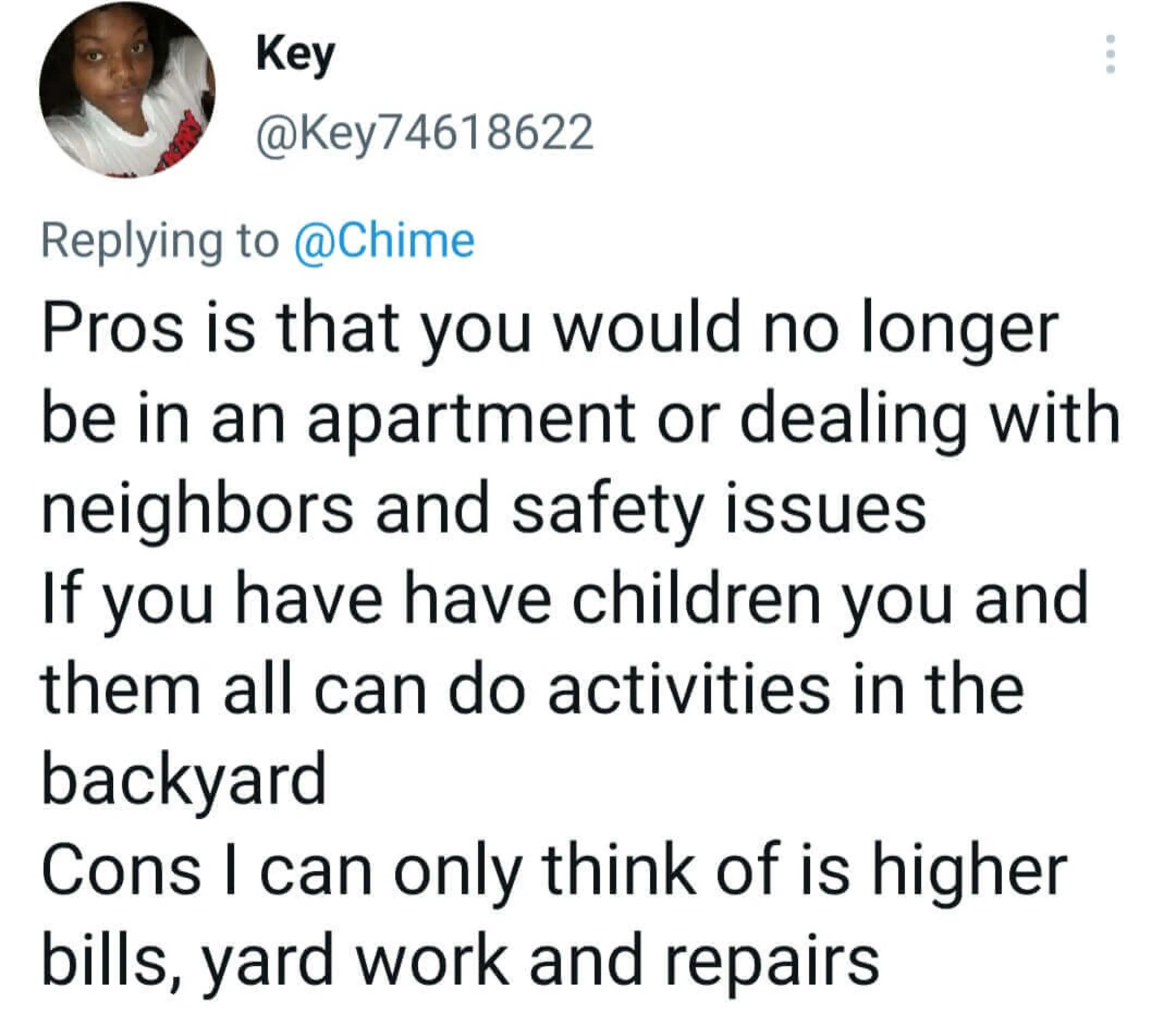

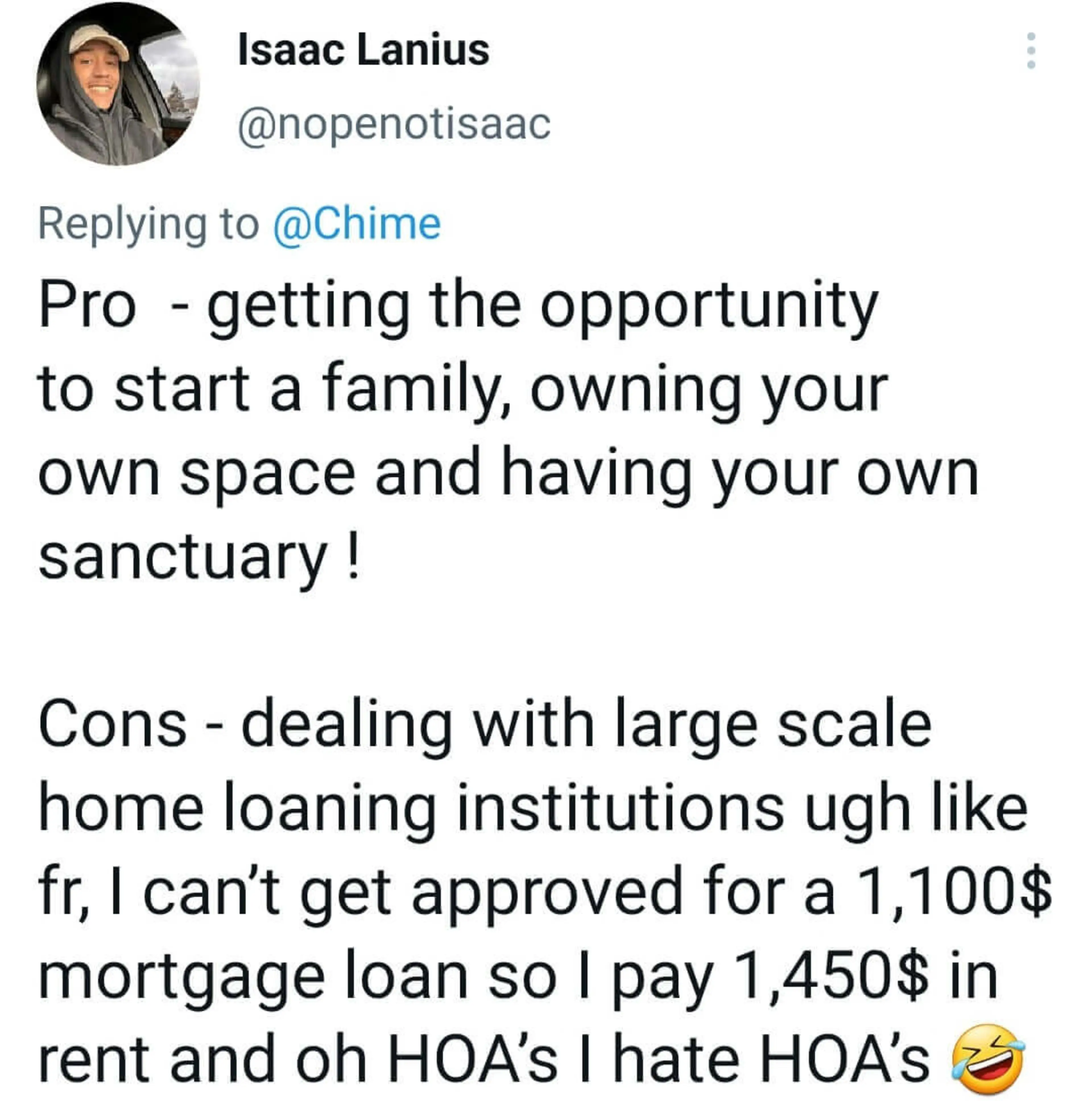

The decision to buy or rent a home is a bit of a conundrum. Which one is better? Let's explore the pros and cons of both options to help you come to a conclusion.

For many people, homeownership is synonymous with the American dream. After all, what could be more idyllic than a picket white fence and a two-story home with a spacious backyard?

But between today's record-high mortgage rates and elevated home prices, you're probably wondering if it's better to drop $50k on a down payment or to continue renting your apartment. There's no one-size-fits-all answer to this question – it depends on your unique circumstances.

Let's explore the pros and cons of both options so you can make the most informed decision.

Benefits of owning a home

Are you thinking about making the jump from renting to owning? Here are some reasons why it could be a great idea.

Building equity

In simple terms, equity is the difference between how much your home is worth and how much mortgage you owe. Every time you pay your mortgage, you're building equity in your home.

Your equity can also increase if your property appreciates, giving you a nice nest egg to tap into when you retire. And if you ever need cash to renovate your home or buy a second property, you can borrow against your equity by taking out home equity loans or HELOCs.

Federal tax benefits

Apart from having a roof over your head, being a homeowner also comes with some terrific tax benefits. For example, you can deduct your home mortgage interest on the first $750,000 of your mortgage debt.

If you've lived in the home for at least two years out of the five years before selling it, the home sale exclusion law allows you to exclude the first $250,000 of profit from your income.

Improving your credit score

Your payment history accounts for 35% of your credit score. Your FICO score might increase when you make your mortgage payments on time each month. And as your positive payment history becomes more extensive, potential lenders will see that you're a responsible borrower and be more willing to offer you favorable terms in the future.

If you're ready to finance your home purchase, learn about the different types of mortgage loans to decide what option would make the most sense for your situation.

Control over living space

Being the owner of your home means you have control over it. Want to paint your living room pink? Go for it! Want to knock out a wall to create a more open floor plan? Have at it!

Of course, there may be some exterior decoration limitations depending on your HOA (homeowner's association). But for the most part, you have freedom when personalizing your home's interior space.

Stability

Another major perk of buying a home is the stability it provides. If you opt for a fixed-rate mortgage, you'll know exactly how much your housing payments are for the next 15 or 30 years.

You also won't have to worry about your landlord increasing the rent or selling the property. And when you have a permanent place to call home, it's easier to feel like you belong to a community.

Cons of owning a home

Owning your own property is not always rainbows and butterflies — it also comes with some downsides. Before purchasing your dream home, here are a few things to keep in mind.

Paying for upkeep and repairs

From leaky roofs and broken appliances to clogged toilets and jammed garbage disposals, unexpected repairs can quickly eat up your savings if you own a home.

According to Angi, the average homeowner spends about $3,018 a year on repairs and upkeep. That's not counting major renovations or additions, which can easily cost thousands of dollars. So, if you're not handy or don't have a lot of money saved up, owning a home can be a financial burden.

High upfront costs

There's more to consider when buying a house than just the sale price. In addition to a down payment (anywhere from 3-20% of the loan amount), you'll also have to pay closing costs (typically 2-5% of the loan amount) and moving costs. And if you're buying an older property, you might have to shell out a few thousand dollars to furnish it and fix it up.

So how can you prepare for all of these expenses? Start by budgeting! Calculate how much you need to save to buy a house by factoring in the down payment amount, closing costs, and other related expenses.

Property taxes

Another not-so-fun part of owning a house is paying property taxes. Depending on where you live, these taxes can be pretty hefty. For example, in New Jersey, the property tax is 2.49%, which translates to $5,419 annually on a $217,500 home. So, while owning a house may be the American dream, be sure to factor in the cost of property taxes before you take the plunge.

Less mobility

If you own a home, you're less likely to pick up and move to a new city or town on a whim. And if you do decide to move, you'll have to put your home on the market. Selling a house takes time, effort, and money — and there's no guarantee you'll find a buyer willing to pay your asking price.

So, if you value mobility and flexibility, you might want to think twice before signing the dotted line on that mortgage agreement.

Takes time to build equity

When you begin paying your mortgage, your payments will mostly go toward interest rather than the loan's principal. This can make it feel like you're stuck in quicksand, never making progress.

Building equity in your home requires plenty of patience. But as you continue to make payments, more and more of your money will go toward the principal.

Advantages and disadvantages of renting

Like buying a home, there are also pros and cons to renting.

Pros

No need to worry about property taxes

The freedom to move if your job or lifestyle changes

Ability to try out a new city or neighborhood before making a long-term commitment

Your landlord is responsible for maintenance and repair costs

Rent payments are typically lower than mortgage payments

Fewer unexpected expenses

Cons

The landlord can sell the property or raise the rent

You can't make changes or renovations without the landlord's consent

You aren't building equity by paying rent

Some landlords don't allow pets

Less stability compared to owning a home

You can lose your security deposit if you damage the property

For the most part, renting is a flexible and relatively affordable option for housing. Though you're at the mercy of your landlord when it comes to rent prices and policy changes, you have the freedom to move around as you please and don't have to budget for maintenance expenses.

If you've decided that renting is the right option for you, be sure to take your time and shop around for the best rental before signing your lease agreement.

Renting vs. buying a house

There are pros and cons to both renting and buying, and it ultimately comes down to what makes the most sense for your situation. Buying a house allows you to build equity, improve your credit score, take advantage of tax benefits, and create a sense of stability and security.

On the other hand, renting allows you to move when you want, without the hassle (and expense) of selling a house. Plus, you won't have to come up with a large down payment or worry about closing costs and property taxes.

To rent or buy: how to make your decision

Still on the fence about whether to buy or rent? Here are a few key things to consider.

The responsibility of maintaining a property

Are you financially and mentally ready to be responsible for maintaining your property? If the answer is no, it might be best to stick with renting. But if you're up for the challenge of mowing the lawn and fixing leaky faucets, then homeownership could be the right move.

Your financial situation

Can you comfortably make monthly mortgage payments without putting yourself at risk of foreclosure? If not, you might want to hold off on buying a home until you're in a better position financially.

Your lifestyle

Do you see yourself living in one place for years or prefer the freedom to pick up and move at a moment's notice? If you think you might want to live in a different city or state in the next few years, renting may be the better option since it's easier to break a lease than sell a house.