Explore Videos

Check out the latest money moves, member stories, and finance guides.

Top Credit Card Tips That Can Boost Your Score #Chime #FinanceTips #Shorts

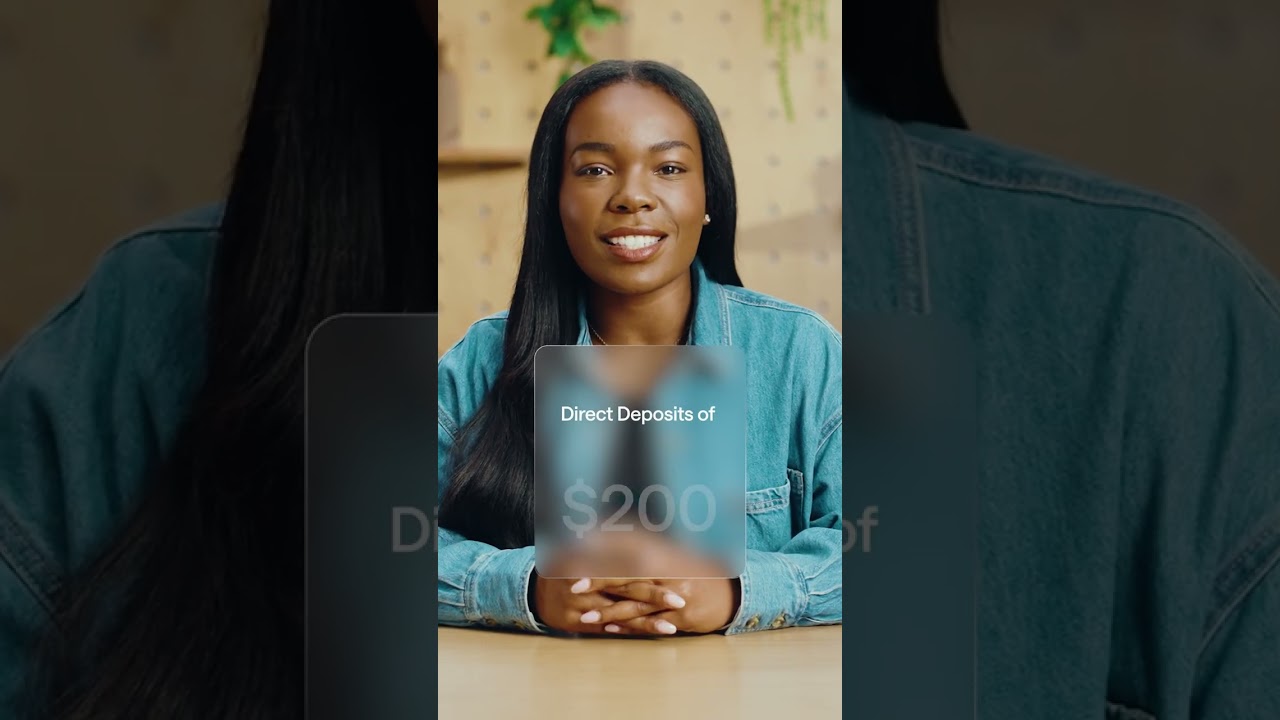

Get up to $500 before payday with #Chime #shorts

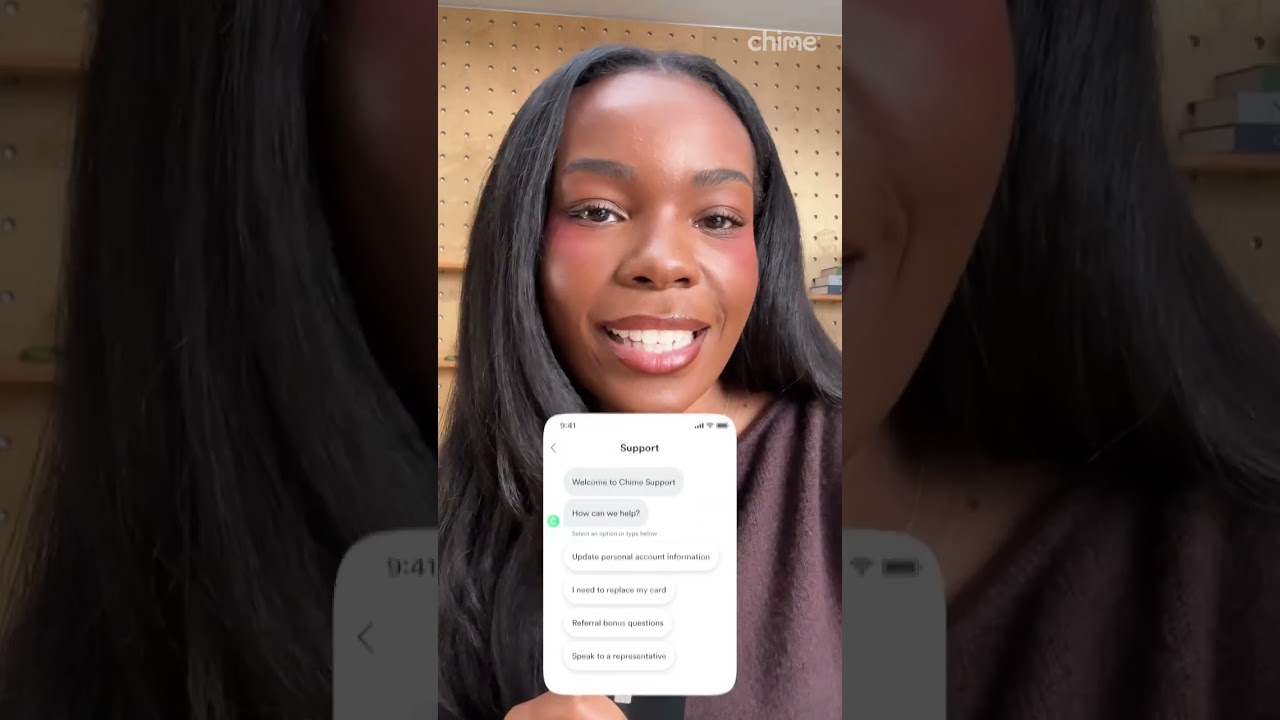

Quick #Chime tip: Need to reach us? This is how to contact customer service 💬