Credit cards are a helpful way to build credit, but you can spend too much if you don't practice sound financial habits. While appealing, purchases like trips to the movies, the latest phone, and skin care products can add up. When the time comes, you'll have to pay off your credit card charges.

You can handle your debt before it gets more complicated. Below are some helpful strategies for tackling credit card debt.

How to pay off credit card debt

You can use credit cards to pay for everyday and emergency expenses while possibly earning points and cash back benefits. However, they can have high interest rates, leading to debt if you don't pay your balance in full every month. Thankfully there are multiple ways to pay off credit card debt for a better future.

Below are four ways to pay off credit card debt: the avalanche method, the snowball method, debt consolidations, and balance transfer.

Method | Description |

|---|---|

The avalanche method | Prioritize paying higher interest debts first: You'll still need to pay the minimum amount on all cards, but the largest payment will go toward the card with the highest APR (annual percentage rate). |

The snowball method | Focuses on tackling lower balances first: Any extra funds you have after paying the low balances will go toward the higher amounts. You'll still need to pay the minimum amount on all accounts to avoid fees. |

Consolidate credit card debts | Instead of several monthly payments, you'll only have one. A debt consolidation loan will ideally have a lower interest rate than your credit cards to help reduce your accumulated overall interest. |

Credit card balance transfers | Move the debt from your existing accounts to one, low-interest card to create a single monthly payment. Cards designed for this purpose often have a 0% introductory interest rate so that you can reduce your debt faster. |

How to use the avalanche method

The avalanche method prioritizes paying higher-interest debts first. You will still need to pay the minimum amount on all credit cards, but you'll make a larger payment on the card with the highest APR (annual percentage rate).

After you've paid off the high-interest debt, put your money toward the account with the second highest interest rate. You'll pay less interest overall, leaving more money in your pocket.

Example: If you have three credit cards with 35%, 22%, and 18% interest rates, you'll want to make additional payments on the 35% card. Once you've paid this debt, you can start paying more towards the 22% credit card, then the 18% one.

How to use the snowball method

The snowball method focuses on tackling lower balances first. After paying the lower balances, any extra funds will go toward the higher amounts. You'll still need to pay the minimum amounts on all accounts to avoid fees.

Example: If you have three credit cards with balances of $6,000, $2,000, and $1,200, you'll pay down the $1,200 balance first. Next, you'll focus on the balance of $2,000, saving the $6,000 balance for last.

How to consolidate your debt

You can pay off your debts faster and potentially with a lower interest rate with debt consolidation. Instead of making several monthly payments, you'll only have one.

The debt consolidation loan will ideally have a lower interest rate than your credit cards to help you accumulate less interest.

Keep in mind:

You'll have to apply and qualify for this type of credit card payoff method.

Most lenders require a mid-600 credit score for debt consolidation loans.

You may still qualify if your credit score is lower, but the interest rate may be higher.

How to transfer a credit card balance

Balance transfers to a credit card allow you to move the debt from your existing accounts to create a single monthly payment. Most of these cards have a 0% introductory interest rate so that you can reduce your debt faster.

Keep in mind:

The offer requires you to transfer your balance within a certain time frame.

After the introductory period, the interest rate will increase.

You'll want to pay off your balance as soon as possible.

Some credit cards have a smaller limit than your debt amount. If that's the case, you could open an additional credit card. As a result of maxing out your credit card limit, your credit score could be negatively affected.

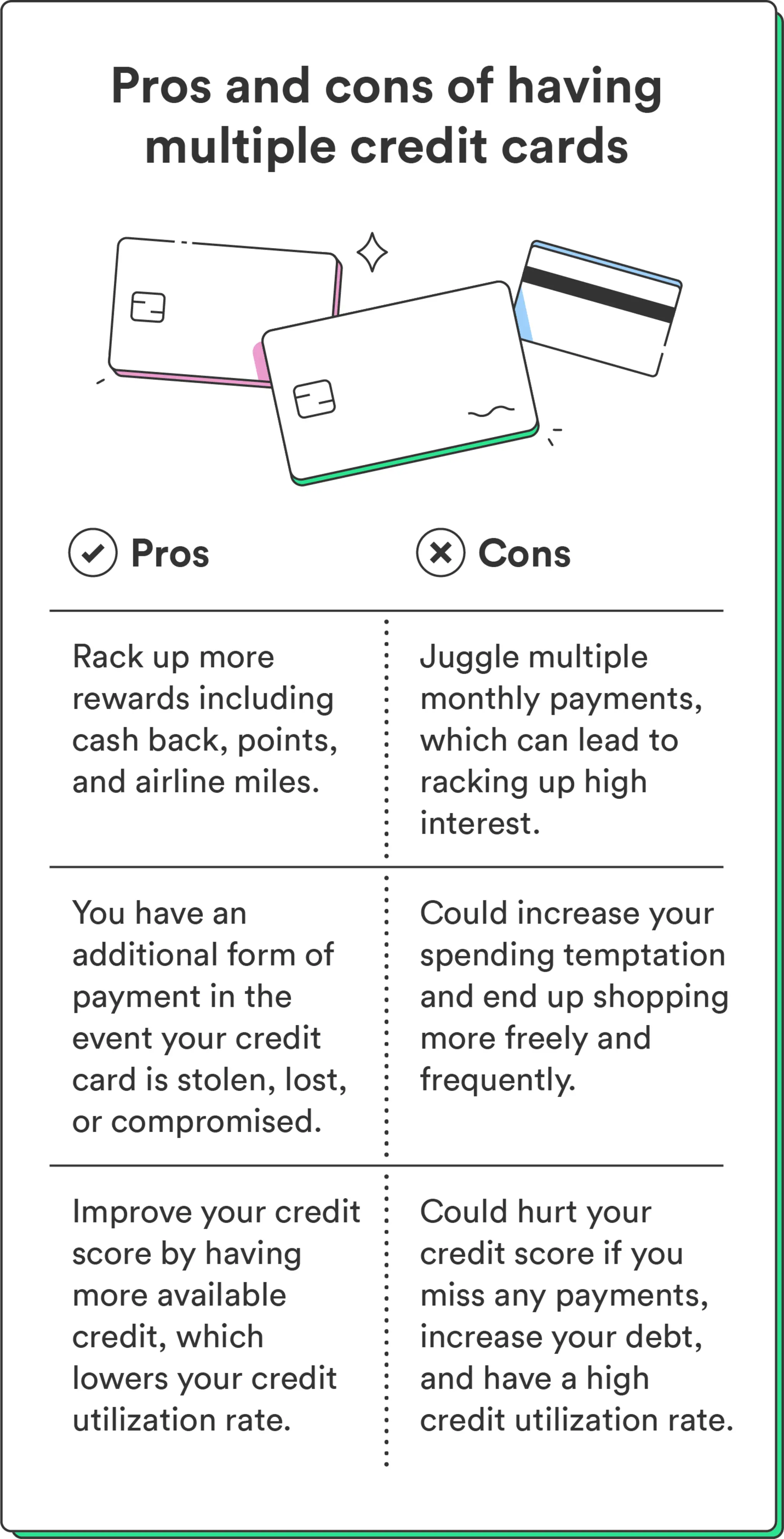

Should you have more than one credit card?

You can have more than one credit card if you pay them off each month – there's no harm in taking advantage of the different reward programs while working on your credit score.

However, if you can't afford multiple credit card payments, you may want to limit the number of credit cards you own.

Benefits of multiple credit cards

If you're using your card responsibly, you can reap benefits like:

Reward programs: Some types of credit card rewards include cash back, points, and airline miles for every dollar you spend. You can maximize your rewards on every purchase if you have multiple credit cards.

Backup card: If your credit card is stolen, lost, or compromised, you'll have an additional form of payment.

Improve credit score: More available credit can result in a lower credit utilization rate and positively affect your score.

Potential drawbacks of multiple credit cards

If you're struggling with paying off your credit card, you'll want to avoid opening another account.

Additional payments to keep track of: It can be challenging to juggle multiple monthly payments – you don't want to miss payments and rack up high interest.

Increase your spending temptations: If you have multiple lines of credit, your mindset may shift to spending more freely and frequently.

How does credit card debt impact your credit score?

Credit cards are a great way to build your credit, which can help you get approved for loans in the future. Your credit score is the three-digit number determined by your overall credit history. FICO® credit scores include the following factors:

Payment history: 35%

Credit utilization: 30%

Credit age: 15%

Credit mix: 10%

Credit inquiries: 10%

Your overall credit score also can affect the interest rates you pay. Credit cards work by demonstrating your spending history and proving you can pay off your balances on time. Credit lenders review your track record and are more likely to let you borrow money based on your history.

It's best to keep your balances and credit utilization lower to stay on a positive trend. Regularly missing payments or accumulating high interest can affect your credit score. The closer you are to maxing out your credit limit can also negatively impact your credit score.

Manage credit with confidence

Using our credit card payoff calculator, you can find out how long it could take to pay off your credit card debt and how much your monthly payments should be to erase your balance. Regardless of your financial situation, make a plan to pay off your credit card debt today.