump it up to $1,000 and continue raising the target until your emergency savings is fully funded.

Tips for saving money

Saving money is often about making small, consistent changes that add up over time. Here are a few practical tips for saving money to help you keep more of your hard-earned cash.

Automate your savings

Saving is a learned habit for most people and setting up automatic transfers can help to reinforce it. Use direct deposit to separate your paycheck into multiple bank accounts if that's an option to automatically grow your emergency fund. If your job doesn't offer direct deposit consider an automatic savings transfer from checking to savings each payday.

Track your spending

It's hard to save what you can't see. Review your spending habits regularly to identify areas where your money might be slipping away — such as unused subscriptions or frequent takeout. Try using a budgeting app or tracking tool to categorize your expenses and set spending limits that align with your goals.

Set specific goals

Having clear goals can make saving more motivating. Whether you're building an emergency fund, planning a vacation, or paying off debt, assign each goal a timeline and dollar amount. Visualizing your progress keeps you focused and helps prevent impulse spending.

Look for easy wins

Small changes can make a big difference. Pack lunch instead of eating out, brew coffee at home, or use cash-back apps for everyday purchases.

Even saving $20 a week adds up to over $1,000 a year.

If you're living paycheck to paycheck

Living paycheck to paycheck can leave little room for savings if money goes out as quickly as it comes in. These saving strategies can help you find a little extra in your budget to save.

Cut down on spending where possible. Reducing spending can instantly add money back to your budget that you could save. Review your expenses and consider what you can reduce or eliminate. For example, if you pay for any streaming services could you cancel one or all of them? Even if you free up just $10 a month, that's an extra $10 you have to build a savings cushion.

Manage your debt. Debt can drain your ability to save if you're juggling multiple payments to credit cards or loans. If you can't pay your debt off in full right now, ask yourself what you could do to make it less expensive. Refinancing student loans, for example, can help you get a lower interest rate. This can also lower your monthly payment and save you money in the long run, ultimately giving you more money in your budget to save. The same is true for transferring high-interest credit card debt to a balance transfer card with a 0% introductory promotional rate.

Improve your financial knowledge. Learning more about money can help you develop the skills and strategies you need to save consistently. For example, if you have a retirement plan at work do you contribute enough to get the full match from your employer if they offer one? If you want to open a savings account, do you know how to compare rates and fees to find the right one? Those are just some of the ways financial know-how can benefit you.

Slow and steady wins the savings race

How much of your paycheck should you save? The simple answer is as much as you can comfortably set aside, while still having money to pay bills, cover expenses, and repay debt.

If you struggle with budgeting, using an app can simplify expense and income tracking. Learn which budgeting apps rate the best for managing your money.