Updated: November 2025 — The IRS has not yet published its 2025 filing updates. This page will be refreshed as soon as new guidance is released.

If you've ever checked out your pay stub, you may have noticed the taxes deducted from your wages. One of those deductions, FICA, is more than just letters and numbers. Short for Federal Insurance Contributions Act, FICA is a U.S. federal payroll tax that funds Social Security and Medicare – two programs that matter for your financial security.

In this article, we'll break down FICA in simple terms to help you understand how it affects your earnings.

What is FICA?

At its core, FICA, or the Federal Insurance Contributions Act is a system that helps you secure your financial future.

It's a combination of two deductions from your paycheck: Social Security and Medicare taxes. With FICA, the law requires employers to withhold a percentage of employees' earnings to fund Social Security and Medicare.

What are the two FICA taxes on a paycheck?

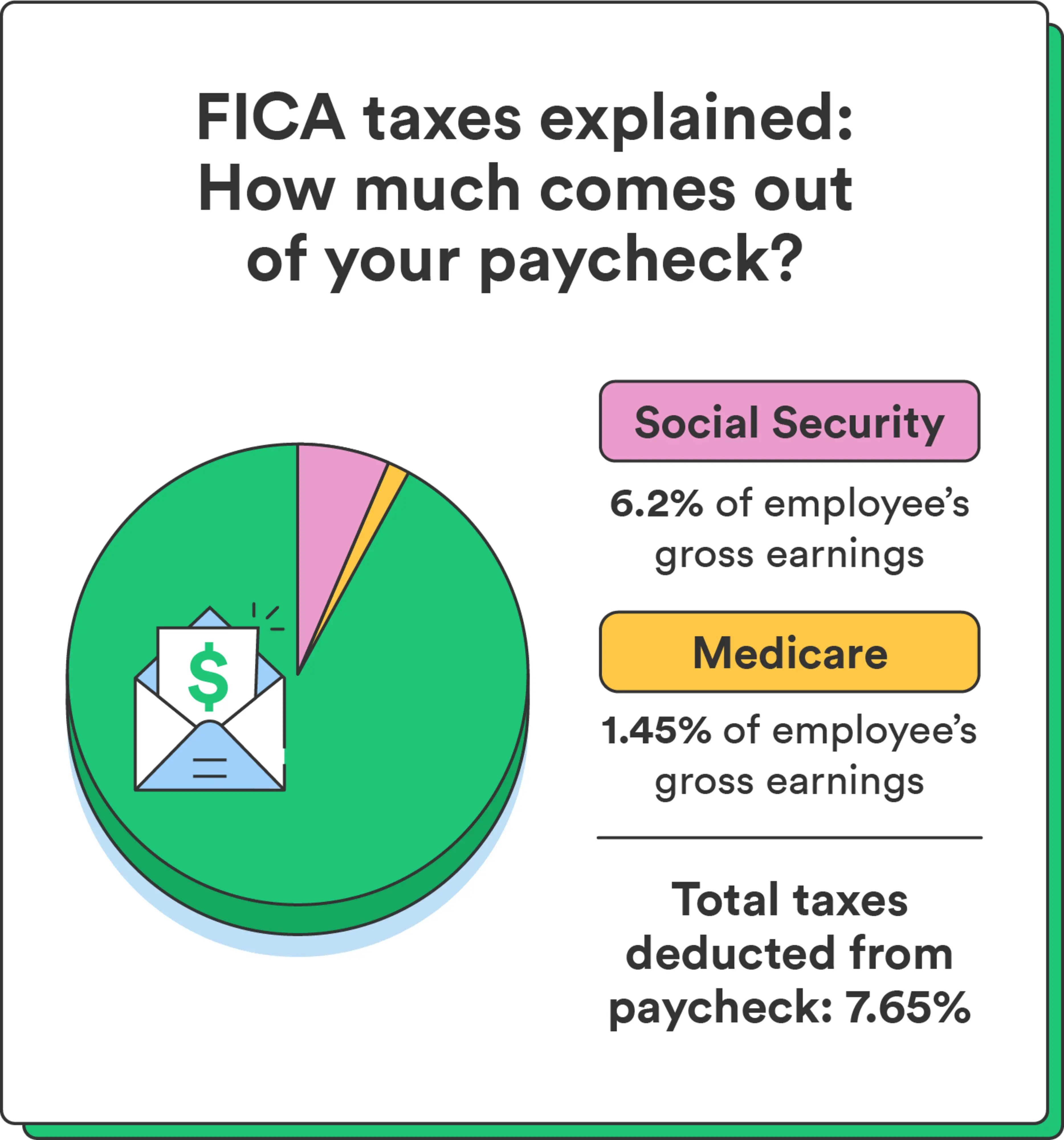

Note that FICA is not one deduction – it's a combination of Social Security and Medicare taxes.

Social Security tax

This tax contributes to the Social Security program, which acts as a safety net for your retirement. It's like setting aside a portion of your earnings to ensure financial stability later in life.

Both employers and employees have to withhold 6.2% of their gross earnings for this tax, up to a maximum wage base limit (the maximum amount of your earnings that's subject to be taxed). This year, this limit is $160,200 – meaning only earnings of $160,200 or less are subject to this tax.1

Medicare tax

The Medicare tax funds the Medicare program, which provides essential health care coverage for those aged 65 and older. It's your investment in future medical security.

Employers and employees are both required to withhold 1.45% of their earnings for Medicare taxes.1 While the Social Security tax has an income limit, there is no maximum wage base for Medicare tax, so all your earned income is subject to this tax.1

However, earners who reach a specific income threshold (based on filing status) should also be aware of the Additional Medicare tax.

This is an extra tax on top of the standard Medicare tax rate. This year, the Additional Medicare tax rate is 0.9% if you earn more than $200,000 as a single filer or $250,000 for joint filers.1

Employee pays: | Employer pays: | |

|---|---|---|

Social Security tax | 6.2% (for the first $160,200) | 6.2% (for the first $160,200) |

Medicare tax | 1.45% | 1.45% |

Total | 7.65% | 7.65% |

Additional Medicare tax | 0.9% (for earnings over $200,000 for single filers and $250,000 for joint filers) |

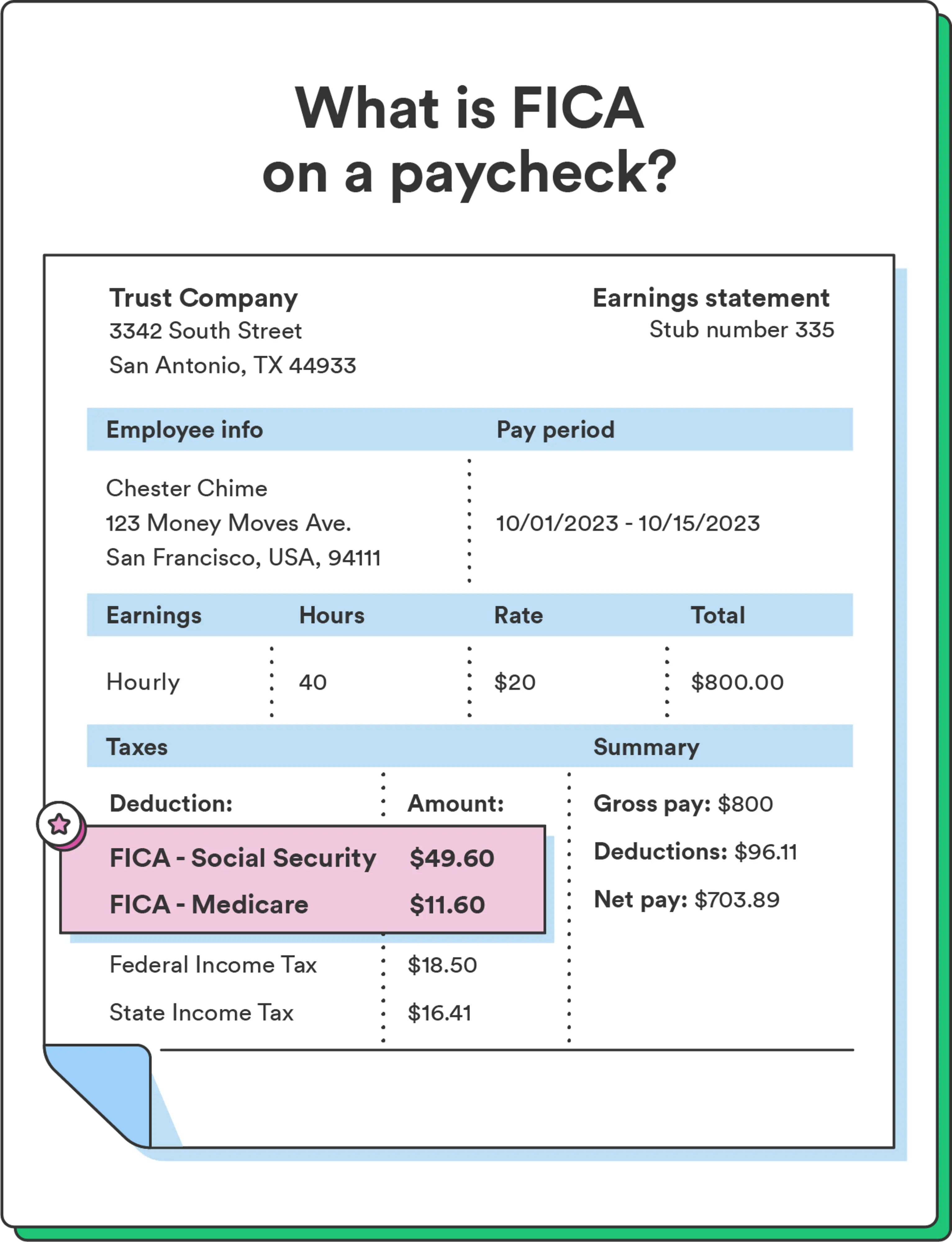

How to calculate FICA with examples

FICA deductions take out a total of 7.65% from your paycheck: 6.2% for Social Security and 1.45% for Medicare. These deductions impact your earnings, and understanding how they work is helpful for managing your finances effectively.

Let's break it down with a simple example: Suppose your gross earnings are $2,000 for a pay period. FICA taxes include the Social Security tax (6.2%) and the Medicare tax (1.45%). Here's how FICA affects your paycheck:

Social Security tax calculation:

You earn $2,000, and the Social Security tax rate is 6.2%.

To calculate your Social Security tax, multiply your earnings by the tax rate: $2,000 x 0.062 = $124.

Medicare tax calculation:

For Medicare tax, you take your earnings of $2,000 and apply the tax rate of 1.45%: $2,000 x 0.0145 = $29.

Your total FICA deductions for this pay period would be $124 (Social Security) + $29 (Medicare), totaling $153. Your employer will withhold this amount from your $2,000 gross earnings, leaving you with a net pay of $1,847.

Understanding this calculation can help you anticipate how FICA impacts your take-home pay and plan your budget accordingly.

SECA: FICA for the self-employed

SECA, or the Self-Employment Contributions Act, is like the solopreneur's version of FICA. When you're self-employed, you're responsible for paying the full FICA tax amount for both Social Security and Medicare.

The self-employment tax rate is 12.4% for Social Security and 2.9% for Medicare, totaling 15.3%.2 For the Social Security tax, only the first $160,200 of your total earnings are subject to be taxed in 2023, similar to FICA taxes.2

While you're responsible for the employee and employer parts of your taxes, there's a silver lining: You can deduct the employer's share as a business expense when you file taxes. This means you get a tax break that can help lower your overall tax bill, making it a bit easier to manage your finances.

Even if you're not self-employed, don't miss out on other tax deductions you may be eligible for.

Chime tip: To deduct the employer's share of the self-employment tax as a business expense, use Schedule C (Form 1040) on your annual tax return to report your business income and expenses. You'll find a line for "Other Expenses," where you can list the employer's share of the self-employment tax.

Stay informed about your paychecks

Understanding FICA taxes empowers you to make informed decisions about your income and budget. Remember that FICA funds crucial programs like Social Security and Medicare, which support your long-term financial security.

If you're self-employed, take advantage of deductions to lower your overall taxes. To own your financial journey, keep learning, stay informed, and consider seeking professional advice when needed.

Learn more about tax withholding and how it impacts your finances.