Key takeaways

Applying for a credit card involves checking your credit score, choosing a card that matches your credit profile and needs, reviewing terms and conditions, and submitting a formal application with required personal and financial information.

Preapproval can help you gauge your approval odds without affecting your credit score, while submitting a full application typically triggers a hard inquiry that may temporarily lower your score.

If denied, you can review the reasons, improve your credit, try a more accessible card such as a secured or student card, or wait several months before reapplying.

Responsible credit card use after approval — including paying on time, keeping balances low, and monitoring for fraud — is essential for building and maintaining a strong credit history.

If you're just getting started with your finances, knowing how to get a credit card, where to get a credit card, or even when you can get a credit card might be confusing.

Learning how to sign up for a credit card is crucial because, when properly used, credit card use can improve your credit score over time.

Wondering how to apply for a credit card for the first time? Cut out the stress and confusion with our guide to opening a credit card.

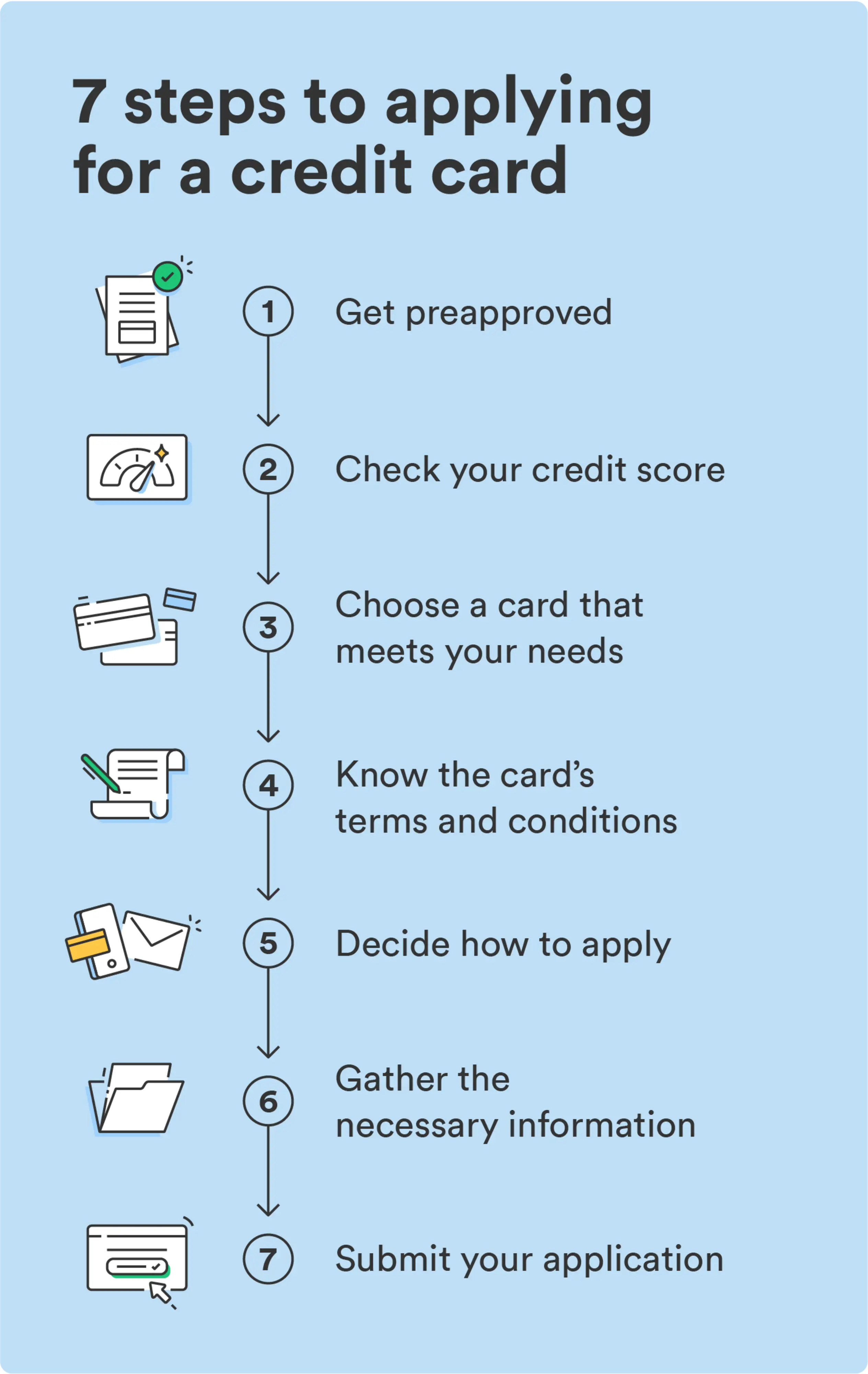

7 steps to apply for a credit card

If you'd like to take out a credit card, you'll need to complete an application process first. Follow these steps to prepare your application.

1. Get pre-approved

Some credit card issuers allow you to get preapproved or prequalified for their credit cards. You'll need to fill out a form and submit your personal information via the card issuer's website. Once you've submitted the form, the card issuer will initiate a soft inquiry on your credit report. A soft inquiry will not affect your credit score.

If you receive a preapproval notice, you've met all the lender's criteria so far. A pre-approval indicates you are likely to get approved, but approval is not guaranteed. You'll still need to apply for the card to be fully approved.

2. Check your credit score

Your credit score is how creditors determine your creditworthiness or how likely you are to pay back a loan. A lot of weight is put on your credit score when you apply for a credit card. Knowing which credit score range you fall in will help you identify the right cards to apply

for.

For example, if a credit card company advertises cards for people with excellent credit (8001 credit score) and you fall in the "fair" credit range, then you'll probably want to steer clear of that specific card.

Credit scores consider your payment history, credit utilization, credit age, credit mix, and how often you apply for new credit. You can check your credit score through a credit card issuer or by ordering it from one of the three main credit bureaus: TransUnion®, Equifax®, or Experian®.

Here is a breakdown of the credit score ranges2:

Exceptional | 800 to 850 |

|---|---|

Very Good | 740 to 799 |

Good | 670 to 739 |

Fair | 580 to 669 |

Poor | 300 to 579 |

3. Choose a card that meets your needs

To narrow down your list of options, start thinking about what you need from a credit card. Here are some common cards you can get and when they make sense.

Secured credit cards: If you have no previous credit history or score, you'll want to look for a credit card that doesn't require those, such as a secured credit card. Secured credit cards are a common tool for beginners to build credit and only require a cash deposit to open.

Retail cards: You can also consider a retail credit card if you're new to credit. Store credit cards are generally easier to get approved for, but be careful: They often incentivize you to shop at a retailer more than you might otherwise.

Reward credit cards: If you've already got a solid credit score from previous credit cards or other types of loans, you may be able to apply for a rewards card. Rewards credit cards offer incentives to consumers with stronger credit scores, such as cash back or travel rewards. Some travel cards waive foreign transaction fees when you spend in another country, a cost that can quickly add up on international trips otherwise.

There are several types, so do your homework to figure out which are the best credit cards for your needs. It's okay to have multiple credit cards as long as you can keep up with the payments.

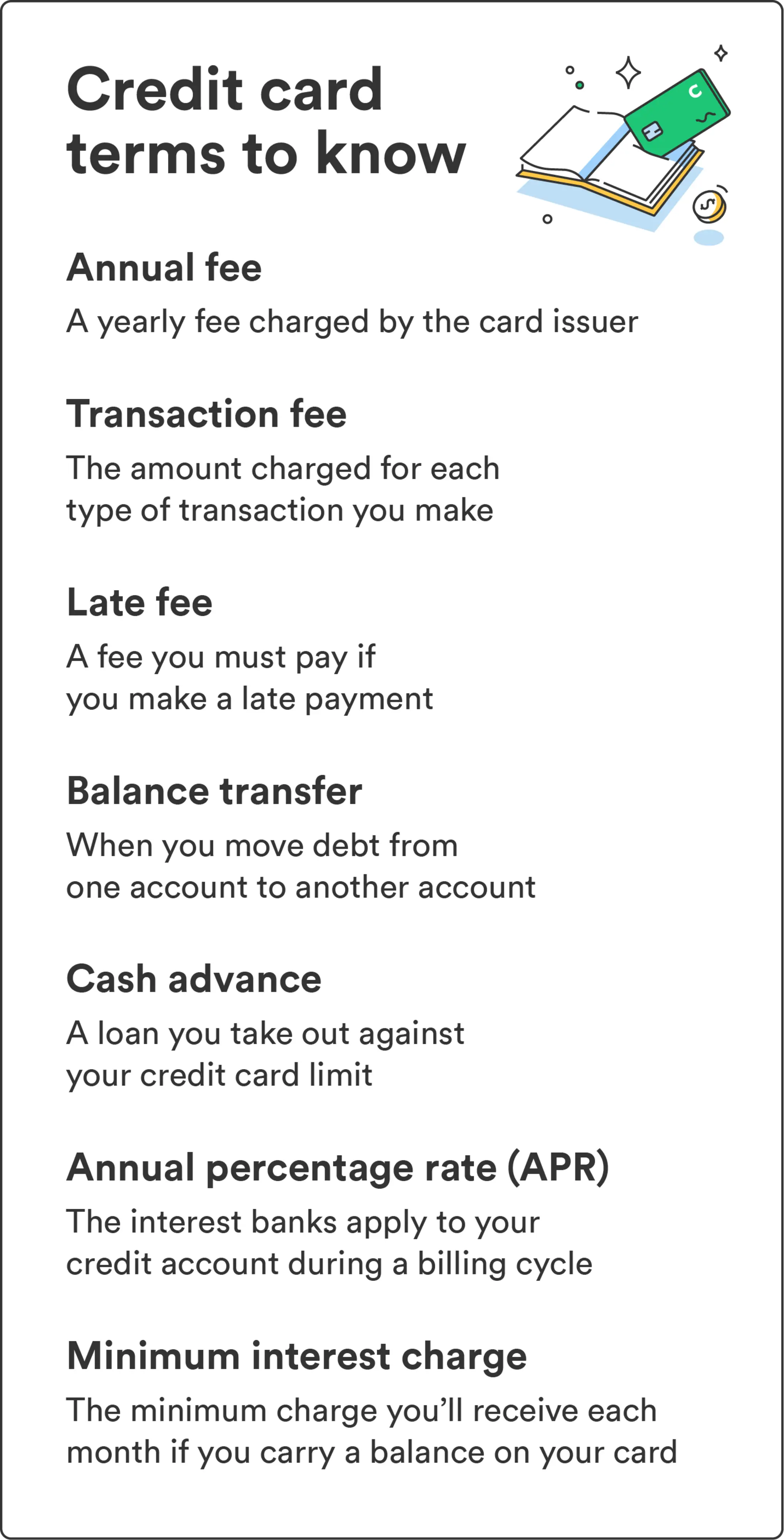

4. Know the card's terms and conditions

Every credit card has a unique set of terms and conditions that detail the agreement between the credit card issuer and the holder. You should be able to view the terms and conditions before you submit your application.

Credit card terms and conditions can include fees that holders are responsible for, interest rates, and the card's annual percentage rate (APR). The rate could be different for spending versus taking a cash advance. If the credit card comes with a rewards program, the details of how a holder claims their benefits can also appear here.

Always check the terms and conditions of a credit card before applying so that you understand what fees you will be responsible for and which rewards you are entitled to. If there's an annual fee, think about whether you'll earn enough rewards during the year to come out ahead.

An understanding of your agreement with a credit card issuer is vital to keeping your credit healthy.

5. Decide how to apply

Now that you're ready to apply for your credit card, you'll need to choose how you want to do it. Depending on the card issuer, you may have a few options:

Applying online will probably be the quickest and most convenient method – you may even get approved instantly.

If you prefer a face-to-face experience, you can also apply in person at a bank or credit union issuing the card. Applying in person will allow you to receive a quick response on approval, and you can ask questions in real time.

You may also apply over the phone, but anticipate that you might be on hold for some time.

The last and least convenient option is applying through the mail. If you opt for this method, it could take weeks to receive a response.

No matter which route you choose, getting approved for a credit card will probably be easier if you apply at a financial institution where you already have a checking account or savings account.

6. Gather the necessary information

To speed up the credit card application process, come prepared with the information you'll need to apply.

Application requirements can vary from issuer to issuer, but in general, this is the info you should know beforehand and have proof of:

Full legal name

Social Security number

Address (you must have a valid U.S. address)

Date of birth

Annual income

Housing costs

In addition, a card issuer might ask for subsidiary information, such as how long you've been at your current address and if you own or rent your home. They could also ask about your current employer, your main source of income, and any assets you may have.

7. Submit your application

Once you've selected a credit card that meets your needs, gathered the necessary documents, and filled out your application, it's time to submit the form and wait for the results. Depending on the health of your credit report, application approval can take a few minutes or a few days.

After you click submit, a hard inquiry may impact your credit score. That's why it's a good idea to limit the number of credit cards you are applying to at the same time. The good news is that the effects of a hard inquiry are often temporary.

Learning how to apply for a credit card is a smart first step toward building your credit history. After you find the perfect credit card for you, learn how to maintain a healthy credit score.

What to do if your credit card application gets denied

Unfortunately, you are not guaranteed to qualify for a credit card. Even after following all the steps, you might find your application denied. Don't get discouraged. There are a few steps you can take next.

Review the reason

If a credit card company denies you, they must send you a letter explaining why because of the Fair Credit Reporting Act.3 Check what happened so you can plan your next move. Some common possibilities include:

Your credit score is too low, or you don't have enough credit history

You have too much outstanding credit card debt and loans

Your income is too low

You applied for too many credit cards and personal loans at once

You ran into past credit issues, like a bankruptcy

Try with another credit card company

If you feel like you were on the borderline of qualifying with the first application, you could try again with another credit card company, perhaps applying for one with fewer requirements. If you were denied a premium travel card that required a high income, you could try applying for a cash back credit card instead.

Work on improving your credit score

Think of how you could improve your credit score for the future. If you are close to maxing out your credit cards, aim to pay down the balances and lower your utilization rate. A personal loan could also improve your credit.

Be sure to keep making the monthly payments on any outstanding loans, credit cards, and bills. This slowly and steadily adds points to your score.

Start with a secured card

If you can't qualify for a regular credit card now, you could build up your score using a secured credit card. These cards allow you to use a security deposit to act as your credit limit. When you pay off the card each month, it improves your credit score.

Wait and apply again later

Getting denied a credit card can be frustrating, but it's just a minor setback in a lifetime of managing money. Focus on improving your credit and building your income. Give it six months between applications.4 At this point, try applying again as a stronger candidate. Hopefully, this time, you get through.

If approved, use your credit card responsibly

While you might be excited to start spending and earning rewards, plan how to use the credit card responsibly.

Smart spending: Only spend what you can pay off monthly on the card. Credit card interest rates are extremely expensive. Let's say your card has a 25% interest rate. $10,000 of debt will cost $2,500 a year, over $200 a month in interest. If you fall into debt, you might be paying it off for years.

Monthly payments: Closely track when your monthly bill is due. If you don't pay your credit card by the deadline, you will be charged an extra penalty and it will hurt your credit score. Set a reminder on your calendar and smartphone. Or schedule automatic payments from your bank.

Watch out for fraud: Pay attention to your monthly statements. Make sure there aren't any purchases you don't recognize, as those could be a sign of fraud. By following these basic steps, you'll be on the right track as a responsible cardholder.

Make credit cards work for you

A credit card can be a powerful financial tool if you use it properly. It saves you from carrying loads of cash, earns rewards, and can even be used to pay your taxes.

Qualifying is the first step. By following this advice, you'll give yourself the best chance of landing a new card, and then you can start enjoying the benefits.

If you're still weighing whether a credit card is right for you, check out the pros and cons of using credit cards.