In The Green®

Most Recent

Chime Guides

Chime Guides

Credit

Banking Basics

Banking Basics

Safety & Security

Managing Debt

Money Habits

Payday

Money Habits

Money Habits

Money Habits

Money Habits

Chime Guides

Chime Guides

Explore Videos

Check out the latest money moves, member stories, and finance guides.

Top Credit Card Tips That Can Boost Your Score #Chime #FinanceTips #Shorts

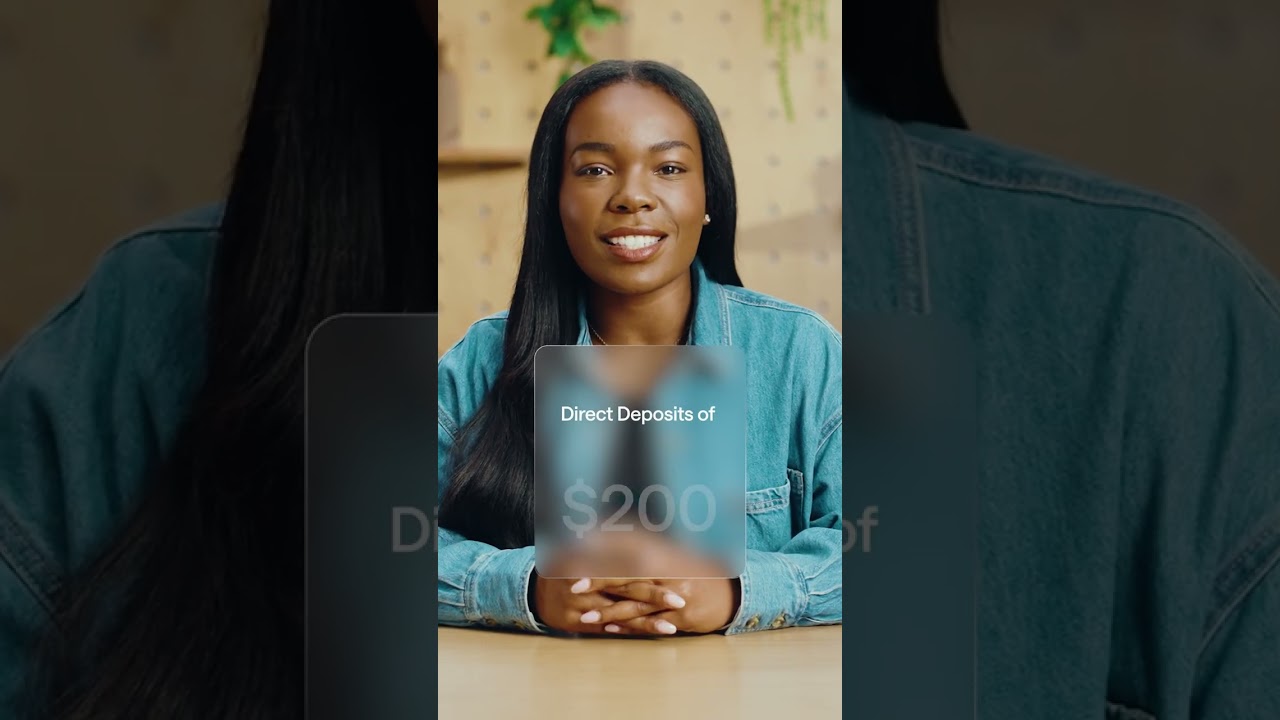

Get up to $500 before payday with #Chime #shorts

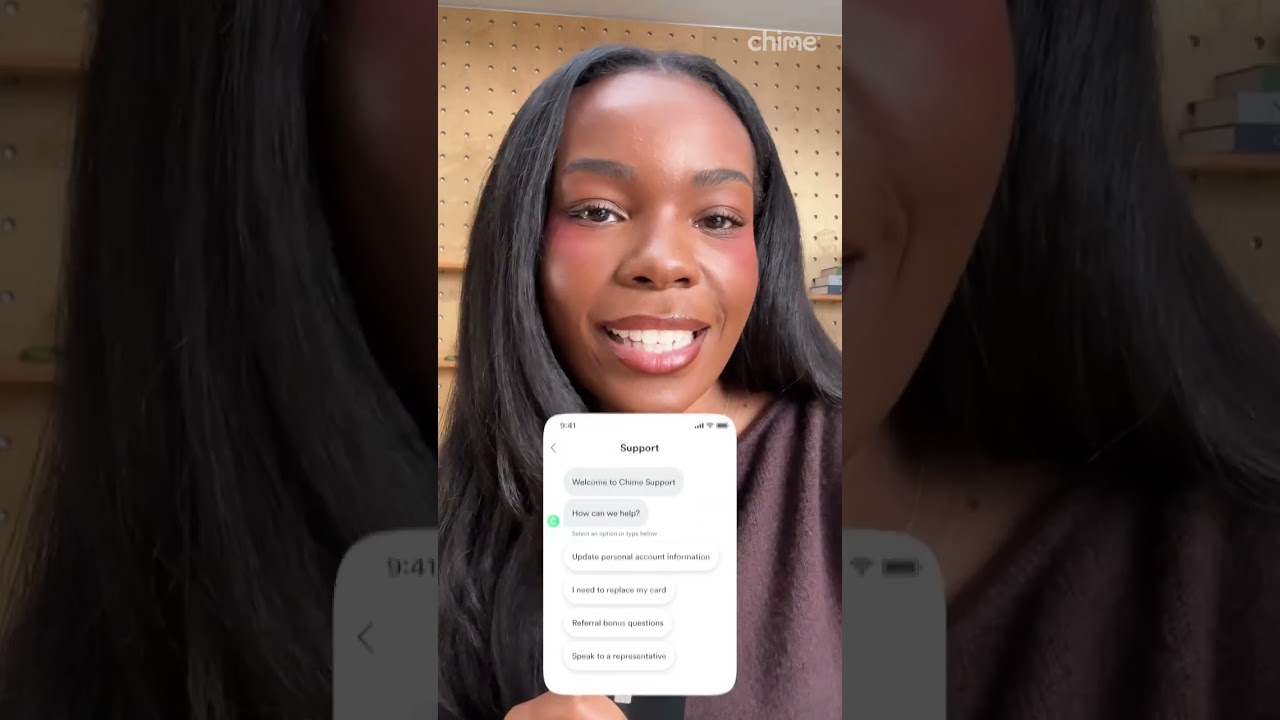

Quick #Chime tip: Need to reach us? This is how to contact customer service 💬

Easy online banking

Applying for a Chime Checking Account is free and takes less than 2 minutes. It won’t affect your credit score!